Actuaries Institute paper says financial institutions should measure their social condition

Ian Laughlin

Highlights

- The Hayne Royal Commission showed institutions have failed to understand and manage relationships with society and their associated social risks.

- This has resulted in great reputational damage and loss of social capital for those institutions.

- ‘Social condition’ is as important as ‘financial condition’ to the success and sustainability of an institution.

- The authors propose an annual Social Condition Report (SCR), in concept like the Financial Condition Report mandated by APRA.

- Boards, management and regulators would benefit from the Social Condition Report.

- The authors have written a mock SCR for a hypothetical major Australian bank.

Australia’s major financial institutions, many of them excoriated during the Hayne Royal Commission for their treatment of customers and other stakeholders, need to better understand their social risks and the social condition of their business.

In a major Dialogue* paper prepared for the Actuaries Institute, authors Ian Laughlin, a former deputy chair at APRA, and Hadyn Bernau, a principal at Finity Consulting, said the ‘social condition’ of a financial services business – the state of its relationships with its customers, employees, regulators, intermediaries, politicians and the wider community – is “no less important to a company’s long-term success than its financial condition”.

“The basic premise underlying this paper is that relationships with key groups in society are so fundamental to the success of a financial services business, and of such great value, that there should be a systematic approach to the management of those relationships,” the paper states.

“Financial services companies should commission a formal Social Condition Report to aid Board and management in their respective duties.”

The paper argues that management and boards often have a poor understanding of their relationships with the social groups with which they have relationships. “Those relationships are often quite poorly managed and nowhere near as strong as the organisation (and other parties) would desire.”

Social and relational events can quickly destroy significant business value. And “pedalling a lot harder” at the same tasks to correct deficiencies, including being more diligent, working harder, applying more resources, and improving reporting in the post-Royal Commission world, isn’t good enough. “We are sceptical about the effectiveness and efficiency of such responses,” the authors said.

Many social risks are being “poorly managed – perhaps not even being identified”. The paper states: “it is common for assessments of the current level of a risk (of whatever type) to be based on backward-looking measures – and this can give a very poor indication of the actual risk profile”.

The Social Condition Report concept is broadly modelled on the mandatory Financial Condition Report, a report highly valued by insurance company boards and APRA because it provides a comprehensive view of the financial dynamics of complex businesses.

The Social Condition Report could be as valuable for boards, ASIC and APRA because of the insights it will provide into the quality of the relationships with society, and the risks to those relationships.

Poor experiences observed in financial services, over a number of years, prompted the paper, which includes a proposal for the way in which financial institutions can systematically and rigorously measure and report on the quality of their relationships with key social groups.

The findings of both APRA’s Prudential Inquiry into CBA and the Hayne Royal Commission have reinforced the views of the authors. The proposal for a Social Condition Report provides a tool to help institutions respond.

The concept of a Social Condition Report includes identifying key groups and relationships, assessing and measuring the quality of those relationships and the risks to those relationships in the context of the board’s appetite for risk.

It involves a comprehensive and integrated assessment, and it would propose specific actions and defined objectives for management.

Placing a value on relationships is challenging but measuring social goodwill is possible. The paper proposes methodologies for doing this and gives examples. This includes the use of artificial intelligence and a structured system for assessing relationships on various dimensions.

“The Actuaries Institute is very supportive of this kind of thought leadership to address broader risks in our industries,” said Institute Chief Executive Officer, Elayne Grace.

Mock Social Condition Report

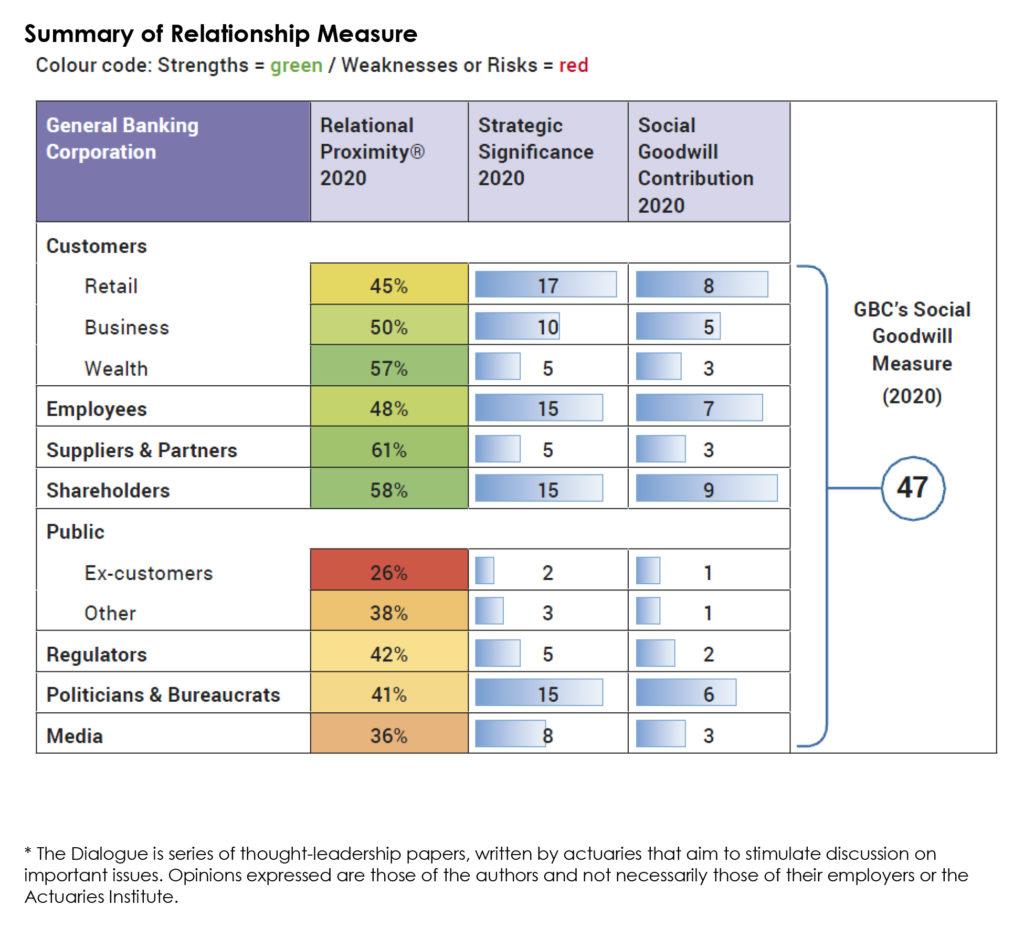

To illustrate their thinking, the authors have prepared a mock Social Condition Report for General Banking Corporation (GBC), a fictitious company, which is intended to be a major player in financial services in Australia. It can be accessed here.

Below is a simple extract from the mock report, a table showing the Social Goodwill Measure.

The Social Goodwill Measure is a weighted average measure of the quality of relationships across all key social groups (KSGs). The weights given to the various KSGs are based upon their relative strategic significance to the ongoing ability of GBC to achieve its purpose and execute its strategy.

This measure is useful for assessing the overall quality of the relationships in absolute terms, for tracking changes over time and for assessing the consequence of interventions to improve relationships.

A full copy of the paper is here.