Seventy per cent of M&As fail – be one of the thirty per cent

M&A is high risk. Research from The Economist Intelligence Unit (and other sources) suggests that inadequate due diligence is a key factor in business case failure – particularly as it reduces the effectiveness of the integration program.

Even Wesfarmers can get it wrong!

There are many examples over many decades of M&As failing to achieve their business cases. A very recent Australian example is the 2018 sale by Wesfarmers of the UK DIY chain Homebase, reportedly for £1.00, after just two years of ownership and an initial purchase price of £340 million.

One of Australia’s great companies, and a very experienced acquirer, Wesfarmers sold Bunnings UK and Ireland with reported write-downs of AUD$1 billion. The company has been criticised by some for failing to understand the differences between the DIY markets in Australia and the UK.

Wesfarmers managing director, Rob Scott, said: “Homebase was acquired by Wesfarmers in 2016. The investment has been disappointing, with the problems arising from poor execution post-acquisition being compounded by a deterioration in the macro environment and retail sector in the UK.”

The missing comparative due diligence

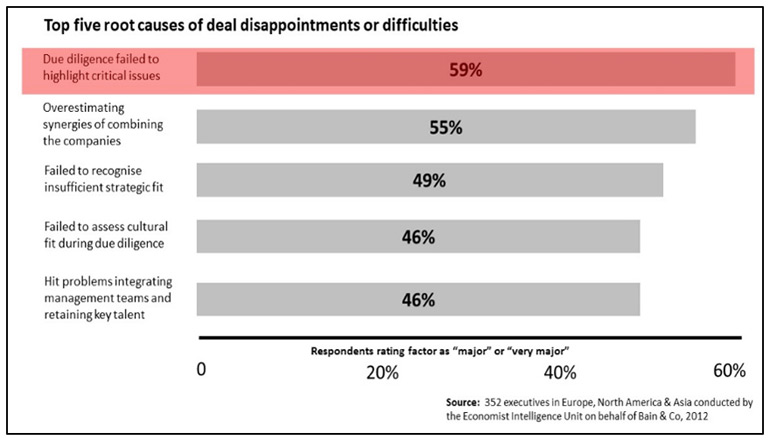

Once the Financial and Legal – and in some cases “Commercial” – due diligence is completed, acquirers often assume that all their major risks are identified (if not necessarily mitigated) and they’re in a position to finalise the business case and to proceed through the bid, negotiation, transaction and subsequent integration stages.

The flaw in this approach is that these traditional – and absolutely necessary – due diligence elements lack two critical elements: scope and comparison; that is, the missing comparative due diligence.

Scope

Generally, a business has a large number of ‘moving parts’: a unique corporate culture; particular strategies; a unique staff mix and ‘grapevine’; a deliberate digital presence; a change capability determined by a range factors (including recent change history); a unique (sometimes legacy) IT stack; and particular approaches to both Operations Management and Governance. Traditional approaches to due diligence do not cover the thorough investigation of this range of business-critical and integration-critical factors.

By having insights based on a wider range of hard data regarding these key characteristics of the target, acquirers have better information to make the core ‘bid / no bid’ decision, more accurately pitch price and terms, and construct a more realistic overall business case that captures the full scope of the integration task.

Comparison

Similarly, traditional approaches to due diligence do not compare the business-critical ‘moving parts’ of the acquirer and the target. The comparison enables more accurate analysis of strategic and cultural fit (crucial factors in M&A success), better business case development, and lower-risk integration planning. As well as highlighting potential showstopper risks, this process can also uncover ‘hidden gems’ (e.g. capabilities, processes, offerings) in the target that will provide leverage to the acquirer’s profitability and ‘sweeten the deal’ in the medium to longer term for their shareholders.

The inevitable result of two entities coming together is the creation of both a new culture and a new BaU: being deliberate about the design and functioning of the elements in and beyond the integration period will maximise the delivery of shareholder value.

Our solution: M&A intel

M&A Intel from Merger Transition Management addresses both the Scope and Comparison issues that constitute the missing comparative due diligence. M&A Intel has been developed from decades of M&A experience and reference to significant amounts of research on the factors that drive M&A success and failure.

M&A Intel is rigorous, comprehensive, low touch, and rapid. It complements – does not replace – the critical Legal and Financial due diligence efforts. M&A Intel helps acquirers to better manage M&A risk and to successfully deliver the M&A business case for their shareholders.

By Craig Henshaw, Director, Merger Transition Management