Weekly market & economic update – week ending 14 February, 2014

17

Feb

2014

From Shane Oliver - AMP chief economist

Investment markets and key developments over the past week

- Shares rose over the past week thanks to a combination of soothing comments from Janet Yellen, good Chinese trade data, talk of more easing in Europe and, in Australia, good earnings results & soaring dividends. Emerging market worries seem to be fading a bit. Growth optimism also saw commodity prices rise with the $A making it back above $US0.90. Bond yields generally rose though as safe haven demand continued to fade.

- Steady as she goes from Janet Yellen. Those who were uncertain about US monetary policy following the handover from Ben Bernanke as Fed chair can breathe easy. The key message from Janet Yellen is clearly one of continuity: gradually winding down QE but only if the economy continues to improve as expected and interest rates to remain on hold well after unemployment has fallen below 6.5%. While Yellen painted an upbeat picture on the economy she clearly still sees unemployment as being too high (despite falling participation) and inflation too low and therefore sees the US requiring accommodative policies for a while to come.

- No debt ceiling debacle in the US, with Congress smoothly suspending it till next year. Quite clearly the Republican leadership has decided that a re-run of the battle last year was not in their interest given the mid-term elections later this year. So the political truce in the US continues and for now the economy is a key beneficiary, at least till after the mid-terms. But with the US budget deficit having fallen to 3.4% of GDP from over 10% post the GFC and government spending flat the last five years, it’s rapidly receding as a political issue.

- Will Toyota’s decision to cease making autos in Australia in 2017 following exit moves by Ford and Holden knock the economy into recession? No. Toyota’s decision seemed inevitable, but it’s still horrible news for the workers, families and communities that will be directly affected. Direct and indirect job losses from the shutdown of auto manufacturing could run up to 40,000 or so. But claims of recessions and economic disaster for Australia are ridiculous. First, even if 40,000 jobs are ultimately lost this is still tiny compared to total Australian employment of 11.5 million people (just 0.3%) and the job losses will be spread over the next 3 years. Second, this impact is likely to be reduced by government assistance programs. Thirdly, it should be noted that manufacturing has been in decline for 50 year or so. Back in 1960 manufacturing employed 26% of the workforce and now it’s just 8%. And yet the economy has performed well despite this. Finally, we need to accept that government assistance of the auto industry amounting to $30bn over the last 15 years in tariffs and subsidies was a waste of taxpayers’ money. The subsidies can now be re-directed to well-targeted infrastructure spending which is what the economy really needs and tariffs on car imports should now be eliminated leading to lower car prices and a boost to real household spending power.

- Looks like a big round of privatisation on the way in Australia. The impression from the Treasurer is that the May budget will likely see big savings focussed on spending cuts rather than tax increases and that another big round of privatisation is on the way. Providing the spending cuts are not too short term focussed but are rather aimed at getting long term spending growth back to more reasonable levels, this is all a move in the right direction. Renewed privatisation is particularly positive as the private sector invariably runs assets better than governments do, it will provide opportunities for super funds to invest in Australia infrastructure rather than having to go offshore and it will free up public money for new infrastructure spending and/or debt repayment.

Major global economic events and implications

- US small business optimism rose but retail sales and jobless claims look to have been dampened by bad weather. With bad weather continuing this month, it will be March before clean US data can be expected again.

- The US December quarter profit reporting season is now 80% complete and is seeing profits come in about 5% better than expected. 76% of companies have beaten on earnings and 65% have beaten on sales.

- Eurozone industrial production was soft in December but this followed a solid gain in November and PMIs point up. Meanwhile, another ECB official indicated consideration was being given to further monetary easing. While PM Letta is stepping down in Italy, clearing the way for Matteo Renzi to take over, the market reaction has been relaxed as a new election is unlikely and Renzi is well regarded and will likely follow similar policies to Letta.

- Chinese data was good with benign inflation and strong exports and imports. The export data could have been distorted by the Lunar New Year but also lines up with stronger economic growth in the US and Europe.

Australian economic events and implications

- Australian data was mixed. On the bad side unemployment rose to 6% and consumer confidence fell. The jobs market is very weak with zero jobs growth over the last year and the highest unemployment rate since 2003. However, a rise in unemployment to 6% or above has been widely expected, including by the RBA and so it’s not a surprise and not enough to get the RBA thinking about more rate cuts. More importantly, the labour market is a lagging indicator of the economy reflecting last year’s weak growth. With more forward looking indicators for the economy pointing up we expect jobs growth to improve later this year which should see unemployment peak around 6.25% before starting to turn back down to around 6% by year end.

- In terms of more forward looking indicators the news over the last week was mostly good. The latest NAB business survey showed further improvement in confidence and conditions including a sharp rise in new orders and hiring plans, housing finance approvals continue to trend solidly up, tourist arrivals rose 7.5% through last year with even US arrivals picking up suggesting the fall in the $A is starting to help and ABS data confirmed solid gains in house prices which provides a strong boost to household wealth.

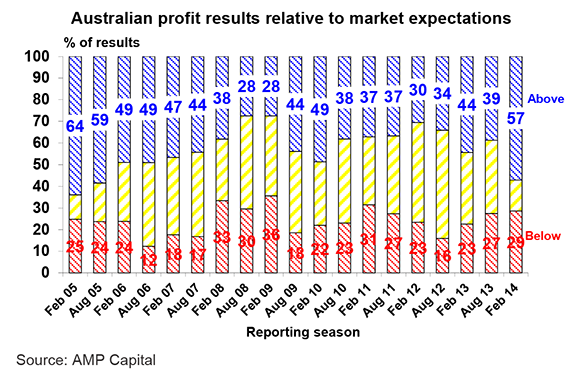

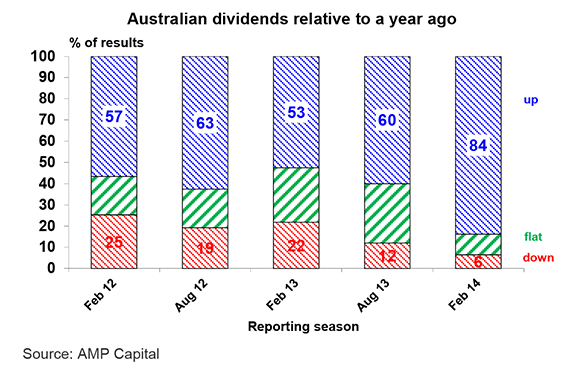

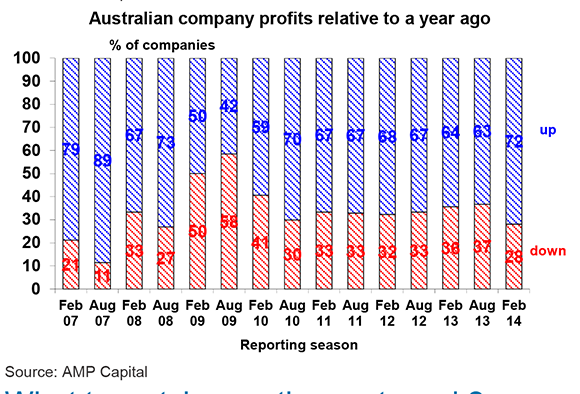

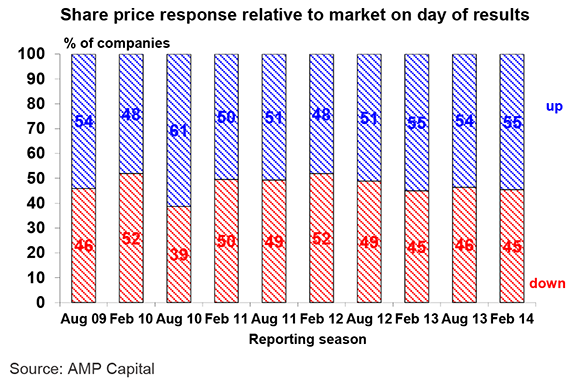

- The news from corporates has been very good. Its early days as we are only 20% or so through the December half earnings reporting season, but so far the results have been impressive. So far 57% of companies have exceeded expectations (compared to a norm of 43%); 72% of companies have seen their profits rise from a year ago (compared to a norm of 66%); a whopping 84% of companies have increased their dividends from a year ago (compared to an average of around 62% in the last two years); and 55% of companies have seen their share price outperform the day they released results. Key themes are a massive turnaround for the resources stocks (notably Rio), banks doing very well (with great results from CBA and ANZ), help coming through from the lower $A, ongoing cost control, improved outlook comments from cyclicals (like Boral) and soaring dividends. The surge in dividends is a good signal that companies are confident about the outlook. The bottom line is that Australian earnings look to be on track for strong growth this financial year.

What to watch over the next week?

- In the US, expect a slight rise in the February home builders conditions index (Tuesday), but weather related falls in January readings for housing starts (Wednesday) and existing home sales (Friday). The February Markit manufacturing conditions index (Thursday) along with the New York and Philadelphia regional manufacturing conditions indexes (due Tuesday and Thursday respectively) are likely to show continued reasonable growth, although all are at risk of being dampened by poor weather conditions. Inflation data (Thursday) is likely to have remained benign.

- In Europe, the flash Markit PMIs are expected to confirm a continued gradual recovery in economic conditions.

- Japanese December quarter GDP data is expected to show a rebound in growth to 0.7% quarter on quarter (or 2.8% annualised) driven by a combination of consumer spending and business investment. The Bank of Japan meets Tuesday but is unlikely to make any changes to monetary policy.

- In China, the flash HSBC manufacturing conditions PMI is expected to remain around the 50 level.

- In Australia, the minutes from the last RBA Board meeting (Tuesday) are likely to confirm the RBA as being comfortably on hold regarding interest rates. December wages data (Wednesday) is likely to show that wages growth is very modest at 2.5% year on year consistent with weak labour market conditions.

- This will be the peak week for Australian December half 2013 earnings results with nearly 100 major companies due to report including BHP, Wesfarmers, Woodside, AMP, Leighton and IAG. Consensus expectations are for 13% earnings growth in 2013-14 led by 35% growth in resources profits on the back of the lower $A and reduced capex and 8% growth for industrials. So far so good.

Outlook for markets

- Although returns will be more constrained and volatile, shares will nevertheless push higher this year helped by reasonable valuations, improving earnings on the back of improved economic growth and easy monetary conditions helping to entice investors to switch out of cash and bonds and into shares. Against this backdrop the recent correction was healthy in leading to less ebullient investor sentiment. The ASX 200 is expected to rise to around 5800 by year end.

- The recent decline in global bond yields should be seen as a correction against the background of a slow rising trend in yields on the back of gradually improving global growth. Cash and bank deposits continue to offer pretty poor returns given low interest yields.

- The broad trend in the $A remains down on the back of softer commodity prices, a reversion to levels that offset Australia’s relatively high cost base and a decline in Australia’s growth relative to that in the US. However, short positions in the $A still remain excessive and so it appears to be going through another short covering rally – supported in part by the RBA’s more relaxed stance on the currency – that could see it rise to around $US0.92-93 before the downtrend resumes.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist

————–