Solving the investor’s dilemma – managing volatility in equities (Part 2)

In Part 2, Dan Bosscher, Portfolio Manager at Perennial Value Management discusses the strategies utilised that make it possible to embed risk management within an equity portfolio and how this can provide investors with a degree of confidence to remain invested in equities, regardless of market volatility or their proximity to retirement. (Read part 1 here)

At Perennial Value, we believe it makes sense to embed risk management in the form of simple insurance style instruments into the equity portfolio itself. The aim is to manage some of the risk of equity market downturns automatically, without the investor having to make a conscious decision to change asset allocations. Using equity derivatives, managing risk in equity portfolios can be more efficient and cost effective, while leaving the upside in markets available to the investor.

Consider a portfolio with a beta approaching 1 on the upside but less than 1 on the downside. As the market rallies, the portfolio also enjoys that rally. As the market falls, the portfolio becomes increasingly weighted towards cash.

Unlike some strategies that give away the upside, we feel managing a portfolio of simple option strategies can achieve the best of both worlds. More importantly managing the downside that is closer to the current level of the share market can give us a better outcome.

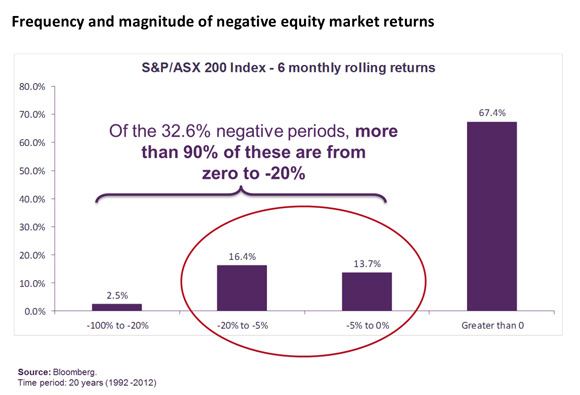

We focus on the most likely loss range of a portfolio. To determine the most likely loss range, in the chart below we show six monthly Australian equity returns over a 20 year period. Approximately two thirds of the time, returns are positive and almost one third of the time, returns are negative. Importantly, of these negative returns, 90% of the falls are between zero and -20%.

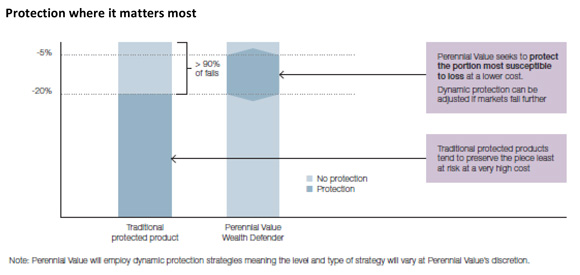

It makes sense to focus on the capital losses that are most likely to occur. This type of dynamic protection differs significantly in its approach versus many other protected products. Traditional protected products tend to preserve the portion of the portfolio down to zero after the initial fall, sometimes at a very high cost. If you think about this in practical terms, this is the portion least at risk. For example, it is hard to imagine that 100% of the shares in the S&P/ASX200 suddenly all become worthless overnight. As shown in the chart below, dynamic protection focuses on the portion of the portfolio most susceptible to loss, typically in the -5% to -20% range. As markets fall, we adjust the dynamic protection strategies and/or increase cash to protect investor capital.

The other limitation with traditional protected products is that they can end up cashing out in a major market correction, and inevitably when the market does recover, the investor does not get to participate in the upside. We need to avoid this outcome and reset the clock each day, making sure today’s portfolio can meet the needs of the investor.

We buy insurance on our biggest asset, our house, our valuables and car. We even buy insurance on our lives and earnings. But one of our biggest assets, our superannuation, is rarely insured. Why not? Access to option markets can be complex and expensive. This process needs to be managed in an ongoing and professional manner. Option markets provide insurance to the investor. Managing option portfolios historically has been the domain of the investment banking community who design, structure and sell products to do this for us. They can be extremely good investments but they can be complicated, expensive and inflexible for the average investor. The role of the professional investment manager is to navigate this environment such that the portfolio owns the most efficient insurance at any time, maintaining a highly flexible approach compared to most other common strategies.

Derivative instruments can be complex and risky. Intuitively selling insurance is a risky business. Receive a nominal amount and risk an event that could be 20, 30 times more damaging than what you have received. While a derivative portfolio can sell options there is one simple rule to live by: be the net buyer of insurance. i.e. make sure that you own more insurance than you sell. In derivative speak this is called being long ‘vega’.

There are various option strategies that can be used to protect against significant losses. Some of the strategies used include:

Put option – buy put options at a specific strike price to protect the portfolio against falling markets below the strike level.

Put spread – buy put options at a specific strike price while also selling the same number of puts at a lower strike price. A put spread protects the portfolio in falling markets, but to a more limited degree compared to a buying a put option alone, and therefore costs less.

Put spread collar – purchase a put spread while simultaneously selling (writing) an out of the money call option. A put spread collar allows for some upside potential, with less downside risk when there is a decline in the market, for relatively little cost.

Put time spread – buy a put with a shorter-term expiration and simultaneously sell a put with a longer-term expiration. A put time spread allows the portfolio to gain if there is a fall in the market. It is also one of the lowest cost protection strategies used within the dynamic protection portfolio.

The table below shows some examples of the most commonly used protection strategies, what they can achieve on both the downside and upside, and how they compare to each other on a relative cost basis.

By maintaining market participation, and having in place protection strategies that will provide a pay off if the market falls by a specified percentage, capital can be better preserved in the long run.

Dynamic protection can provide peace of mind. If you can limit the downside, investors can feel empowered to stay invested in equities even if markets get choppy, when they might otherwise just panic and exit the market, quite possibly at the wrong time. Limiting capital losses in a market downturn is equally, and possibly even more important, than maximising outperformance in rising markets, due to the effects of compounding. By reducing the impact of a fall in the market on your equity investments, you should have a higher level from which your capital can grow, all thanks to the effects of compounding. Compounding works best if you stay invested. By maintaining market participation, and having protection strategies in place, capital can be better preserved in the long run across varying market conditions.

At Perennial Value, we believe we have moved the goalposts by combining a mainstream long-only Australian equities capability with dynamic protection strategies in the Perennial Value Wealth Defender Australian Shares Trust. By doing this, we have created an investment capability that seeks to limit the drawdown in equity markets while retaining the ability to capture the full upside that equity markets generate over time. In other words, the best of both worlds for those investors who are seeking to protect their equities portfolio from significant capital losses.