Know your investment manager: They may not be as passive or active as you think

Active or passive? The argument within the investment community over which offers better results continues to rage. However, we think that a more important question is being missed – are investors getting what they expect from the two investment styles? At Nikko Asset Management, we would argue that perhaps they are not.

Not all active managers are as active as you might expect –‘closet indexers’ are becoming ever more prevalent. This can surprise investors in those managed funds who expect an active manager to be active but actually receive a close-to- benchmark return. Conversely, depending on the benchmark followed by passive investment strategies, investors can be unwittingly invested in some surprisingly risky indices. Due to their composition, some of these benchmarks are actually very active bets on certain market risks and thus can entail higher risks than investors expect for a ‘passive’ strategy.

In our view, it is important for investors to truly understand their investment managers and the risks that they are taking on. These issues have implications for expected returns.

In a world where the lines between passive and active are becoming ever more blurred, the identification of ‘true-to- label’ managers is crucial.

Active strategies are often more passive than people realise

Active investing seems to have failed investors’ expectations over a long period of time. On average, active funds have underperformed the market index by a statistically significant margin. This has led to an explosive growth in passive investing over the past decade, in large part because it is difficult for investors to justify paying active fund fees if active managers don’t generate alpha.

However, all is not necessarily as it seems.

Dr. Martijn Cremers and Dr. Antti Petajisto of the Yale School of Management analysed this topic in 2007 and proposed the concept of ‘active share’, which is defined as the percentage of a fund’s portfolio that differs from its benchmark index. In his 2010 study of the US fund management industry from 1980- 2009, Petajisto observed that actively managed mutual funds in the US saw their active share ratio consistently decline from 60% to less than 20%. He defines anything below 60% as ‘closet indexing’.

Petajisto’s conclusion is that on average, fund performance is correlated with the degree of management as measured by active share. The study shows that declining active share in so-called actively managed funds is what led to theunderperformance. This is because managers began hugging their benchmarks for a variety of reasons (job security, pressure to produce high IR, rigid risk control environment, swelling AUM, etc). The most significant catalyst may have been the GFC–when market volatility began to increase and stocks suffered severe losses, the pressure on managers to mitigate relative underperformance and increase risk controls was immense. This caused managers to align their portfolios more closely to a benchmark index in an attempt to reduce the risk of major underperformance and stem outflows from their funds.

However, the study shows that the most active stock pickers outperformed their benchmark indices even after fees and transaction costs. Concentrated stock-picking can produce consistent excess returns, whereas managers that purport to be ‘active’, while actually hugging a benchmark, can underperform. In the study, non-index funds with the lowest active share score underperformed their benchmark by over 1% annually net of fees.

Our investment management teams believe that it is important to take active positions based on the fundamentals of issuers, stocks and fixed income securities. Valuation is crucial to the delivery of long-term returns, while closet index tracking can be detrimental to real returns and the preservation of capital. We view benchmark indices as a useful way to measure long-term performance compared with the broader market and not something to be rigidly followed as part of the herd. As global investor Sir John Templeton said, “if you buy the same securities everyone else is buying, you will have the same results as everyone else. By definition, you can’t outperform the market if you buy the market.” If you claim to be an active manager, then you should be actively managing portfolios with high conviction calls and not just chasing the index.

Passive strategies more active than you might think

Apart from lower fees, passive strategies seem to offer the perception of lower risk than active management since index funds shouldn’t underperform the benchmark. However, passive strategies replicate the composition of a particular index, which in itself implies certain market bets depending on which regions and/or companies it comprises. Passive investment strategies can actually be riskier than investors expect since certain benchmarks actually entail very active bets on certain market risks.

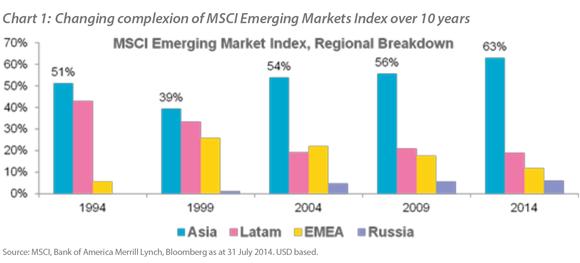

As an example, if you look at the MSCI Emerging Markets Index over the past two decades, its composition has changed dramatically (see chart 1). Asia’s portion now accounts for almost two-thirds of the Index, compared with less than 50% when Asian Financial Crisis hit. MSCI is due to review the inclusion of China’s onshore equity market in its benchmark Emerging Market Index next year with a proposed initial 5% weighting. When this happens, it will cause a major shift in the index composition so that passive investing in that index will entail a direct exposure to Renminbi-denominated securities.

Thus, buying an Emerging Markets index can actually be a very active form of investing. ‘Passive’ Emerging Market investing with a market capitalisation-weighted index in effect means following a momentum-based strategy, where you increase the weight of the best performing regions and companies every year and sell the losers. Market capitalisations and stock returns drive the portfolio weights, dictating how much you invest in each region and each underlying company.

There is nothing wrong with momentum investing, but investors must understand that it works in certain cycles and fails in other cycles, so it may not be as ‘low risk’ as they expect. This is particularly true for passive strategies investing in China and shows how passive investing may actually be a very active form of investing when the choice of a market benchmark is not straightforward.

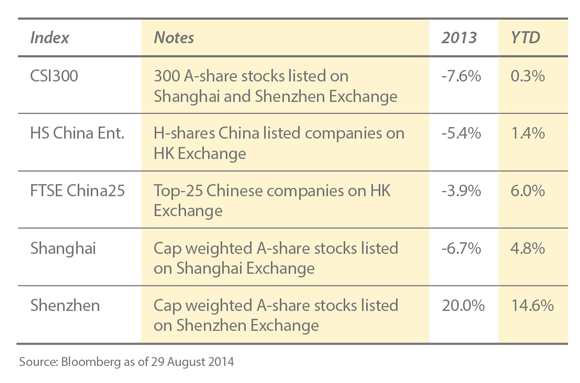

Due to market controls and government regulations, there are currently several exchanges where Chinese companies list and four or five indices that an investor can access to invest into China. But if you look at the components of these indices, they are vastly different in terms of what they cover.

Depending on which index you choose, you may be investing in the largest State Owned Enterprises in China where most of the ownership is still Beijing-controlled, or you may be more weighted towards private enterprises. Looking at the returns over the past two years, the differences might make you think that they are related to different continents altogether (see table below).

In effect, a passive investment into China is actually a very active bet on a particular sector of the Chinese economy. Factors in Emerging Markets are far too complex and too fluid to have a truly passive investing strategy so benchmark selection is crucial.

In addition, as Emerging Markets recovered from the GFC, the correction started to reflect regional dynamics and themes. These regional fundamentals have started to drive stock prices much more than macro events. For example, earnings from Asia have been rising much faster than the rest of the Emerging Markets (see chart 2). Looking at the differences in underlying fundamentals, you can see that labeling everything under the Emerging Markets banner may be an oversimplification of risks and returns in a ‘passive investing’ strategy.

By Yu Ming Wang Deputy President, Global Head of Investment, CIO International, Nikko Asset Management