Jason Todd

Stagflation has re-entered Australia’s macro vocabulary with unusual ease, but the label is doing far more rhetorical work than analytical work. In technical terms, Australia does not (yet) meet that definition, but the risk is already being amplified with qualifications somewhere in the fine print. Stagflation is a powerful word, but misusing it risks overstating the threat and misunderstanding how both policy and markets are likely to respond.

Equity investors are a resilient bunch. Over the past five years, markets have absorbed an almost uninterrupted sequence of shocks and moved higher. Only the inflation and rates shock of 2022 produced a sustained drawdown, and this was as much about the magnitude of the problem as it was about failing to recognise it early. Every other sell-off has been shallow and short-lived, including the most recent, where markets did a round trip in a little over a month.

This is an encouraging trend, but one that is not fully recognised. Markets have not only rebounded from fears around energy supply disruptions but have done so while simultaneously ringfencing stress in specific pockets – notably the ongoing bear market in software and rising unease across parts of private markets. We think this reflects the resiliency of the macro backdrop as well as the tailwinds of structural drivers propelling parts of the equity market complex higher. There are a lot of naysayers, but recent history has illustrated that markets are now more effective at isolating shocks, reallocating capital, and distinguishing between what is systemically threatening and what is merely disruptive. Time and again, this has been on display.

That brings us to the current juncture. We do not pretend to know how or when the current Middle East crisis is resolved. But a ceasefire, even an imperfect one, has materially reduced tail risks which the market has been quick to price in. Negotiation under constrained escalation is always preferable to negotiation amid open conflict. While the first round of talks failed, both sides now have clearer lines of disagreement, and the fact that discussion continues under de-escalation is a meaningful step forward and in permanently removing the war discount from equities.

That said, some economic damage is inevitable and already in the pipeline. Elevated energy prices and inventory pressures will weigh on growth, particularly as confidence remains weak.

Australia has kicked an own goal via poor strategic policies around energy supply and a mish-mash of policy statements that have sown the seeds of confusion and panic. It is inevitable that growth and corporate earnings downgrades are coming. But while “stagflation” is a distinct possibility, we draw the line at using this as a reason to embrace a negative view on assets. In fact, we go further and suggest that it is now becoming a misused synonym for “danger” when, in fact, the outlook is far more nuanced.

Stagflation is often invoked as a synonym to infer investor danger, but it is a very different economic condition from recession, and far rarer. A recession has a clear statistical anchor: two quarters of negative growth marked by falling output and rising unemployment. Stagflation does not.

It has no formal threshold, no declaring authority (like the NBER in the US) and therefore has a looser diagnostic standard. In simple terms, it requires the coexistence of persistently high inflation, stagnating growth and rising unemployment, all at the same time. That combination matters because it traps policymakers where tightening worsens job losses, but easing entrenches inflation.

But it is because stagflation has no hard thresholds that it is so easily overused. Slowing growth with inflation above target is not stagflation unless labour markets are breaking. Anyone can sound bearish by reaching for the word, but true stagflation is structurally toxic, not merely uncomfortable – and mislabelling difficult late-cycle conditions as stagflation risks overstating the threat and misunderstanding how markets are likely to behave.

Economic strain, economic pain?

Much of the stagflation rhetoric applied to Australia collapses under closer inspection. True stagflation requires persistently high inflation, stalled growth, and a sustained rise in unemployment, simultaneously and over time. Australia does not meet that test. Inflation has moderated from its peak, growth is slowing but not stagnant, and the labour market remains tight rather than deteriorating. The danger lies not in the term itself, but in mistaking economic strain for economic breakdown and in not being able to differentiate between the risk of stagflation, a stagflationary shock and/or a period of prolonged stagflation.

Why is the equity market so elevated if stagflation is coming?

We are not concerned by the macro narrative that is amplifying the risk of stagflation or arguing that markets are complacent about downside risks because they have bounced back to record highs. There is a time dependency to the outlook, and the economic and earnings impacts are non-linear.

But we remain more optimistic than prevailing commentary and don’t see why the Australian markets cannot continue to perform despite growth and inflationary concerns. The most important question does not hinge on someone’s definition of stagflation, but on the mix of growth and inflation at which markets can perform.

Over the past year, the equity market has not had a problem absorbing inflation above the RBA’s band and provided inflation and growth shocks are temporary, I don’t think this will change outside of how you isolate the impacts for individual stocks. Obviously, we don’t know how the RBA will react or what the implications will be (with certainty) on corporate earnings, but the COVID-19 growth/inflation shock was not that long ago, and if memory serves me right, investors did not permanently discount stocks, and I can’t see why they would. We make the following points:

- We think some of the recent panic reflects narrative amplification rather than new information. Political polarisation, particularly in the US, has increasingly distorted macro interpretation, encouraging investors to favour worst-case readings of events over probabilistic assessment. In other words, it’s been way too easy to be bearish, but that bias is now receding from prices, even if not from headlines.

- We don’t see pre-Iran war highs as a constraint for markets, either offshore (particularly the US) or Australia. We think underlying equity dynamics were solid heading into the war, and while there are areas under greater stress as we exit the crisis (such as the consumer and industrials highly dependent on energy), we see this as isolated drags rather than market constraints.

- Collapsing confidence is not inconsistent with elevated equity markets. Consumer confidence is weak, yet equity markets sit near record highs. That is not a disconnect – it is how markets have always worked. Confidence is a poor leading indicator for equities. It reflects how households feel about the past. By contrast, equity markets are pricing in the future value of earnings, which are not necessarily determined by where confidence sits. Furthermore, sentiment often collapses after economic stress is already evident, while markets often recover well before confidence does.

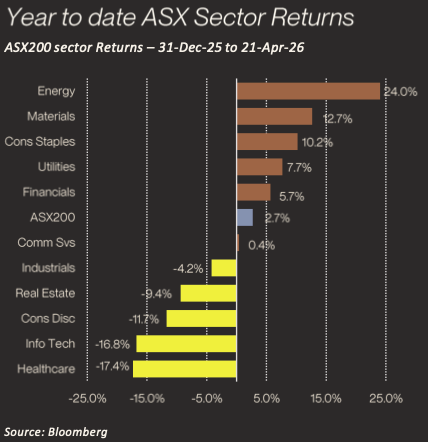

- Peak Australian equities is not peak share prices for many stocks: The ASX200 index is only 3 per cent off its record high and has almost recovered the entirety of its Iran conflict losses. However, healthcare ( -18 per cent), IT (-17 per cent), consumer discretionary (-12 per cent), and property (-10 per cent) are all well down year to date. It has been defensive sectors such as consumer staples (+10 per cent), utilities (+8 per cent), as well as energy (+24 per cent), and materials (+13 per cent) that have driven the market higher. This performance distinction is consistent with cyclical concerns, not ignorant of them.

What should investors do?

We urge investors to carefully interpret “stagflationary” and “higher for longer inflation” narratives. The term stagflation is being overused and misused regarding its negative implications for investors. Even in a stagflationary environment, equities can still outperform bonds, and cash, given the erosion of real fixed income/cash returns, and if pricing power and defensive earnings streams support nominal earnings for the equity market.

The reason why the equity market has recovered despite ongoing energy supply concerns is that corporate earnings have risen due to the contribution from Energy and Materials. We think it’s wrong to argue the market is complacent on risks, given that the earnings backdrop remains supportive – if not bifurcated. What’s more, the market is discounting cyclicals and other areas of the market that are likely to come under downside earnings pressure.

On the other hand, there are clear relative winners from a short bout of stagflation, such as those with pricing power (energy, materials, and utilities) and those with defensive characteristics, pass -through ability and real earnings power (consumer staples & healthcare). We don’t think the market is mispricing risks, and investors should avoid getting overly negative off the back of a blunt statement that the Australian economy is heading towards stagflation. That time may come, but it needs to be seen in hard data and not just via a narrative that wants to cover all downside bases.

By Jason Todd, CIO