Ethics and your referral partners

Trust should be the cornerstone of all client relationships.

Most financial advice practices have referral partners they send business to, or receive business from. You may also use any number of third party outsource providers for non-client facing elements of your service offering. This article examines your obligations with respect to those relationships and FASEA’s Code of Ethics.

Ethics and trust go hand in hand. They are mutually reinforcing; improving one improves the other, but conversely, damaging one damages the other. A large part of building a successful financial advice business is building a client base and building trust with that client base – after all, who would provide their intimate financial details with someone they didn’t trust, and rely on them to act in their best interests to help them meet their financial objectives?

Trust should be the cornerstone of all client relationships. While it can’t be built in one meeting, it can be destroyed quickly.

Building trust

Trustworthiness is one of FASEA’s five values that underpin its Code of Ethics and ethical standards. According to FASEA[1]:

Acting to demonstrate, realise and promote the value of trustworthiness requires that you act in good faith in your relationships with other people. Trust is earned by good conduct. It is easily broken by unethical conduct.

Trust requires you to act with integrity and honesty in all your professional dealings, and these values are interrelated.

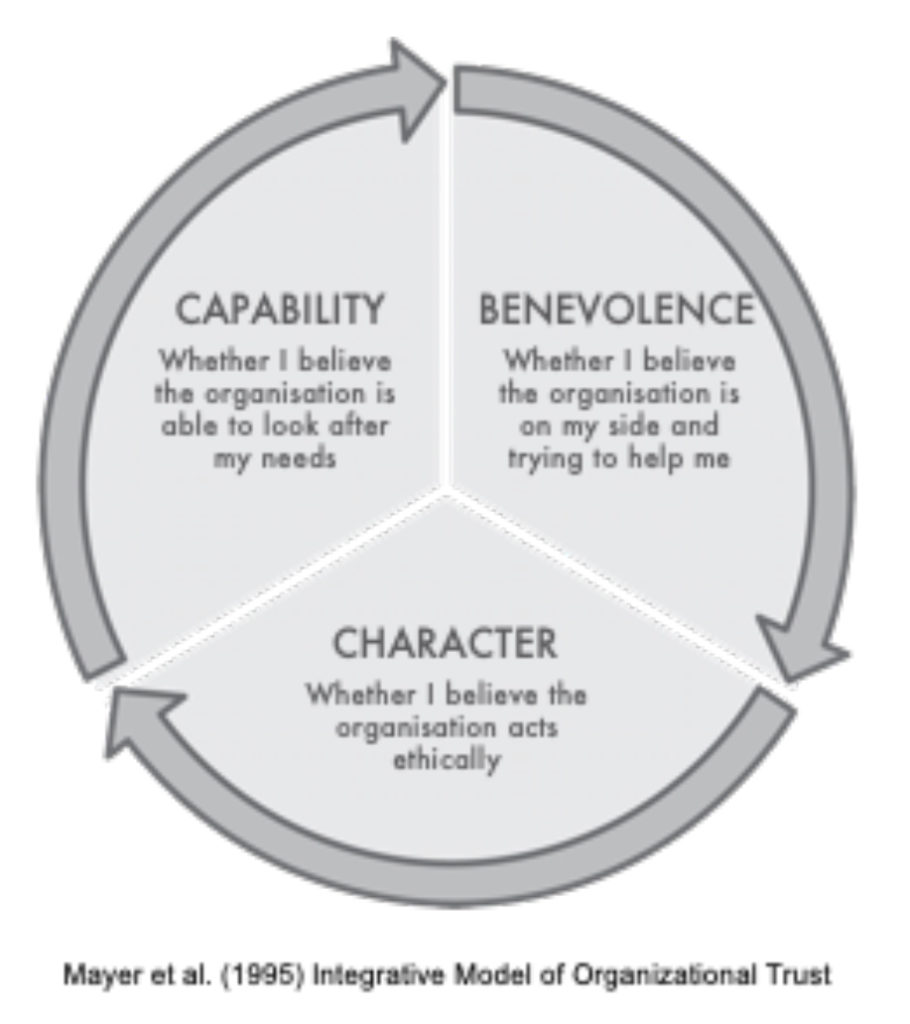

Figure one illustrates a model of organisational trust that is relevant for financial advice practices and the myriad of corporate partners with which it may have a referral relationship or an outsource arrangement.

Figure one: Integrative Model of Organisational Trust

The model posed by Mayer et. Al. (1995)[2] suggests that trust is comprised of three key components:

Capability

Do you have the skills, competencies, and other relevant abilities to service your clients? Do any of your referral partners have the requisite capabilities in their field of expertise? Likewise, does each outsource partner offer the appropriate services to look after your clients’ needs, rather than simply a cheaper option? After all, you won’t be judged solely on your contribution, you’ll be judged on the sum of the parts.

Competence is also one of FASEA’s core values. It states:

Acting to demonstrate, realise and promote the value of competence requires you to have regard to the knowledge, skills and experience necessary to perform your professional obligations to each of your clients. It requires you to assess the professional services required by each client with regard to their individual needs, priorities, circumstances and preferences, expressed or implicitly identified as the subject matter of the financial advisory engagement.

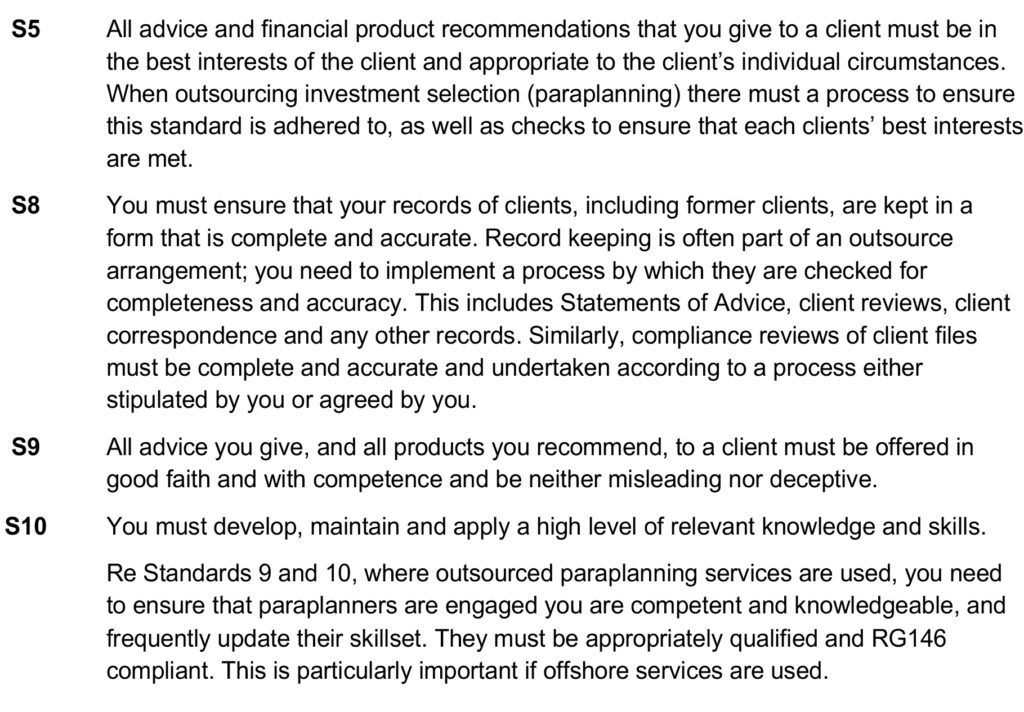

While capability is implicit in several FASEA standards, it is directly linked to two standards:

S9 All advice you give, and all products you recommend, to a client must be offered in good faith and with competence and be neither misleading nor deceptive.

S10 You must develop, maintain and apply a high level of relevant knowledge and skills.

Benevolence

Defined by Mayer et. al. as ‘the perception of a positive orientation of the trustee (financial adviser) toward the trustor’ (client) – or, in other words, your client believes you are on their side and working to help them. Likewise, they would expect referral partners and outsource providers to likewise deliver the same degree of benevolence.

Benevolence is consistent with fairness, another of FASEA’s values:

Acting to demonstrate, realise and promote the value of fairness requires that you bring professional objectivity to the task of engaging clients professionally, and when recommending financial products and professional services.

Benevolence permeates most of FASEA’s ethical standards, but is explicitly captured in those that reference acting in your clients’ best interests:

S2 You must act with integrity and in the best interests of each of your clients.

S5 All advice and financial product recommendations that you give to a client must be in the best interests of the client and appropriate to the client’s individual circumstances.

S6 You must take into account the broad effects arising from the client acting on your advice and actively consider the client’s broader, long-term interests and likely circumstances.

Character

This term is used interchangeably with integrity in this model, and is consistent with the remaining FASEA values of honesty and diligence. The relationship between integrity and trust involves the client’s perception that the financial adviser adheres to a set of principles – or ethics – that the client finds acceptable.

FASEA’s value of honesty references integrity:

Acting to demonstrate, realise and promote the value of honesty requires that you conduct yourself with integrity in all your professional dealings with your clients and with all others that you engage with in the professional setting.

When a client believes a company is ethical and is committed to ethical business practices, a higher level of trust is likely to develop.

There’s no doubt that building trust with your clients is important for your business. It’s imperative for client retention and it’s a requisite for referral business. As illustrated by the model in figure one, integrating ethical practices in your business will increase your ability to build and maintain trust with your clients.

That’s all well and good for those elements of your business you control. What about your referral partners or outsource suppliers? What happens when you refer business to other finance specialists: accountants, stockbrokers, risk advisers, mortgage brokers and others. A wrong step by any one of these providers can undermine trust in you and your business, and potentially breach FASEA’s Code of Ethics.

Referral partners

FASEA Standard nine requires advice given and product recommendations to be offered in good faith and with competence. Further, standard ten requires advisers to develop, maintain and apply a high level of relevant knowledge and skills. Given the broad range of financial needs any one client may have – and licensing requirements – it’s not unusual for financial advisers to refer clients to other finance specialists, either within their own practice or outside of it.

These relationships are often established at the licensee level and you’re told who you need to deal with for what issues. A negative experience with a referral party may not only reflect badly on you and your business, it can alter your relationship with your client. At its worst, the interaction can result in a breach of FASEA’s Standard of Ethics and come back on you if you fail to act on an issue.

Standard three

When dealing with referral partners, the first thing to note, is Standard 3:

S3 You must not advise, refer or act in any other manner where you have a conflict of interest or duty.

While this standard is primarily focused on conflicts of interest, it also means that where a referral arrangement exists, you must not be remunerated for the referral. This holds true for the reverse situation, where the referral is to you.

According to FASEA’s guidance, you will breach Standard 3 if “a disinterested person, in possession of all the facts, might reasonably conclude that the form of variable income (e.g. brokerage fees, asset based fees or commissions) could induce an adviser to act in a manner inconsistent with the best interests of the client or the other provisions of the Code.”

There’s been a lot of debate about this standard. In fact, the Association of Financial Advisers (AFA) claims: A ban on the receipt or provision of referrals for a benefit, including any expectation of reciprocal referrals, will fundamentally challenge existing practices and impact upon the flow of new clients for many businesses that rely upon referral arrangements.[3]

While debate about aspects of the standards enumerated in FASEA’s Code of Ethics will no doubt continue, as they stand are they enforceable by law.

It’s important to note that Standard 3 refers to actual conflicts of interest between the duties you owe your client and any personal interest or duty you owe another individual or organisation. According to FASEA’s guidance, you would not breach Standard 3 merely by being a duly remunerated employee of an entity that lawfully provides retail financial advice and services and referring to a specialist within that practice. This extends to profit sharing. You are, of course, required to ensure the provision of advice and services are in the best interests of your client and comply with the other provisions of the Code.

Let’s examine some of the relationships that might exist between financial advisers and referral partners.

Accountants

This is one of the most common referral arrangements. In fact, businesses have been built around the model of accounting practices buying financial advice businesses, and vice versa. While there’s been a lot of regulatory to and fro over the years, the synergies been tax advice and financial advice are evident.

As well as been synergistic, there are also areas of overlap. For years, accountants have advised clients about investment strategies to manage and mitigate tax. Agribusiness, a model built on tax deferred income was a favourite with accountants but, while potentially providing a tax benefit, it was not always in the client’s best interest from a holistic perspective. Ultimately, although it may have provided tax benefits to some clients, the implosion of the sector caused significant loss for many investors.

Accountants have also long been proponents of self-managed super funds (SMSFs). While in many cases it may be an appropriate strategy for the client, there may be times that you question its validity. Irrespective of the relationship with the referral partner, your client and their best interests must, at all times, come first.

If there’s a scenario where a client’s accountant makes a recommendation about an investment or a strategy, even if it’s tax related, you have the right to question it if it seems not to be in the client’s best interest. While there’s a case for making enquiries of a strategy even if the accountant isn’t a referral partner, in the situation where there’s a formal referral relationship it’s even more important.

It may be because you have a better understanding of the product, or because of your in-depth knowledge about the client’s financial objectives and their risk profile. An accountant’s product or strategy recommendation may be too risky for that client or inappropriate in when you take their total portfolio in account. It’s important to call it out and discuss the whole picture with the referral partner; that way, you can agree on what’s best for the client, will help them achieve their financial objectives and within the agreed risk parameters.

Stockbrokers

Not all financial advisers are licensed to recommend direct investments, or may have limitation on what they can recommend. A number of broking firms have ‘intermediary desks’ established to work with financial advisers.

Others may have the requisite licence, but lack the time to keep up with the research to ensure they meet their obligations under Standards 5 and 9, to understand the intricacies of each security they recommend. Others may simply use a broker to implement trades. Irrespective of the level of service, the trust connection between adviser and broker is important. It’s imperative for your relationship with the client that the broker acts in their best interest at all times and does not make recommendations or implementations that contravene FASEA’s Code of Ethics.

If the referral comes from you, whether the broker is providing advice or implementation only, you need to ensure it’s appropriate for your client. Referring a client to a business or individual where their best interests are not met and ethical standards are not adhered to can have negative repercussions for you.

Mortgage brokers

Mortgage brokers have a particular skill set and there may be times you need to refer a client for loan assistance. Their renumeration typically comes from the financial institution where they place the business and, in most cases, they are paid an upfront commission and a trail or ongoing commission for the business. These commissions are paid out once the loan settles and are based on a percentage of the loan amount.

The 2018 Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry uncovered a range of examples where mortgage brokers encouraged people to take loans larger than they could comfortably service, the implication being this was for their own gain.

As a consequence, in January 2020, the Federal Government passed legislation to create a duty for mortgage brokers to act in the best interests of consumers. Where there is a conflict, brokers must prioritise consumers’ interests when providing credit assistance.

This ‘best interests duty’ will come into effect from 1 July 2020.

Risk adviser

Risk advice is a specialist area. Some financial planning practices may have an in-house risk specialist, others outsource to a business focused on risk. It would be expected that in-house risk advisers would adhere to a practices’ approach to managing ethics in a way that’s consistent with the FASE code; however, that needs to stipulated and not assumed, as a failure to act accordingly can have negative repercussions for the broader practice, as well as individuals within it.

The hard conversation

Where an outsource model is used, it’s imperative that there’s an agreement between you with respect to the risk advice provided. You need to ensure that it’s appropriate for each client, consistent with their estate plan and will meet their needs as and when required.

With all referral agreements with financial specialists, you need to stipulate your requirements for their conduct. If a formal agreement is not already in place, or if it does not cover the requirements stipulated in FASEA’s Code of Ethics, that needs to be established as a matter of priority. You know how you expect your clients to be treated and the quality of advice you expect – don’t assume that’s what will be provided.

It’s important to review the advice provided and where you have doubts or queries about its appropriateness, have a conversation with that referral partner. It may be a hard conversation, particularly if they feel you are questioning their professionalism. However, if you believe that a recommendation is not in that client’s best interest, you need to act.

Explain your concern in the context of the client’s financial objectives, risk profile, estate plan or existing portfolio, whichever is the most relevant for the conversation. By making the client central to the discussion, it becomes less personal and more focused on achieving positive outcomes for your mutual client.

Outsource partners

It’s hardly surprising that many advice businesses look to outsource some of their business processes. The paperwork obligations that arise every time they provide personal financial advice are onerous. Any of the work that support staff in your office can do can be outsourced. Typically, those activities that are client facing or revenue generating are kept in-house.

A Google search of outsource businesses servicing the advice community show that you can pay other businesses to undertake a myriad of business processes, including:

- Document preparation, including SOAs and regular reviews

- Data input and presentation

- Paraplanning

- Portfolio management

- General administration, including virtual assistants

- CRM management

- Client correspondence and reporting

- Business functions such as finance, marketing, IT and compliance.

There are three most common outsourced business models available to you – freelancers, staff leasing and fully managed services.

Freelancers – are generally a low cost option, but can be higher risk. Through a variety of online service providers, you can get freelance individuals on a project base or on an ongoing basis. While there’s no doubt you can find some excellent people freelancing, you need to undertake background checks as you would for an employee, to ensure they have the appropriate experience and credentials for the role. The greatest risk is continuity if they choose to walk away.

Staff leasing – often used by an outsource partner to provide a range of services for your business, whether in Australia or offshore. The outsource provider handles the specified business processes and you retain full control of the staff and work quality. On the plus-side, it allows you to build your own remote team dedicated to your business and gives you greater control.

Fully managed services – this is where the outsource provider handles everything for you. You provide a list of requirements and key performance indicators; they do the rest. If you’re looking for a hands off solution, this is ideal; on the downside, the outsource provider will control your business processes.

The Google search also showed that while outsourcing can be a cost effective measure for scaling a practice, they are often offshored, which can lead to less control. Outsourced staff, whether based in Australia or offshore, represent your business and your brand. You want it to reflect your practices, which should include your adherence to FASE’s Code of Ethics. Therefore, when choosing an outsource provider, it’s important to choose one that aligns with your business vision and values.

Questions to ask a prospective outsource provider

Once you have determined which parts of your business you’d like to outsource, using FASEA’s Code of Ethics as a framework, you should ask the provider how they will conform to each standard. Providing scenarios is a good way to test the provider’s approach to ensuring compliance and dealing with any breaches.

Further, encapsulating the Standards in the provider’s key performance indicators can be a good way to manage the outsource provider’s adherence to the Code. This should form part of the outsource provider’s regular reporting to you.

Governance practices should also be reviewed. How is the personal information of each client protected? What checks and balances are in place to ensure there’s no identity theft or exposure to cyber-attack?

You should also ask about staff retention. A firm that experiences high staff turnover is less likely to be able to consistently align to your values and lead to increased risk of breaching the Code.

Staff training is also an importantly element. You need to ensure there is support for appropriate ongoing training to ensure the work they do for you meets not only your requirements, but those requirements applied by law.

Finally, where you offer staff training sessions around ethics, it would be useful to see if you can include relevant staff from your outsource partner in these training sessions.

Why is this important?

Importantly, we you outsource, you need to stipulate the process and clearly say ‘this is the way we want things done’ – and the way you want things done must include meeting your obligations under FASEA’s Code of Ethics. In particular:

The following case studies are fictitious and use the current environment to create scenarios loosely based on past cases that have been before the Australian Financial Complaints Authority (AFCA) and its predecessor organisations.

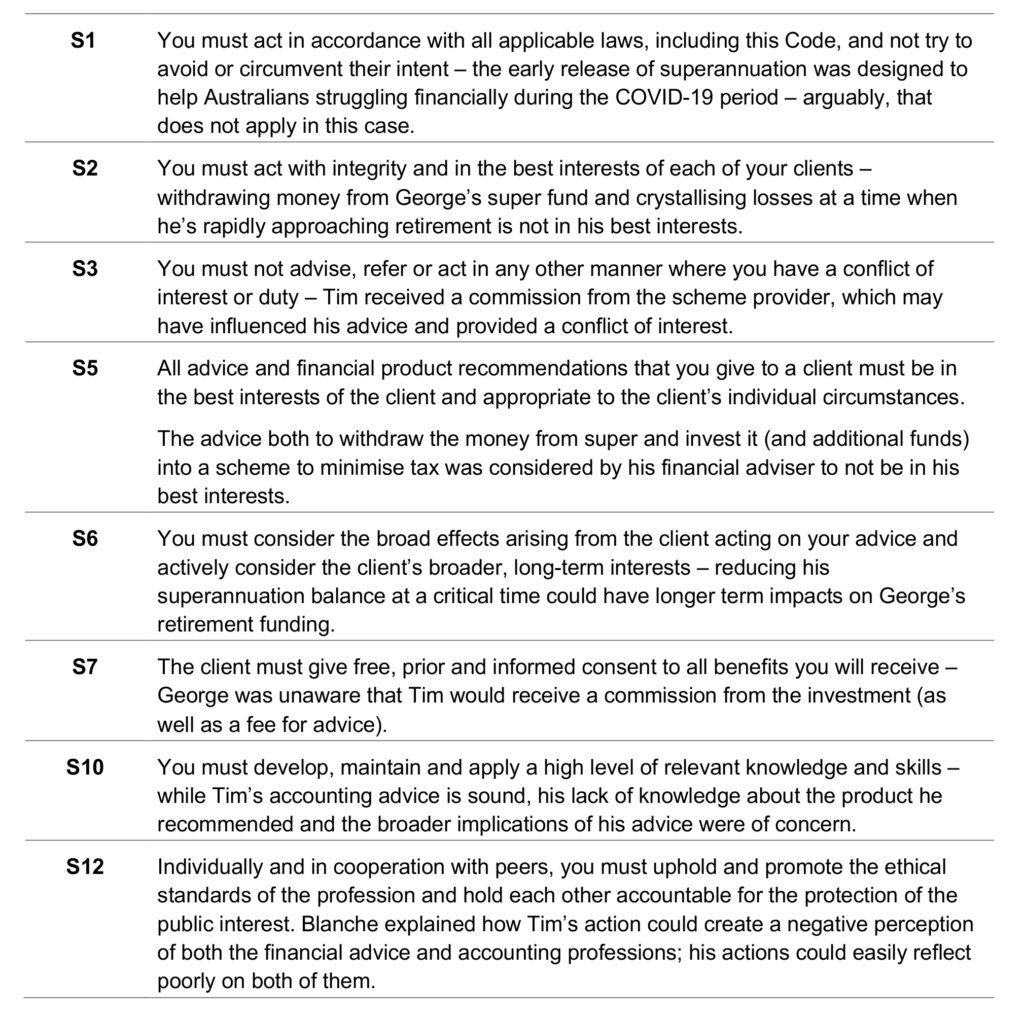

Case study one: a tax effective investment scheme

Blanche Green is a financial adviser with many years’ experience. Her financial advice practice BG Financial Planning works in tandem with ABC Accounting and had done successfully for many years.

One of her clients, George, runs a successful business and is nearing retirement. ABC Accounting has looked after his accounting needs for many years and between his adviser and accountant, he’s been working on a business succession plan. His accountant retired quite suddenly due to ill health, and a new graduate, Tim, has taken over his affairs.

In a review meeting with George to discuss the succession planning, Blanche discovers that Tim has not only recommended that George take advantage of the government’s early release scheme for superannuation, he has implemented the $10,000 withdrawal. The intent is do so again post 1 July 2020. George has no pressing need for the money and given his approaching retirement, it’s not an opportune time to unnecessarily crystallise losses in his superannuation portfolio. As George had invested heavily in his business over the years, his superannuation portfolio was not substantial.

When Blanche quizzed George about the withdrawal, he admitted Tim had invested the money in a ‘tax effective’ investment scheme, akin to agribusiness investments of days gone by. George sheepishly admitted he’d invested a further $20,000 in the scheme and planned to add to the investment once the next super tranche was released after 1 July.

Blanche contacted Tim to discuss his advice. She was concerned about the withdrawal from his super account and also about the scant information she could find about the tax effective investment scheme into which George had invested. While Tim was able to describe its tax effectiveness – a description provided by the investment company – he was unable to clearly articulate how it worked or how it invested. He did not disclose, until specially asked, whether he received a financial incentive to place the investment. He did. He had not informed George of this arrangement.

Blanche explained to Tim how his advice could impact George’s retirement plans and also took him through FASEA’s Code of Ethics, to explain how his advice had potentially breached it, as follows:

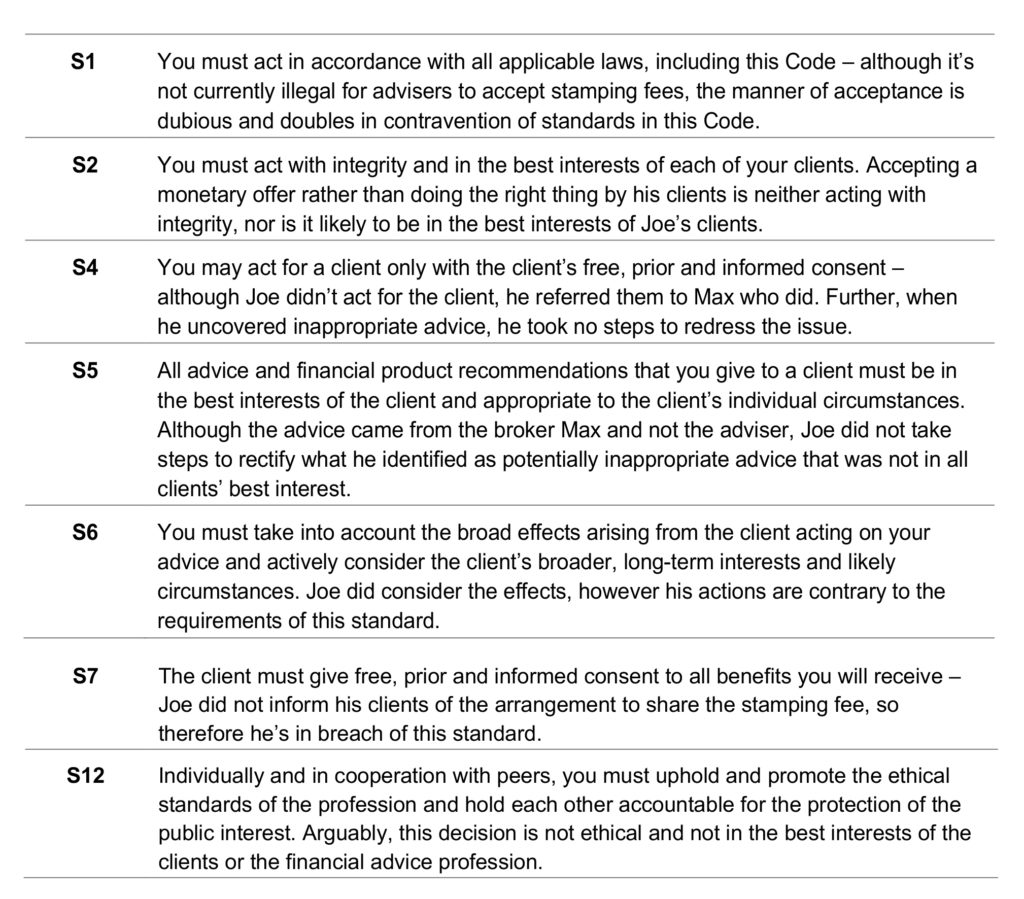

Case study: stamping fees

Stamping fees have been in the media a lot recently. ASIC is currently undertaking a review of the stamping fees – or commission by another name – paid on to financial advisers and stockbrokers on investments listed investment trusts (LITs) and listed investment companies (LICs). It’s believed these fees should be eliminated to stop the selling of what can be inappropriate investments to clients; the concern is, some may be motivated to recommend the product because of the stamping fee.

In this scenario, Joe is a financial adviser who is not licensed to provide advice on direct shares. He has a referral arrangement with Max, a stockbroker at BJ Was Brokers, to whom he refers some of his clients who want to invest directly in the sharemarket. Joe’s clients are typically older and like to invest in dividend paying, solid, blue chip stocks.

Max had sometimes invested clients in established LICs such as AFIC, that hold a portfolio of quality blue chips. This often happened when clients did not have sufficient funds for adequate diversification.

Joe received a transcript of investments from BJ Was and noticed a number of clients had a holding in a new LIC with which he wasn’t familiar. Some had sold shares in AFIC or blue chip stocks to make the investment. When he looked into the new LIC, he saw it was a higher risk product, one that invested in smaller, more speculative companies, and which didn’t provide the dividend income these clients generally sought.

When Joe questioned Max, after some dithering he offered to share the stamping fees he’d received from the LIC, which amounted to some thousands. Joe had two choices – act ethically and demand these fees be repaid to clients and steps taken to restore their portfolios to appropriate holdings or go along with Max’s suggestion. He chose the latter and, in doing so, potentially breached the following FASEA ethical standards:

Case study – the outsourced paraplanner

ABC Financial Advice Services was located in an area of Sydney that had experienced gentrification and an influx of professional couples. It was growing quickly and the business principals, Jeff and Mike, decided that by outsourcing some of their business processes, they could scale the business more quickly without having to add a large number of staff.

Jeff was charged with finding some potential outsource providers and they held a ‘beauty parade’ to see what each had to offer. They settled for ABC Outsourcing, with staff based offshore, as they could get a significant amount of their business processes dealt with at a very reasonable cost. One of the processes they outsourced was paraplanning.

As part of the due diligence process, Mike and Jeff made sure that the paraplanners provided by ABC Outsourcing had appropriate Australian-equivalent accreditation and qualifications, were RG146 compliant and there were processes in place to ensure ongoing professional development.

Once satisfied this was the case, as ABC Outsourcing met the other criteria required, the company was appointed.

At the six month review, Mike and Jeff expressed their satisfaction with ABC Outsourcing. It had met the KPIs set and in the case of paraplanning, provided quality and timely service. However, not long after, they noticed a sudden decline in the quality of Statements of Advice and reporting. They were undertaking a number of client reviews and the information coming in was incomplete and inaccurate. After making several enquiries, they discovered the initial high quality paraplanners had been replaced by inexperienced and unqualified staff; staff that evidently were paid less by ABC Outsourcing.

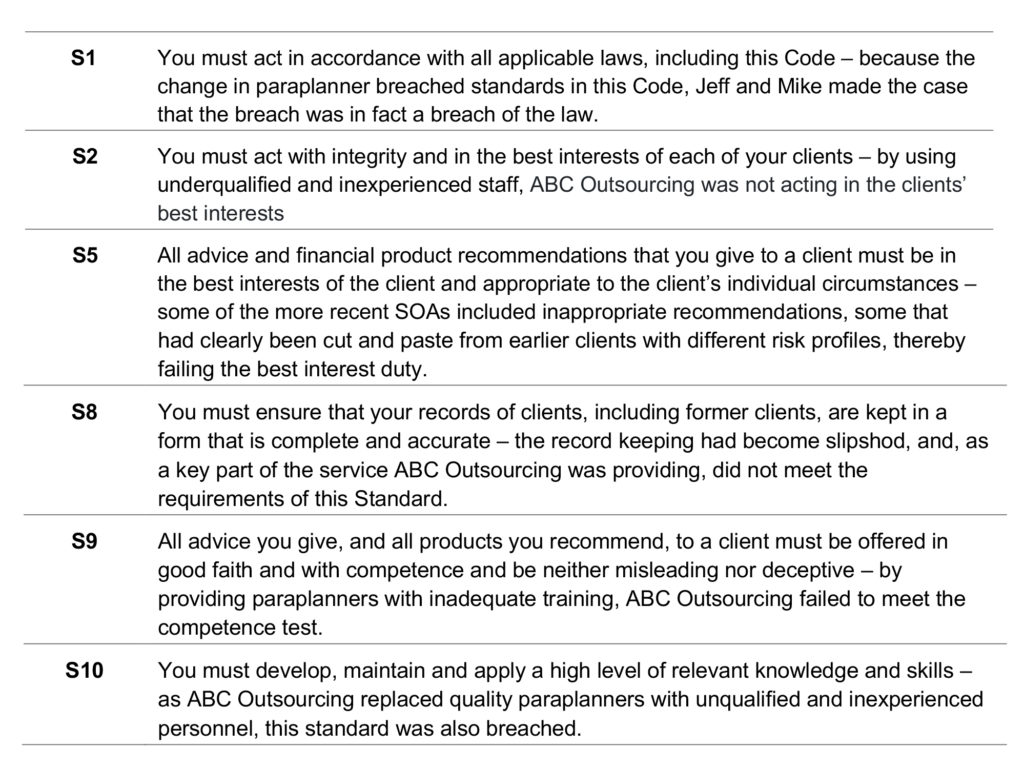

Because they had used FASEA’s Code of Ethics to frame the KPIs agreed with ABC Outsourcing, they were able to refer to them when detailing the issues arising from the change in paraplanning staff. In particular:

Although you can outsource some of your business processes, or refer to other specialist practitioners, you cannot outsource or refer your ethical obligations. At every point in the advice value chain, you need to ensure your clients’ best interests are being met and, where this is not the case, take appropriate action to rectify the situation as soon as practical. That way you can look your clients in the eye and know that you have consistently behaved with professionalism and embraced the ethical code that frames your industry.

———-