The conversation – talking risk with clients (Part 1)

Risk insurance is important – it helps your clients and their families to cope financially should the unexpected happen.

Risk advice is an integral part of a financial plan, yet for many clients – and often, their advisers – it’s not a comfortable conversation. After all, who wants to talk about worst case scenarios? In this article, sponsored by Zurich Australia, AdviserVoice explores the importance of risk insurance and having the all-important risk conversation.

A lot of focus is given to accumulating and building assets; contributions to super, setting up self-managed super funds, the allocation of investment funds. As well as building assets, a financial plan needs to protect assets. Although a variety of investment tools can be, and are, employed in the protection of assets, risk insurance should also be incorporated into a holistic financial plan.

The role of insurance in a financial plan

Over the course of their lifetime, your clients expect to work and earn an income, buy and pay off a home, and grow assets both within and outside superannuation. At retirement, they expect to use those assets to fund their retirement. That’s the ideal scenario…in a perfect world.

However, it’s not a perfect world. Clients fall ill, get injured, sometimes die prematurely. Such events impact their ability to generate an income which, in turn, impacts their ability to pay off their home and accumulate adequate assets to fund their retirement. Worse still, many have to drawdown on assets to get through these unexpected periods.

The majority of clients are part of a family unit – anything that happens to them has a broader impact on their family, particularly when disaster strikes the primary breadwinner.

This is where having risk insurance is an essential part of a financial plan.

Risk insurance can replace lost income and provide payments to ensure clients don’t need to deplete their existing assets. Importantly, risk insurance can help keep your clients on the right financial course should the unexpected happen.

There’s a range of insurance options to help your clients mitigate risk and provide peace of mind for them and their family. Insurance needs vary due to a variety of factors: age, working status, income, family health history, and the number and age of any children.

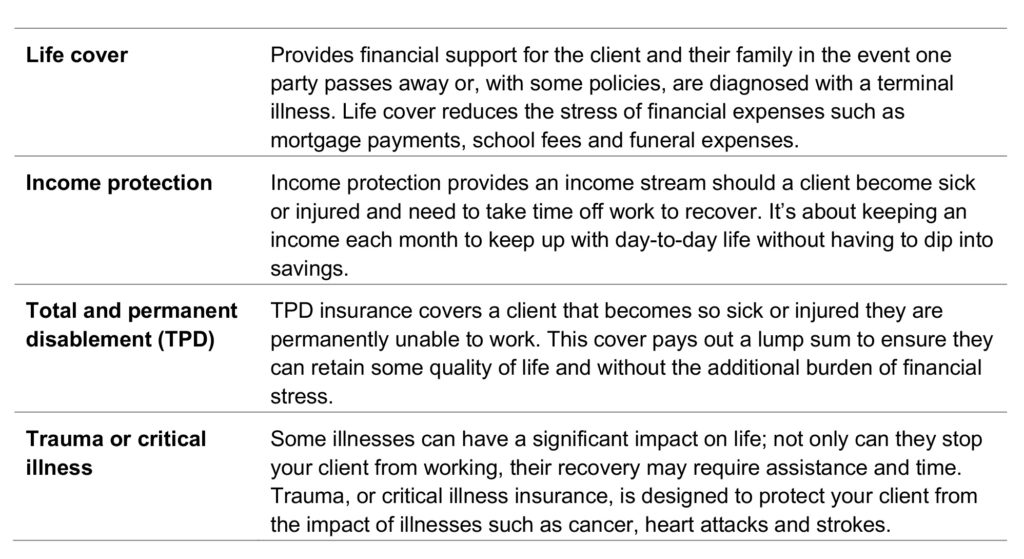

Personal insurances worth discussing with your clients include:

Australia’s underinsurance problem

In Rice Warner’s report Underinsurance in Australia 2017, it was found that the underinsurance gap remains significant for Australia’s working age population.

The research found that group insurance sold through superannuation makes up about 70% of all cover for Australians; it’s been the major factor over the last decade in reducing Australia’s underinsurance problem. Despite this, underinsurance remains a significant problem.

The amount of insurance cover held by Australians varies considerably. Rice Warner’s report provided the following estimates for insurance held by working Australians:

- Life cover – held by 94%, with an average cover amount of $344,500, around four and a half times median household income.

- TPD insurance – held by 81%, with an average cover amounts of $237,000, around three times median household income.

- Income Protection cover – held by only a third of the working population, with an average cover of 75% of median household income.

According to Rice Warner:

“The results of significant underinsurance not only restrict the lifestyle the claimant and their dependants can enjoy after an unfortunate event, it also incurs substantial cost to government mainly in the form of social security benefits.”

Could your clients afford to rely on social security alone in the event of serious illness or injury? As well as lost income, the cost of care can be significant.

Although Australia is a ‘lucky country’, many live with a false sense of security in terms of their health, and their capacity to cope financially, in the event of ill health.

Underscoring this point was a recent Zurich research study, conducted in conjunction with Oxford University, revealing the extent to which Australians see themselves as ‘bulletproof’. The same study found that – compared to their peers in other developed economies – Australians also have the most faith in the adequacy of social security to protect them in times of need, and unsurprisingly, the lowest interest in purchasing life insurance.

The cost of care

Illness and injury costs more than lost income and doesn’t simply happen to ‘other people’. Consider these statistics:

- Cancer represents 19% of the disease burden in Australia and is one of the most financially impactful – there are 380 new diagnoses of cancer every day in Australia

- In 2014–15 there were a total of 483,673 injuries in Australia, equivalent to 1,325 every day

- Over 600,000 Australians are living with coronary artery disease

- Nearly half the population will experience mental health challenges during their life time; the cost of depression averages $17,190 per individual.

While advances in medicine and treatment techniques are improving the survival rates across most conditions, there is a cost burden – estimated at $30 billion and upwards each year – which falls on all of us as individuals. And as good as our safety nets are, the out of pocket (OOP) cost impact to those affected by ill health can be crippling.

Depending on the condition, direct costs can range from hundreds to many thousands of dollars each year. In 2015/16 total health expenditure in Australia was $170.4 billion[1]. While State and Federal Government pick up the lion’s share of this burden, individual Australians – and their families and carers – still accounted for around $30 billion of this annual cost[2].

Indirect costs to the individual, such as time spent off work and time spent travelling to and from medical appointments, as well as indirect costs to families and carers also pose a significant burden. Carers often have to give up or reduce their working hours, compounding a family’s financial stress.

Consider the cost of these illnesses and injuries and imagine the impact on your clients and their families:

- The average lifetime cost for cancer sufferers can range from $20,360 to $95,460

- Cancer patients using drugs not supported by the PBS can face bills of up to $5,000 per month or more

- Each month there are 11 new quadriplegic events and 11 new paraplegic events; the lifetime direct cost of quadriplegia can exceed $11 million

- Around 20,000 Australians live with spinal cord injuries (SCI) and approximately 50 percent of those working prior to suffering an SCI will never return to the workforce.

These are often compounded by indirect costs – such as foregone income – impacting the sufferers and their carers. A report[3] investigating the impact on carers of people who have experienced stroke found that:

- 58% of primary carers of people with stroke and disability spend 40 hours or more per week in their caring role

- 21% report a decrease in income due to their caring role

- 24% incur extra expenses due to their caring role

- 31% have difficulty meeting everyday living costs.

Risk insurance is a vital part of the ecosystem that helps protect the financial, emotional and physical wellbeing of Australians. However, without a better understanding of how each of these systems interact, and a realistic appreciation of the true costs of poor health, we are ill equipped to judge the appropriate types and levels of support to best suit our circumstances, and to navigate a complex network of services and providers.

Zurich Australia’s Cost of Care study examines the incidence – and cost burden – of ill health in Australia. By drawing on aggregate health data, and individual case studies, the Cost of Care whitepaper serves to give financial advisers and their clients a clearer picture of the direct and indirect cost impacts to them and their families in the event of serious injury or illness.

In doing so, the study aims to give a greater understanding of the healthcare, social security and insurance ecosystem, in turn allowing more informed decision making about the most appropriate mechanisms to protect one’s financial wellbeing. It’s a solid entry point to having the conversation with clients about protecting themselves and their families from unexpected illness and injury.

Talking to clients

For most people, insuring their home, belongings, car or caravan against damage or loss is a given. It doesn’t require too much thought or discussion…the main concern is getting appropriate coverage to get the insured item repaired or replaced.

It’s much harder to repair or replace a person, yet so many people leave themselves unprotected – or underinsured – against accidents and illness that can affect anyone, anytime.

While it might not be a comfortable conversation to have with a client, it is important. You can start with a simple question:

“If the unexpected happened, if you became ill or sustained an injury, would your family be able to maintain their lifestyle without your income?”

For couples, that question should be directed to both parties.

In most cases, the answer will be no and may lead the client to having to sell assets.

However, there will still be those who are happy to game the system, take a risk, believe it won’t happen to them. Perhaps they have some cover in their super and believe that’s enough. Whatever the reason for their recalcitrance, you need to put that decision into some perspective for them.

You could, for example, share some odds.

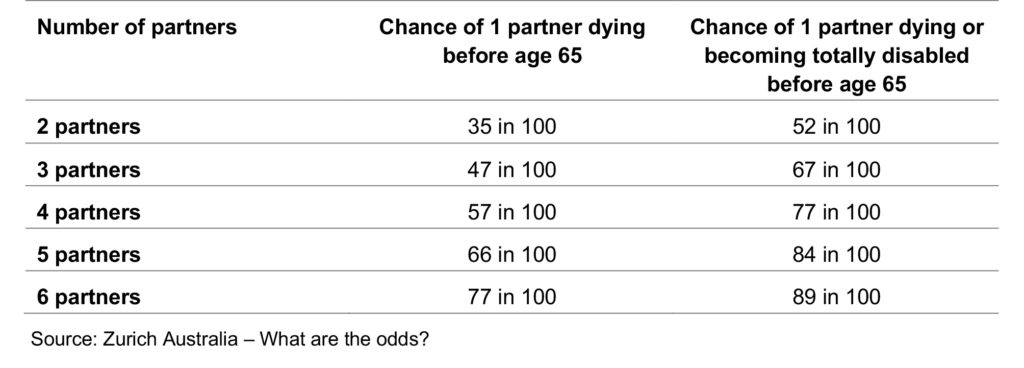

For those clients in a business partnership, what are the odds of a business partner dying or becoming totally disabled?

If perhaps it’s illness that will pique your client’s interest, some statistics from Zurich’s Cost of Care whitepaper may help put the need for risk insurance into perspective:

- Cancer represents 19% of the disease burden in Australia, and is one of the most financially impactful – in 2018, it was expected that 138,321 Australians would be diagnosed with cancer

- Cardiovascular disease (CVD), which covers a range of conditions affecting the heart and arteries, such as heart attack, stroke and high blood pressure, is responsible for one death every 12 minutes in Australia

- There are 96 stroke events every day in Australia, of which 29 are fatal.

Although your clients may feel uncomfortable facing their own mortality – or that of their loved one – it’s an important conversation to have. They’ll be far more uncomfortable if they’re unable to earn an income and meet their expenses. On top of that, illness and injury doesn’t come cheap – although there may be an expectation that Medicare and private health insurance covers the lot, there can be significant out of pocket costs.

For example, as highlighted in the Cost of Care whitepaper:

- The average lifetime cost of cancer for individuals aged 15-64 is $126,280

- On average, each heart attack costs $25,000 in total costs

- The healthcare cost of spinal cord injury ranges from $104,350–$106,850 per year – before the cost of equipment and modifications

- The lifetime cost of stroke is up to $32,411

- 21% of primary carers of people with stroke and disability report a decrease in income due to their caring role.

While many people can be put off by needing different types of insurance, it’s important to contextualise it and help your clients understand why and when they need a particular type of risk insurance.

There are a number of triggers for having – or revisiting – this conversation.

- The initial meeting

- Annual reviews

- Marriage

- Starting a family

- Illness or death in a parent, particularly when it’s an illness that can run in families

- Financial change – a new job, a return to work, starting a new business

- Divorce

If a client cannot support their family’s lifestyle should they suddenly lose their income, if covering medical or rehabilitation costs would create unnecessary financial stress, they need to consider risk insurance.

Whether you provide the advice, or refer them to a specialist risk adviser, it’s the relevant adviser’s role to engage with their clients about life insurance. They must determine the right type of cover and sum insured, one that’s appropriate to the clients’ needs and affordable to them over time.

As with all elements of a financial plan, it should be reviewed regularly to make sure it continues to meet the clients’ needs and takes into account any changed circumstances. Risk insurance is important because it helps your clients and their families to cope financially should the unexpected happen.

Read Part 2: CPD: The conversation – talking risk with clients (Part 2)

![]()

———-