Australian Fixed Income outlook- Domestic economy gets a kick start but global trade a risk

Domestic Investment Opportunities – credit still a focus

Western Asset, a leading fixed income investment manager affiliate of Legg Mason, in its recent midyear market outlook notes: “Trade negotiations have caused a substantial drag on sentiment, particularly over the past year. This has been feeding into softer trade figures and economic data, particularly manufacturing data, to the point where the US Federal Reserve (Fed) now has a dovish bent and markets expect more than one rate cut before the end of this year.”

The Western Asset investment team writes: The fear has long been that the ever expanding tit-for-tat on tariffs would lead to a major slowdown in trade, investment and activity globally, alongside possible geopolitical tension. Conversely, a resolution of trade tensions would be a welcome development for confidence and global economic activity. Most investment theses probably had not anticipated such a protracted standoff and there appears to be no resolution in sight.

Domestically, although inflation has consistently undershot the target in recent years, it is jobs growth, and the economic activity that follows, that is most likely to shape policy over the remainder of the year for the Reserve Bank of Australia (RBA) and the government. It would be positive if the government can be convinced to ease the fiscal purse strings, particularly now that traditional monetary policy has basically run its course and the Government is returning to budget surpluses.

A drop off in jobs growth, while the participation rate remains at or near record levels, would lead to a higher unemployment rate, hence the urgency by the RBA to keep activity high. A greater concern for policy makers is if the economy fails to return to moderate GDP growth by the end of the year after the past three lacklustre quarters.

Australian Rates – RBA likely on hold to assess recent cuts

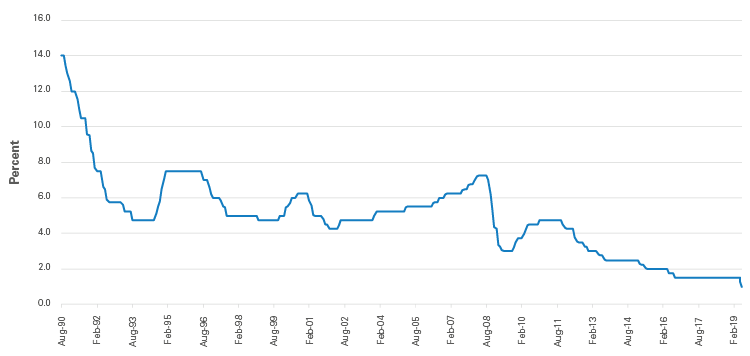

The Reserve Bank of Australia (RBA) cut rates by 25 bps to 1% at its July meeting. This is not only the record low for the RBA, but the first consecutive cut in interest rates in Australia since 2012. Looking forward, the main question is whether the RBA will cut again in the short-term. We believe that they have bought some time, but employment growth is the key now.

Chart 1: RBA cash rate

Source: Reserve Bank of Australia, as at 5 July 2019.

With the major banks having passed through between 40 and 45 basis points (bps) of the 50 bp rate cut and with parliament passing the personal income tax cuts, consumers will have considerably more disposable income. Add to this the loosening of prudential settings for banks in the testing of new borrowers’ ability to service a mortgage and you have three measures that are providing a considerable economic stimulus. With house prices appearing to have found some support recently post the election and the “no change” result to the tax treatment of property, we should see an improvement in sentiment in the second half of the year.

Our base case is that the RBA will sit tight for a few months at least, and quite possibly for the remainder of 2019. This should enable the RBA to assess the impact of the cuts, as well as any contribution from fiscal policy towards improving economic growth, employment and ultimately inflation.

Domestic investment 0pportunities – credit still a focus

Monetary conditions globally remain extraordinarily accommodative, particularly as more recent pricing indicates expectations that the Fed will cut the funds rate more than once by the end of the year. Most other major central banks have also become increasingly dovish.

We believe such conditions will continue to favour spread sectors and in our opinion, these sectors should be the best-performing fixed-income assets and remain our major theme. Nonetheless, we are highly critical in our assessments of credit, deal structures and pricing.

We maintain an overweight to corporate bonds with a concentration in large financials, property trusts and utilities, focused at shorter maturities to manage spread risk. We may seek to add selectively where market volatility has forced spreads wider than credit fundamentals would justify or as new opportunities present.