Halley’s Comet and Life Insurance economics 101

Edmund Halley also worked in the field of actuarial science – which arguably has been more important for society.

Edmund Halley (1656 – 1742) was a remarkably talented man of science, who made important contributions to mathematics, physics, and of course, astronomy. A peer of Sir Isaac Newton (apple, gravity etc), Halley’s most public legacy is the comet named in his honour after he correctly predicted the frequency of its appearance (roughly every 75 years). But it is his work in another field – actuarial science – which arguably has been more important for society. In 1693, using demographic data for a relatively unknown Polish city, Halley developed the first life table[1], thus creating the foundational basis for life insurance as we know it.

The ability to predict and price risk is central the economics of life insurance. This article will examine the economic framework for life insurance, including the fundamental business framework as well as the interrelationships between the many components of that framework, including product design, claims, underwriting, and reinsurance.

By developing a deeper understanding of the financial dynamics of life insurance industry, and the external forces at play, financial advisers will be better equipped to understand the way insurers respond to these forces, including through product design and pricing changes.

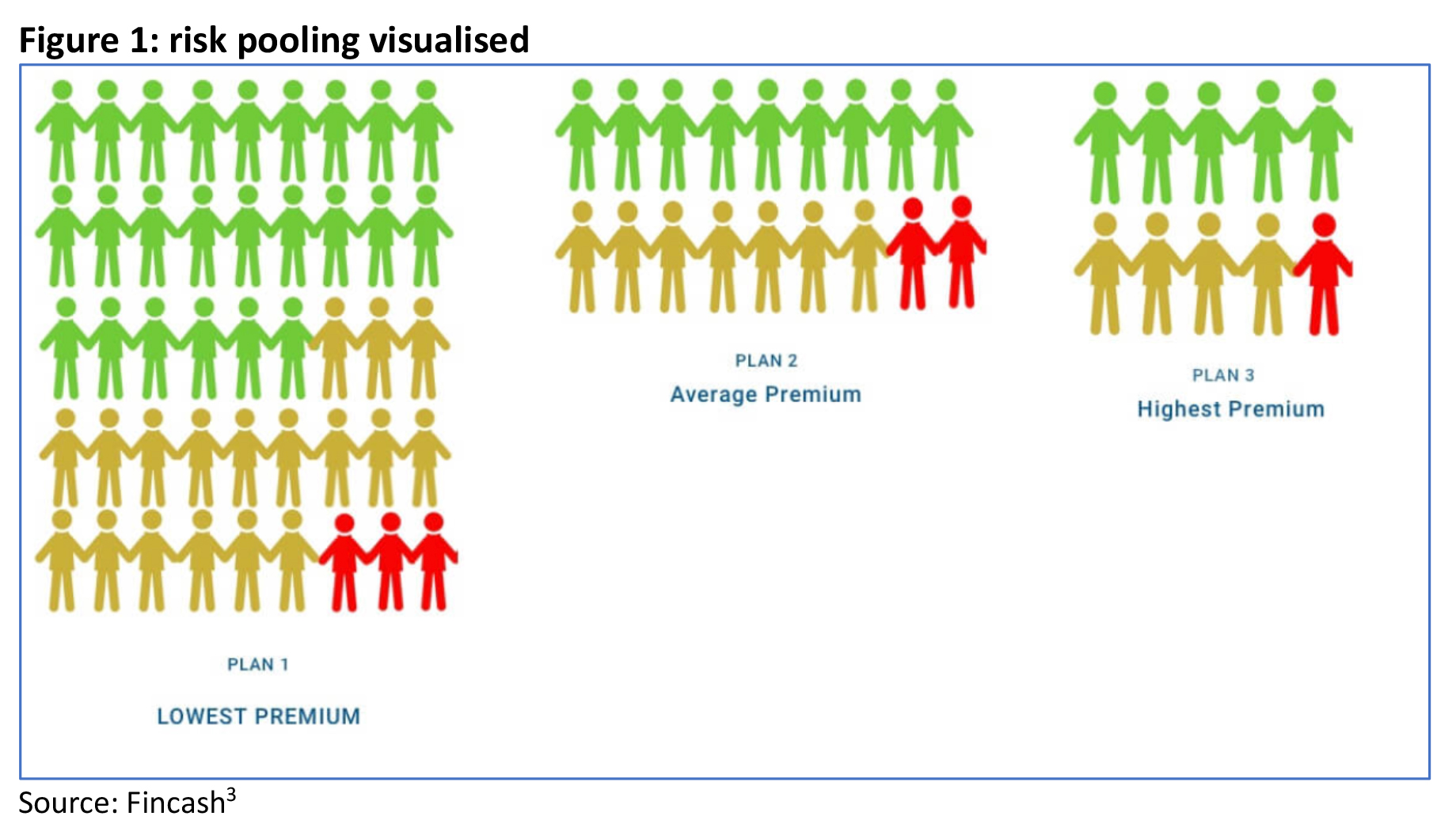

Today’s insurance is brought to you by – risk pooling

A core concept within any type of insurance (including life and general) is the risk pool. By aggregating together people with similar risks, those risks can be spread. A frequently cited example is that of ancient shipping merchants[2], who would come together and effectively pool and share the financial risks of one of their boats and/or cargo being lost at sea. Simplistically, the bigger the pool became, the more the risks were shared and the lower the contribution each participant in the pool (i.e. the premium) needed to pay for the pool to remain sustainable. Figure 1 demonstrates this concept neatly.

By understanding the concept of risk pooling, it is easy to see the importance of related concepts such as controlling admission of people into the pool based on their individual risk profile (underwriting), tailoring the contribution made by each pool participant to their risk profile (pricing), and the volume of people encouraged to join the pool (distribution).

Below we will explore these concepts, and more, specifically as they apply to the economic framework for life insurance.

The basic financial flows of life insurance

A simple summary of the main financial flows into – and out of – life insurers is shown below.

The profitability – and sustainability – of life insurers thus follows as an extension of the relative size of inflows versus outflows.

Whilst each company is different, an illustrative rule of thumb for life insurance financials in the retail channel is shown below:

Based on long term historical averages for the retail channel, this breakdown shows that for every dollar of premium paid to a life insurer, roughly 50 – 60 cents is paid out in claims, 20 – 25 cents is paid in commissions, 10-20 is paid in other running costs, leaving a profit margin of 10-15%.

Several important aspects of this illustrative example are worth bearing in mind:

- It is an illustration of a long term ‘equilibrium’ state, and is not reflective of the current profitability challenges facing Australian life insurers;

- Long term profitability of 10-15% is low relative to other sectors of the Australian financial services industry (partly explaining bank attitudes to life insurer ownership), but high relative to other countries[5] (partly explaining the attractiveness of Australia to overseas insurers).

- For group life, a much bigger proportion of premiums is returned as claims[6], as the operational and distribution costs for group schemes are relatively lower.

How life insurance products are priced

While Life tables are much evolved from Halley’s first effort – thanks to centuries of claims experience and superior data availability) – the underlying principle remains the same, and the starting point for anyone pricing risk products will be mortality data (life cover), and morbidity data[7] (TPD, trauma, income protection). These ‘rates’ of morbidity and mortality – which reflect the theoretical risk of someone dying or suffering disablement or illness – are then ‘loaded up’ with allowances including running costs, distribution costs, and risk factors related to specific target market selections and product features. Rates can also be loaded with risk buffers to reflect a lower risk appetite on the part of the insurer, or the higher risks inherent in truncated underwriting processes (for example, those used by many direct insurers).

The interplay of segmentation, expenses, shareholder expectations and risk appetite – and how these vary between insurers – explains why premium rates, for essentially similar types of cover, can vary so much across the market.

For example, if Insurance Company A concentrates on providing life-insurance solutions to those in their late twenties, they may be offering cheaper prices, as well as more lenient underwriting, than Insurance Company B, which is focusing on providing policies to those in their mid-forties.

Life Company C might target blue-collar workers. That may mean it can offer lower prices while still achieving reasonable profits at the height of a mining boom but must take the risk of its revenue and profit margin taking a hit in a bust. Likewise, Insurance Company D might offer health-and-wellness options, which means it will need to price its product differently to a competitor not offering these options.

Alternatively, if an insurance company’s shareholders are willing to accept a lower rate of return, it has the flexibility to price its products at a lower rate and possibly gain market share. (However, insurer reputation means that discounting doesn’t automatically translate into more customers).

Accurate risk pricing – that is, pricing that reflects the true risk of an individual making a claim – is critical to ensuring the long-term sustainability of an insurance pool but is a challenging balance to get right. Price too low and excessive claims may send the pool bust. Price too high and he number of people in the pool may reduce, which can also undermine its viability. To the extent that the mortality and morbidity tables are the key driver of risk pricing, we should think of them as dynamic and evolving. Claims experience essentially creates a constant feedback loop as to whether these tables – and therefore pricing assumptions – are accurate. Over time, through AI, big data and more comprehensive data collection by insurers, these tables will become far more refined, and pricing at a micro – truly individual – level can become possible.

Claims

The major outgoing for insurers – indeed the primary purpose for their existence – is the payment of claims.

In a purely theoretical sense, the premium rates paid by policyholders reflect the true risk of them suffering an event, as defined within the terms of the policy. Paying claims that are not consistent with the terms on which risk was priced can undermine the viability of the pool by essentially covering risks not priced for. The job of claims management is therefore as much about protecting the interests of other policyholders as it is to ensure the claimant receives the benefits of their insurance protection.

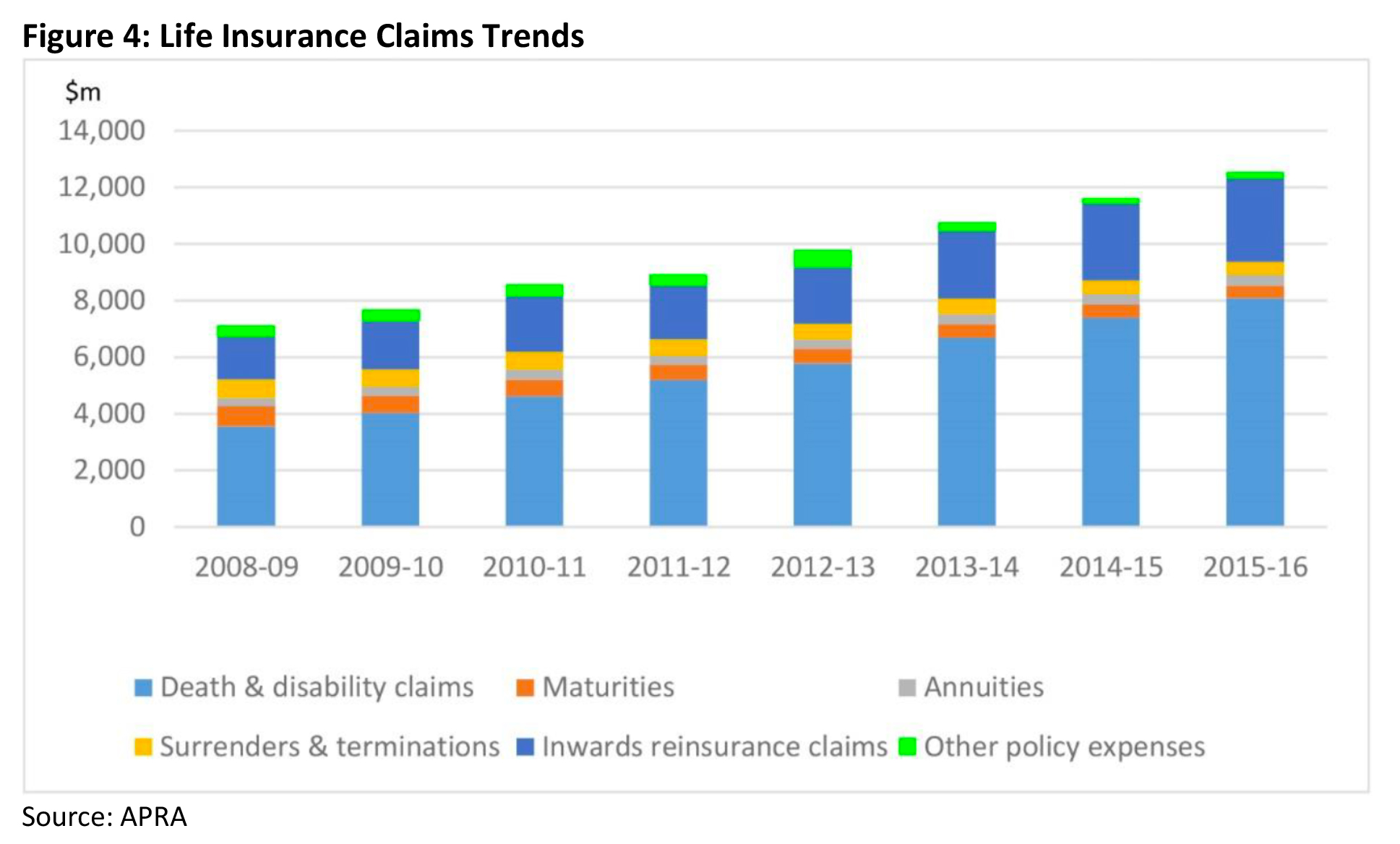

Broadly speaking, Australians are making more – bigger – claims on their life insurance. This is particularly true for TPD, Income Protection and Trauma cover. (In the case of income protection, claims are also lasting longer, 36% longer in 2018 than they were in 2013, to be precise.)

Figure 4 shows this trend between 2008/9 and 2015/16, with death and disability claims increasing from just under $4 billion in 2008/9 to just over $8 billion 7 years later[8].

Claims have continued to increase, and APRA’s most recent claims data release[9], in April 2020, showed that Australian life insurers admitted over 108,000 claims – worth over $9 billion – during the 2019 calendar year, of which around 54% were in respect of group schemes and 20% for retail policies.

Whilst the majority of factors driving these increases are well understood, some trends are defying expectations.

Whilst we are living longer, we are also becoming more overweight, with 67% of Australian adults classified as obese[10] in 2017/18, and thus at increased risk of high blood pressure, type 2 diabetes, coronary heart disease, stroke and several cancers. The fact that cancer related disability claims increased 31% between 2013 and 2018 should surprise no one[11].

More challenging for insurers, however, has been the mental health claims growth. According to the FSC, disability income claims paid due to mental health in 2018 were 53% higher than in 2013 with a 125% increase in the incidence of claims amongst men due to mental health[12].

The increasing prevalence of mental health claims is unlikely to be a temporary phenomenon. A variety of indicators suggest our mental health continues to deteriorate. In particular, anxiety and depression rates are continuing to increase[13]. According to Australian Institute of Health and Welfare (AIHW) data[14], the proportion of the population using Medicare subsidised mental health specific services grew from 4.3% in 2008/9 to 8.7% in 2018/19. The number of GP consultations to prepare mental health plans has grown from 813,257 in 2012 to 1,191, 786 in 2016.

The extent to which claims payments across the industry continue to outstrip priced in expectations – especially in disability income – has contributed to a significant recent profit squeeze; in 2019, one year after reporting a small profit of $34.1m (after tax), the Australian life industry made a loss of almost $1.3b on risk products[15].

Reinsurance

Rather than hold all the liability for potential claims themselves (self-insuring), most Australian life insurers look to share some of the burden of claims costs with one of several global reinsurers operating in our market.

In Australia, it is estimated that around 20% of in-force life insurance business is reinsured[16].

There are several benefits from using a reinsurer:

- Smoothing of claims experience, and profitability, by sharing risk

- Leveraging the global expertise and claims experiences of reinsurers (who work with many other insurers)

- Reducing the amount of capital that needs to be held against claims liabilities, which has pricing benefits and gives the insurer the capacity to write more policies with the same amount of capital.

The two main types of reinsurance used[17] by Australian life insurers are:

- proportional, or quota share, where the reinsurer takes on a pre-agreed proportion of risk on all policies; and

- excess of loss, where the reinsurer covers claims above the level that the life insurer is willing to retain (retention limits).

One practical economic implication of the use of reinsurers is the role they play in setting pricing. Their underlying mortality and morbidity rates, which drive the premium rates paid to them by insurers, are based in part on the totality of their global claims experience, and any change they make to their own rates will have a direct impact, either on the end premiums paid by consumers, or on the profit margin available to the insurer.

A second implication is that their ‘skin in the game’ is generally matched by a desire to get actively involved in claims and underwriting. Many insurers will use underwriting guidelines developed – or at least approved – by the applicable reinsurer. And in those claims where reinsurers are liable for at least some of the benefit amount, they will almost certainly demand the right to sign off on the claim decision.

The availability of reinsurance in a market is critical to the ability of individual insurers, and even the market as a whole, to be able to offer a broad range of protection options. Where that availability is under pressure because a reinsurer threatens to withdraw support, as is potentially the case with the individual disability income market, drastic measures – such as the APRA intervention[18] banning agreed value policies – can become necessary.

Capital management

Most life insurers run sophisticated treasury management functions, dealing with millions of dollars of cash inflows and outflows, and managing the assets of the business in line with strict APRA prudential standards.

These standards[19] – which were overhauled in 2013 – include requirements to invest policyholder funds (premiums) in separately managed statutory funds, and to hold a certain amount of capital in order to ensure an insurer can continue to meet claims liabilities. (Capital needs to be held for other purposes, too).

The Insurance Risk Charge is the minimum amount of capital required to be held against insurance risks[20]. The Insurance Risk Charge relates to the risk of adverse impacts due to movements in future mortality, morbidity, longevity, servicing expenses and lapses. In calculating the charge, allowances are made for the several factors, including market and credit risks.

Whilst historically it was not uncommon for insurers to make substantial profits through aggressive investment strategies, contemporary capital requirements generally drive insurers down a fairly conservative investment path, lest any adverse market movements require the injection of further – costly – capital.

Distribution costs

Distribution costs represent one of the largest single expense items to life insurers, especially in the retail market. As such, any changes to the ‘shape’ of adviser remuneration, such as those mandated by the LIF reforms, can have a substantial bottom line impact for insurers.

As an example, the reshaping of up-front commissions – halving the initial payment but doubling the ongoing trail – in turn reshapes the economic contribution made by each new policy. The long term nature of life insurance policies (guaranteed renewable policies can literally stay on the books for decades) mandates a long term horizon for financial modelling, and if we compare a model of 120% upfront and 10% trail to 60% upfront and 20% trail, any policy which stays in force longer than 7 years starts to become more expensive in terms of commission costs. Level commissions can prove even more challenging over long time frames.

Whilst it is tempting for some observers to assume the reshaping of upfront commissions has been some sort of ‘golden ticket’ for insurers, the reality is far from that. As well as long term commission costs increasing, the reduction in upfront amounts has made it less viable for some advisers to actively provide risk advice, compounding the loss of advice capacity driven by other factors, and ultimately driving down sales volume. These ‘twin pincers’ of higher costs and lower volume represents a significant economic challenge for the life insurance industry.

Product design

Product design can have a substantial economic impact to an insurer. Whilst the annually renewable contracts seen in general insurance effectively allow insurers to manage and limit their exposure in line with changes in external risk factors, the guaranteed renewability of life insurance can lock insurers into an exposure for decades. Over such a long-term horizon, changes to the circumstances of the life insured, as well as substantial social, medical and technological changes are highly likely but hard to predict (life insurers do not have a crystal ball).

Product design and pricing obviously go hand in hand. Product benefits which seem reasonable at the time, and which attract modest cost, can prove problematic over the long term as the world evolves.

Income protection products can be especially challenging; a policy with an age 65 benefit period represents a claims liability potentially lasting decades, and a conservative approach to capital management and reserving can make these contracts particularly expensive.

Product design and sales volume are also linked, especially in a market where research ratings play an important role in the product recommendation process

Underwriting

Underwriting works hand in hand with product design and pricing in shaping the nature of the risk pool, by controlling those who enter the pool, and on what terms. At a simple level, tighter underwriting can maintain or improve the risk profile of the pool, which over the longer term can limit upward pressure on claims (and premiums). However, such an approach can come at the expense of generating new entrants into the pool, which can have its own adverse consequences over time.

Group life

In terms of underlying financial dynamics, important differences exist between group and retail insurance.

Typically, new members into group life schemes have not been underwritten (unless they requested cover in excess of the default amounts). People in the workforce are generally assumed to be healthier than those who aren’t, plus the default nature of cover all but eliminates the risk of anti-selection. As such, an ‘automatic acceptance’ approach becomes viable, representing a substantial cost saving relative to individually underwritten policies.

The absence of retail commissions and the economies of scale possible in administering one master policy for hundreds of thousands of lives insured also impacts the way group cover is priced and means a much higher proportion of premiums are returned to members via claims payments.

Whilst its relationship with the superannuation system offers some sort of predictability in terms of distribution, this relationship creates its own risks in terms of regulatory change, and the recent ‘Protecting your super’ legislation has significantly disrupted the economics of group schemes, removing a cohort of younger healthier lives from risk pools, thus changing the risk profile and necessitating a repricing of risk for those remaining in the pool. This has been reflected in a raft of significant upward adjustments in group life premium rates[21].

Conclusion

The economic framework for life insurance involves a complex interplay of forces around two foundational concepts, the ability to pool risk and the ability to price risk accurately. Overlaid on top of this are considerations such as risk appetite, the availability and cost of capital, underwriting, product design and distribution. External influences such as regulatory reform, market performance and structural factors (e.g. research ratings) all combine to create an environment of challenging financial dynamics.

By developing a deeper understanding of the financial dynamics of life insurance industry, and the external forces at play, financial advisers will be better equipped to understand the way insurers respond to these forces, driving deeper, more informed, client conversations.

![]()

———-