Quality. As an investment term, it’s often touted, but not always well understood. Julian Beaumont of Bennelong Australian Equity Partners (BAEP) explains the term and how to use it to orientate long-term investment returns.

A bias towards high quality companies naturally comes with the question of how to define quality. The answer is not straightforward and there is no simple textbook definition. This contrasts with other investment styles such as value and growth that can be assessed objectively based on a few select quantitative measures. Value is characterised as cheap, typically by reference to a low price-to-earnings or price-to-book ratio; whilst growth is characterised by fast growing sales and earnings. Defined this way, there is generally near universal agreement when it comes to identifying the typical value or growth stock. Not so in the case of quality.

Trying to quantify quality

The concept of quality is inherently imprecise and subjective and, as a result, it can mean different things to different people. Unable to deal with this ambiguity, quants and the like have attempted to simplify quality down to a few quantitative measures. The issue then becomes deciding which metric or metrics best define quality, and in this respect, there is no uniform agreement[1]. A few select measures, however, are more commonly referenced and arguably do most of the heavy lifting, with probably the most popular being the return on equity, or ROE[2]. These are summarised in the design of the MSCI Quality Indices, which identifies quality stocks as those ranking in the top 5% in terms of return on equity, levels of financial gearing, and stability of earnings growth. Definitions like these in fact do a reasonable job of approximating quality, particularly in their effort to group stocks into quality ‘buckets’. Indeed, the MSCI World Quality Index is made up of the type of high quality stocks one would expect to see, including for example Microsoft, Johnson & Johnson and Nestle.

As much art as science

However, purely quant-based tests have limitations. These limitations are most pronounced at the individual stock level. Quant-based tests invariably rely on accounting-based metrics and this means they are necessarily backward-looking. They assume the past will carry on into the future, which is reasonable enough at a general level but ignores the possibility of change at any particular company. To gauge this, it is necessary to look at the softer issues that lie behind the numbers.

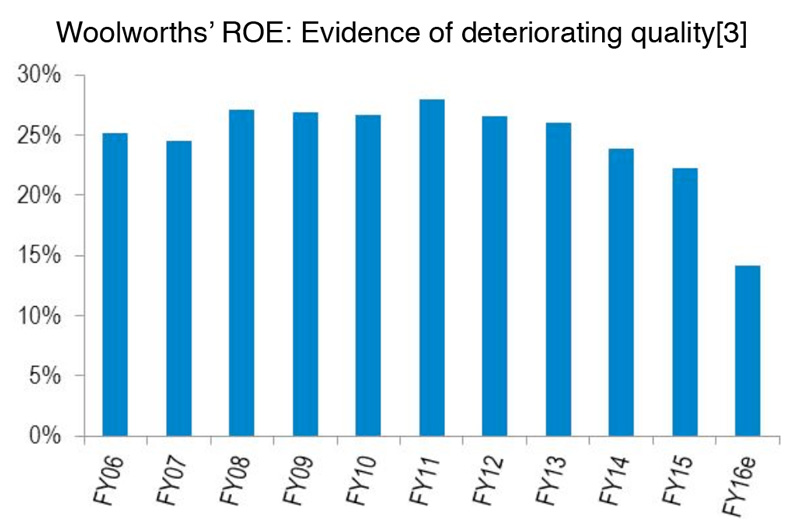

Until recent years, Woolworths Limited was considered one of the highest quality ‘blue chip’ stocks on the ASX. It dominated the supermarket industry with scale advantages and a compelling customer offering, which in turn allowed it to nicely grow sales, earnings and dividends. On its own admission, it then began late last decade to ‘put profits ahead of customers’, including pushing grocery prices and shaving in-store service. This manifested in profit margins that grew well above historic and global norms and evidenced a business that was over-earning. Soon enough, competition intensified, in particular with a new low-cost proposition from Aldi and a rejuvenated Coles. Somewhat arrogantly, Woolworths maintained a short-term profit focus, and these competitors were able to steal sales and chase down its lead. Meanwhile, a maturing profile saw it stretch for growth. This included heavy investment in new stores of questionable profitability and, helped along by a healthy dose of hubris, a misguided $4 billion investment in the Masters start-up. This year, the company will report asset write-downs of over $4 billion, a further decline in sales, and margins below Coles. It now finds itself facing a difficult turnaround that even on the company’s reckoning will take as long as five years.

Woolworths is a good case study in showing how an assessment of the qualitative factors – including the increased competitive intensity, deteriorating customer offer, poor capital allocation, and cultural concerns – are important in uncovering quality issues that the numbers alone may not reveal for some time.

A few other examples will suffice.

- Most investors today will quite rightly identify CSL Limited as a high quality global biopharmaceutical company. This was not always so. In the early 2000s the company struggled with uneven profits, sub-par returns on equity, and relatively high debt levels[4]. It was then in the process of consolidating the plasma products industry, first with the acquisition of ZLB Bioplasma in 2000, and then Aventis Behring in 2004. These acquisitions brought it scale and consolidated the industry, enabling it to build a strong competitive position in an attractively structured industry that underpins the strong returns and growth it enjoys today. Its share price has reflected the transformation, rising from below $4 in 2003 to now almost $120. As another example, TPG Telecom went from losing money in 2008 to a highly efficient, low cost provider by consolidating the broadband industry.

- Companies can restructure into higher quality franchises. Earlier this decade, Caltex was largely characterised by a very volatile and highly capital intensive oil refining business. In 2012, the company set about a restructuring which involved shutting its problematic Kurnell refinery and refocusing the company back to its quite stable and high returning fuel distribution business. Its share price almost tripled from the time the restructure was announced until the time its higher business quality came to be reflected in its financials. The reorganisation of Amcor last decade, in which it shed weak business and scaled up strong ones, is another example of quality improving as a result of internal restructuring.

- Companies materially exposed to regulatory risk can have their businesses or profitability upended. This regulatory risk is typically not evident in the financials. As an example, the lucrative Victoria pokies duopolies of Tabcorp and Tatts were literally taken off them by the Government in 2012 without compensation. Some industries that rely on Government licenses or funding, including gaming, healthcare and education, are particularly exposed to regulatory risk.

Earnings risk and upside potential

Fundamentally, we believe company earnings are the ultimate source of shareholder returns, both to the upside and downside. In this context, the quality of a company is that which defines its earnings risk and upside potential. In assessing quality, we employ a research-intensive approach that investigates all aspects of a particular company and its earnings prospects, including the qualitative and quantitative factors listed in the adjoining table, and in fact many more.

Contrasting examples

Superficially at least, Ramsay Health Care and Primary Health Care run quite similar businesses. Ramsay is the largest private hospital operator in Australia, while Primary is the second-largest operator of medical centres and pathology labs. Both companies provide healthcare services that are economically resilient and for which demand continues growing strongly. The two companies, however, provide a useful contrast in terms of quality.

Ramsay Health Care

Ramsay has a very strong competitive position through its ownership of a strategic portfolio of 70 private hospitals across Australia. These hospitals gain from significant barriers to entry. It requires considerable capital and time to set up a new hospital, and it is generally uneconomic to do so especially when it means competing against an existing hospital that already has scale. Owing to the popularity and scale of its hospitals, Ramsay is able to achieve very high occupancy levels, procurement and operational efficiency savings, and negotiate better rates with the private health insurers who are largely responsible for paying for their members’ hospital visits. Ramsay’s strength is evident in its Ramsay’s ROE of 23%, which in fact has been increasing in recent years.

Ramsay’s business is very well positioned to profitably take advantage of industry growth, which it does by

incrementally expanding hospitals to soak up the increasing demand. This involves considerable investment at high returns, which reflects and supports the high ROE, and which underpins strong growth in earnings per share (EPS) that has averaged 19% per annum over the last seven years. Fortunately, it has a large pipeline of similar investment opportunities, including over $1 billion over the next five years.

Ramsay has an enviable industry reputation. This is underpinned by strong relationships particularly with doctors, who are free to choose where to treat their patients. Top management shares a similar reputation. They are of high calibre, all long time employees of the company, consistently over-deliver, and have significant shareholdings of their own in the company.

In contrast to most healthcare service providers, Ramsay arguably has less exposure to regulatory risk. Its business receives a relatively low percentage of its revenues as direct funding from the Government, relying largely on private health insurance and private co-payments. To the extent that the Government retards the private hospital sector – for example by discouraging the take-up of private health insurance – it must take up the burden themselves. This seems unpalatable in the context of current fiscal constraints and forecasts of massive healthcare demand to come. Ramsay’s efficient operating model and willingness to invest reduces the risks of adverse regulation.

Primary Health Care

Primary’s market positions are more tenuous. The success of its medical centres business is largely determined by its ability to attract and retain doctors to work at its clinics. Primary’s main ploy is to ‘buy’ doctors, which has historically involved large upfront payments and tying them up with five-year lock-ups, minimum billing targets, and restraints of trade, all of which the company would aggressively enforce through the Courts. Understandably, this resulted in a strained relationship with doctors. In contrast to Ramsay, Primary has been unable to take advantage of industry growth, its doctor numbers have in fact been in decline for some time. The company is now looking to embrace more flexible working arrangements, including less focus on upfront payments, but it has little to offer a doctor that is truly unique, which in itself explains the previous need for large upfront payments.

Primary’s other large business in pathology is arguably a stronger one. The pathology industry operates with high barriers to entry, with the scale of the largest players ensuring their centralised labs are run more efficiently. However, the benefits of scale also mean heavy competition for the referrals of their client doctors. This has historically involved paying exorbitant ‘rent’ to the doctors to house collection centres at their practices, a practice which may now be regulated away. However, if margins are not competed down, they may very well be regulated down.

In fact, Primary is very exposed to regulatory risk. It derives the bulk of its revenues from GP visits and pathology tests and these are largely paid for by the Government through Medicare. As seen earlier this year with Medicare cuts to lab and imaging services, the Federal Government can and will restrict reimbursement on which Primary’s earnings primarily rely.

Like its industry reputation, Primary’s corporate reputation has struggled. Primary has historically been run more like a family business than a listed company. For example, the founder’s sons ran the company’s two main businesses from an early age and sat on the Board. An effort is now being made to improve governance with, for example, the two sons displaced from the Board and only one left as a business head. However, clouds remain, with for example the CEO currently embroiled in a corruption scandal relating to his time as CFO at Leighton Holdings.

Primary’s accounting has been particularly aggressive. The most obvious example has been in its capitalisation of the cost of acquiring doctors’ practices and in failing to amortise this cost over time. This has left its reported earnings overstated. Indeed, the real cost of these practices has drained cash flows and ensured high debt levels that are only now being addressed through asset sales. Including the goodwill for its ‘ownership’ of doctors’ practices, as well as for overpriced acquisitions along the way, its ROE is just 5%. Indeed, its market value is worth less than what has been invested into it. Excluding this goodwill, the company has a deficit of shareholder equity.

Having your cake and eating it too

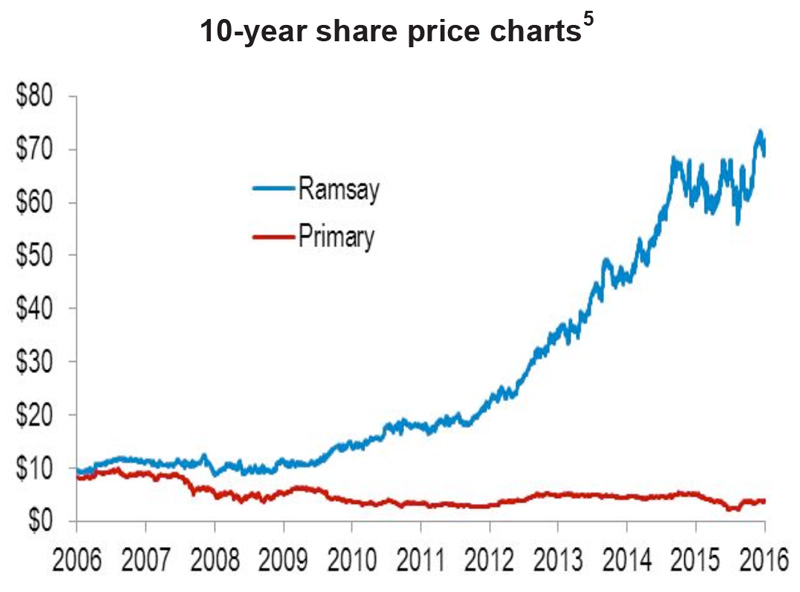

The chart below shows why it was worthwhile paying up for Ramsay’s quality instead of being sucked in by Primary’s apparent cheapness. Ten years ago Ramsay’s shares traded at $9.60 and are now almost $80. This performance has been underpinned by a quadrupling of EPS over that time. Primary’s shares traded at $8.40 ten years ago and have halved since to about $4 today, with its EPS a quarter less over that time.

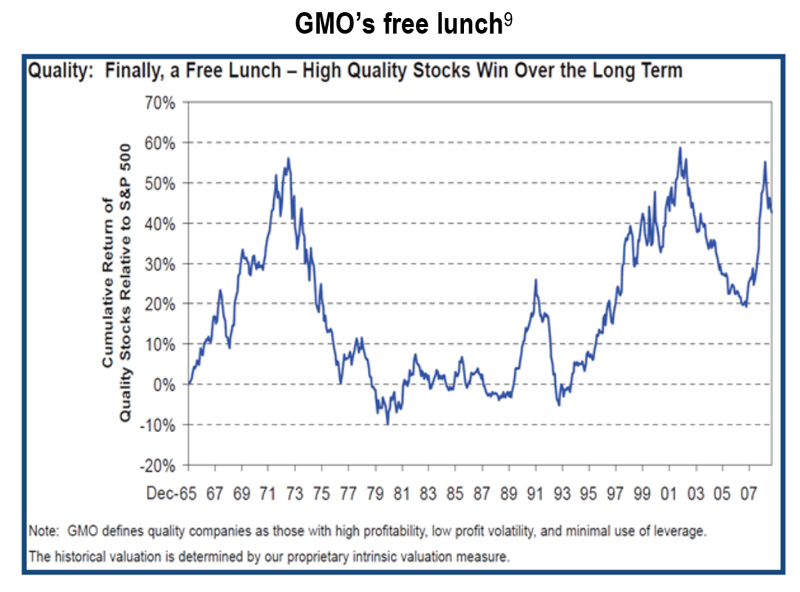

The experience of Ramsay and Primary is quite common for high quality versus poor quality stocks. Research covering both global and local markets[6] shows quite consistently that quality outperforms over time, and perversely for those that still think the two are inversely correlated, the better returns come with less risk. Indeed, Jeremy Grantham of GMO fame went as far as to say that in quality he had finally found a ‘free lunch’[7]. Interestingly, for those that insist that the ‘quality rally’ of the last five or so years explains the free lunch, Mr Grantham’s analysis, which relied on a similar definition to that used for the MSCI Quality Indices discussed earlier, is based on a period starting in 1965 and ending in 2009[8].

Quality’s happy combination of generally higher stock returns and lower risk reflects BAEP’s view of quality as defining the upside potential and downside risks of stocks. Of course, this is not an argument to buy high quality stocks at any price. The Nifty Fifty days of the 1970s is evidence against that, as seen in the steep peak down in the graph above. However, over time, quality is typically underappreciated and therefore undervalued. Quality works, it seems, because the market systematically undervalues the type of boring but reliable growth in earnings and valuation seen from the likes of Ramsay, and underplays many of the risks that threaten the earnings of the likes of Primary.

Conclusion

Our goal as fund managers is to maximise investment returns over time. We seek to achieve this by selecting stocks on the basis of their upside potential and downside risk. We view this risk-return dynamic for any company through the prism of earnings prospects, and in turn through a focus on the quality of a company. In assessing quality, we do not work to some narrow but easy-to-apply definition. Instead, we apply judgement based on quite a broad understanding of quality, which involves weighing up a great number of relevant factors. Unfortunately, the outcome is less clear cut than afforded by a quant-based definition, but we would rather be vaguely right than precisely wrong.

By Julian Beaumont, Investment Director

[1] To give you a taste from academia, there are two very different tests that have gained prominence: the first is the Novy-Marx measure that relies on the gross-profits-to-assets ratio (see Quality Investing, 2013, Robert Novy-Marx); the second is the Piotroski F-score that calculates the total of a binary 0 or 1 score on each of nine metrics such as ROA, asset turnover, and earnings quality (see Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers, 2002, Joseph Piotroski (University of Chicago Graduate School of Management).

[2] The return on equity or ROE is the most commonly used measure of a company’s productivity. It reflects the extent of a company’s profitability in relation to the investment made in its business and is calculated as the profit divided by shareholder’s equity. The intuition behind its use is that only a few privileged companies can achieve, maintain and invest at high ROEs. Capitalism is such that high returns tend to be competed away and it takes a company with special qualities to fend off capitalist attack.

[3] Source: Company accounts, BAEP estimates. Note that write-offs have been added back into shareholders’ equity.

[4] In 2003 financial year, CSL Limited earned approximately $70 million in post-tax earnings, had approximately $500 million of net debt, and its ROE was just 5.5%.

[5] Source: IRESS, for the 10 year period to 30 June 2016

[6] See for example “Investing in Quality” (UBS, P Winter, 17 April 2014)

[7] GMO, “Friends and Romans, I come to tease Graham and Dodd, not to praise them.” (On the potential disadvantages of Graham and Dodd-type investing.), April 2010

[8] Likewise, the MSCI World Quality Index has outperformed since devised in 1975 by 1.36% per annum, and over the last 10 years by 3.44% per annum.

[9] Source: GMO, “Friends and Romans, I come to tease Graham and Dodd, not to praise them.” (On the potential disadvantages of Graham and Dodd-type investing.), April 2010

———-

This information is issued by Bennelong Funds Management Limited (ABN 39 111 214 085, AFSL 296806) (BFML) in relation to the Bennelong Australian Equities Fund, the Bennelong Concentrated Australian Equities Fund and the Bennelong ex-20 Australian Equities Fund. The information in this document is current as at 4 August 2016. The information provided is general information only. It does not constitute financial, tax or legal advice or an offer or solicitation to subscribe for units in any fund of which BFML is the Trustee or Responsible Entity (each a Bennelong Fund). This information has been prepared without taking account of your objectives, financial situation or needs. Before acting on the information or deciding whether to acquire or hold a product, you should consider the appropriateness of the information based on your own objectives, financial situation or needs or consult a professional adviser. You should also consider the relevant Information Memorandum (IM) and or Product Disclosure Statement (PDS) which is available on the BFML website, bennelongfunds.com, or by phoning 1800 895 388. BFML may receive management and or performance fees from the Bennelong Funds, details of which are also set out in the current IM and or PDS. BFML and the Bennelong Funds, their affiliates and associates accept no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. All investments carry risks. There can be no assurance that any Bennelong Fund will achieve its targeted rate of return and no guarantee against loss resulting from an investment in any Bennelong Fund. Past fund performance is not indicative of future performance. Bennelong Australian Equity Partners (ABN 69 131 665 122) is a Corporate Authorised Representative of BFML.