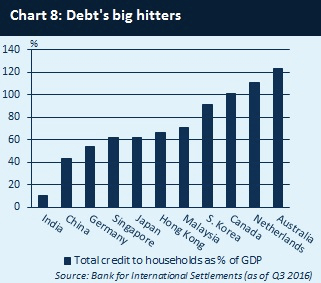

Developed Asia has been front and centre in the growth of global household sector debt over the last decade, with indebtedness in Australia, Korea, Hong Kong and Singapore now comparable to the world’s most heavily indebted nations (Chart 8).

Much of this growth has been underpinned by booming housing markets, which are difficult to control with interest-rate policies alone. Indeed, this is especially challenging in the current environment, with the loose policy required to address sluggish growth and inflation risks exacerbating financial imbalances.

In recent years, central bankers across developed Asia have sought to prevent excesses through a wide range of macroprudential policy measures. The results have been mixed.

In Australia, policymakers have been locked in a battle against household leverage for many years, with household debt-to-GDP rising above 120% – ranking number one globally.

In particular, the Council of Financial Regulators and the APRA have been vocal of late about the risks posed by interest-only loans and investor lending.

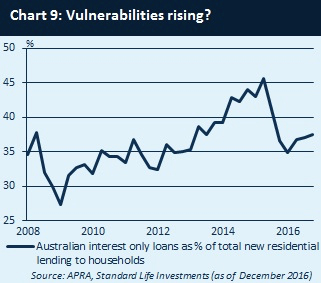

According to the recently published Financial Stability Review, interest only (IO) loans account for 23% of total owner-occupied loans, but a striking 64% of investor loans. It is the recent uptick in these IO loans, particularly the latter category, which has caught the regulator’s eye (Chart 9).

The concern is well founded. Given their structure, IO loans result in a higher average level of indebtedness over the life of the loan than a typical principal and interest payment loan.

Consequently, borrowers are more susceptible to falling into negative equity in the event of a housing price decline, while higher required payments at the end of an IO loan period increases the risk of default.

To make matters more awkward, it is exactly these types of loans that macroprudential tools were used to target in late 2014. The initial response to measures, such as higher interest serviceability requirements, was encouraging.

However, the recent resurgence in these loans raises questions about the effectiveness of these measures in the medium term. The latest Financial Stability Review certainly increases pressure on banks to rein in excessive risk and lenders are already responding, with out-of-cycle mortgage-rate hikes and tougher loan serviceability tests.

However, the persistence of IO and investor loan growth is likely to continue to increase vulnerabilities in the Australian housing market.