What doesn’t kill us makes us poorer – the cost of care in Australia

There is clearly one critical question advisers should ask of all their clients; are they financially prepared for the cost burden of experiencing, or caring for someone experiencing, illness or injury?

Life, looking good in the ‘lucky country’?

As the self-proclaimed ‘lucky country’, Australia’s impressive achievements across sport, science, and cultural pursuits, are often out of proportion to our modest size. Happily, another area where we ‘punch above our weight’ is in life expectancy, where Australia ranks amongst the best in the world.

Since the very first Australian life tables were developed by Morris Birkbeck Pell in 1867, our life expectancy has improved from 46.5 years for men and 49.6 for women, to 80.4 and 84.6 years respectively[1].

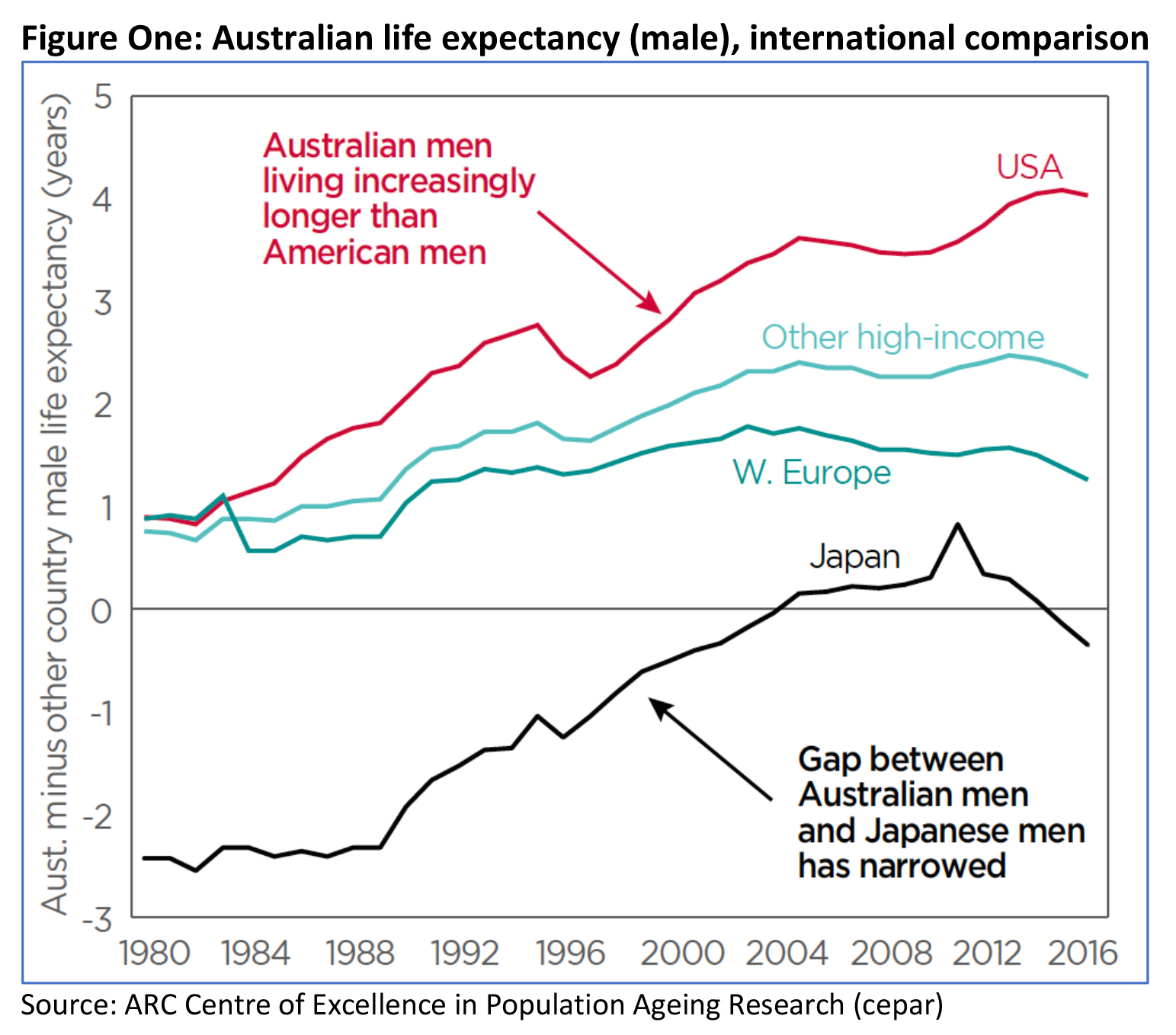

And, as Figure One, below, highlights, relative to our global peers, we’ve outperformed again, with Australian life expectancy higher than our colleagues in America, Western Europe, and many other high-income countries.

Examining the source of mortality improvements over time is enlightening.

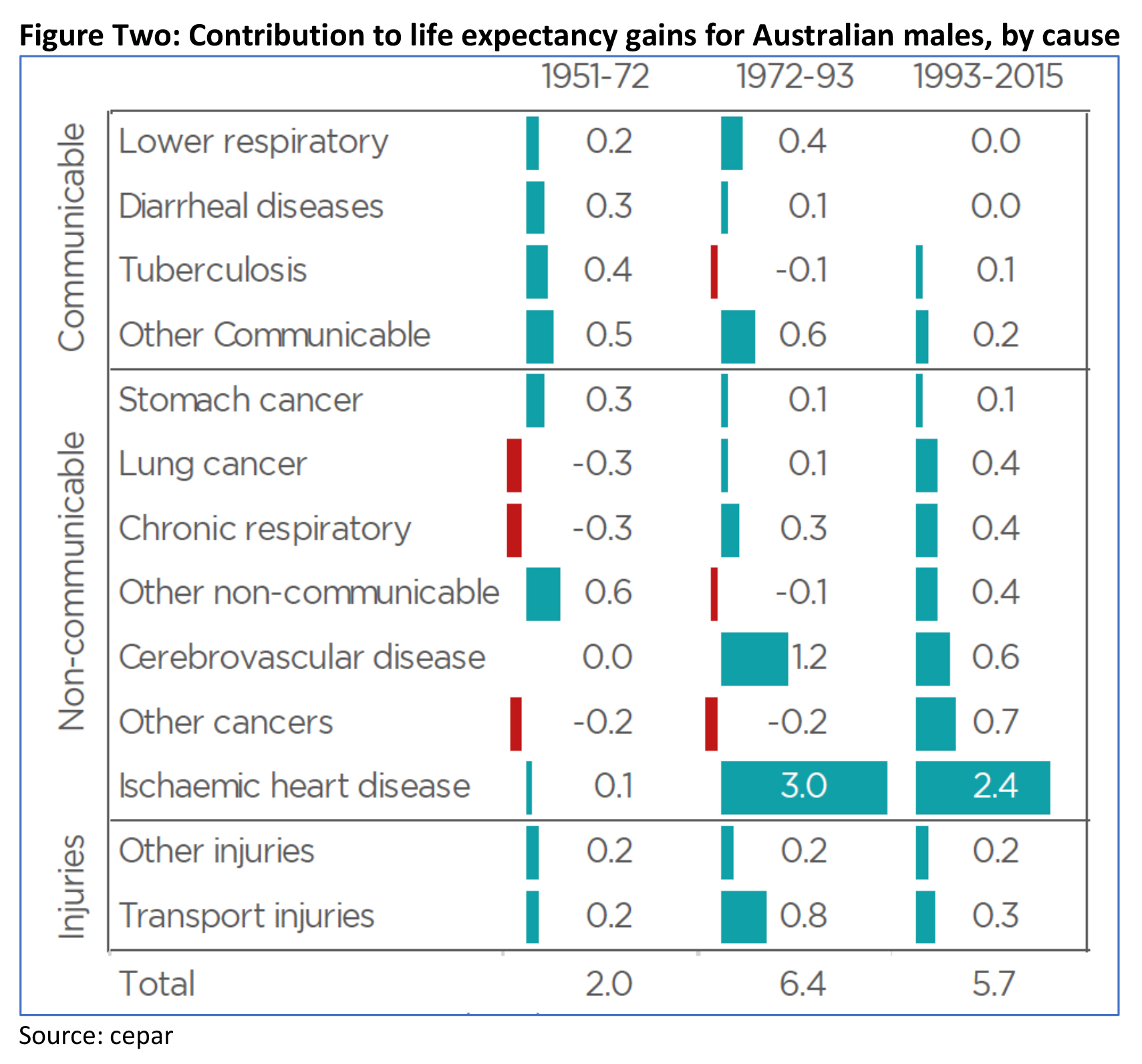

Figure Two illustrates life expectancy increases attributable to improvements in several major health conditions, including cancers, heart disease and transport accidents. The timing and effect of government interventions in areas such as tobacco, drink driving and car safety can be clearly seen, as can an overall positive trend attributable to improved lifestyles and ongoing medical advancements.

Whilst most experts agree we are unlikely to see mortality improvements of quite the same magnitude going forward, life expectancy is still likely to trend up. Indeed, one survey[2] predicts that by 2050, Australian life expectancy will reach 92 for females and 88.5 for males.

So, it’s all good news, right?

Well, sort of.

Although the incidence of many serious health conditions is decreasing, the reality is that the number of Australians suffering illness and injury continues to trend upwards. The good news is that – thanks to continual improvements in medical care techniques – these are conditions that, increasingly, we are living with, rather than dying from.

The bad news is that this care comes at a cost.

The growing cost of care

In 2017/18 total health expenditure in Australia was $185.4 billion[3]. Whilst State and Federal Government pick up the lion’s share of this burden, individual Australians – and their families and carers – still accounted for around $30 billion of this annual cost[4]. This is nearly twice the amount funded by private health insurers.

This amount relates to direct expenditure only and doesn’t account for any indirect costs in the form of income foregone by the individual and/or their caregivers.

Estimates suggest approximately two thirds of health expenditure by individuals relates to primary health care (i.e. unrelated to visits to hospitals or specialists), and approximately one third relates to medications[5].

The out of pocket burden falling on individuals

While Medicare is universal, and can cover hospital, medical and pharmaceutical benefits, more than 11 million Australians choose to ‘supplement’ their healthcare funding with private hospital cover[6]. Despite this, individuals are often left with a ‘gap’ between the amount covered and the total cost of the medical services.

This gap can arise for several reasons, including where service providers choose to charge more than the ‘notional fee’ for a service, as calculated by health authorities. This gap translates to an out-of-pocket cost, borne by the individual; the quantum of these costs can create a barrier to individuals seeking suitable treatment for their conditions.

An Australian study investigating the effects of healthcare costs on individuals found that 14% of adults didn’t receive the recommended care due to costs; for those living with chronic health conditions, the proportion was even higher, at an alarming 24%[7].

What does care cost?

From an incidence and cost perspective, two of the most significant categories of health problems are cancers and cardiovascular disease, and we will examine these in more detail below. By also directing our attention to some of the more ‘unusual suspects’, such as respiratory conditions, brain and nervous system disorders, and kidney disease, we can develop a more comprehensive and meaningful picture for advisers developing risk strategies for their clients.

Cancer

Cancer contributes to 19% of the total disease burden in Australia and has a significant social and economic impact on individuals, families and the community. In 2020, it is expected that 150,000 Australians[8] will be diagnosed with cancer, with the most commonly diagnosed cancers being prostate, breast, bowel and melanoma.

One in every three Australian men and one in every four Australian women will be diagnosed with cancer by the age of 75 years[9]. Furthermore:

- The chance of developing prostate cancer is one in five, with up to 40% of those diagnosed experiencing a recurrence;

- For breast cancer, there is a one in eight chance and recurrence rates range from 3-23%;

- The likelihood an individual will get bowel cancer in their lifetime is one in 13; up to 50% of those will experience recurrence within 2-3 years following their initial diagnosis;

- With the second highest incidence rates in the world, it is estimated that Australians have a one in 16 chance of developing melanoma cancer and approximately 11% will experience recurrence of the disease 25 years after initial treatment.

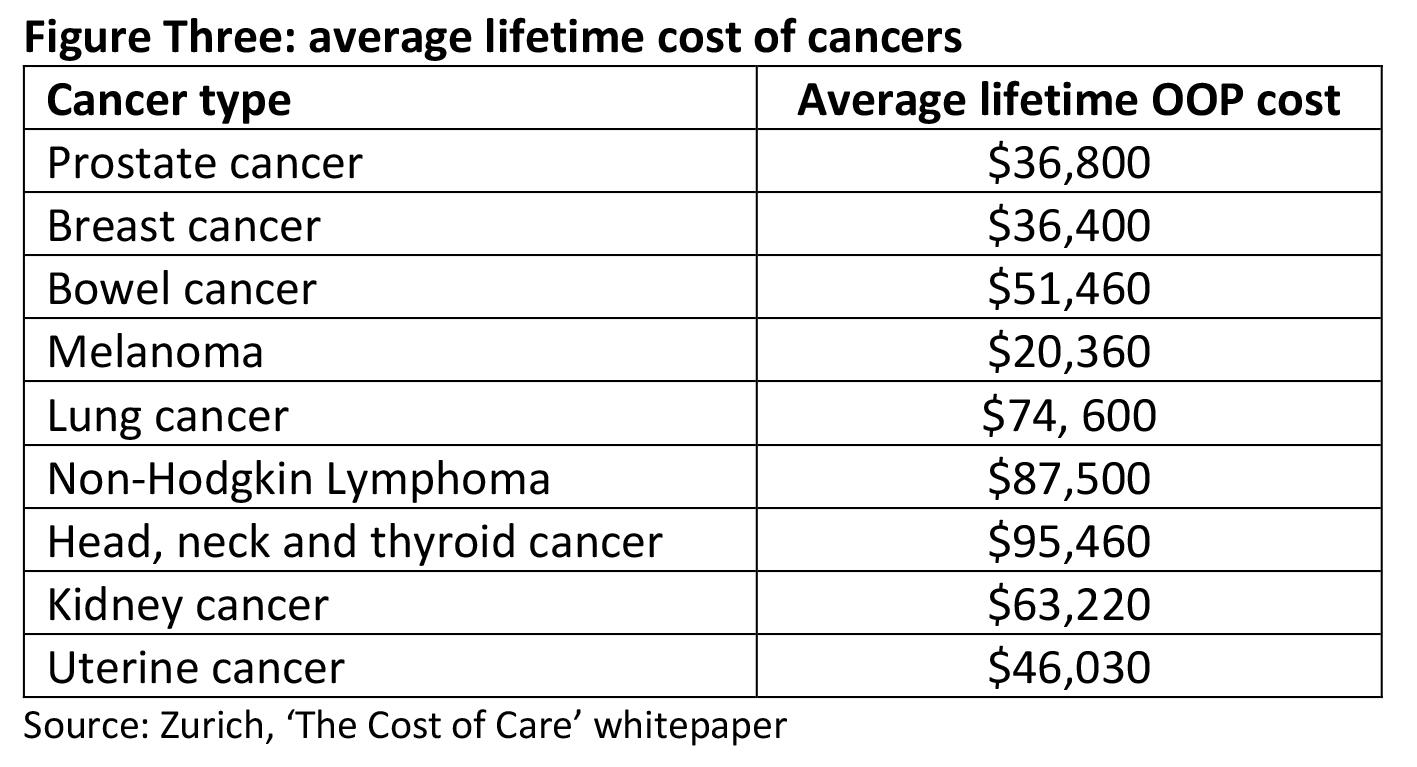

Although healthcare in Australia is largely publicly funded, out-of-pocket (OOP) costs associated with cancer diagnosis, treatment and survival can place a huge burden on sufferers and their families. Figure three details the expected average lifetime costs for 9 of the most prevalent cancers in Australia.

Approximately one in three Australians with cancer perceive the financial burden of prescribed medicines for cancer treatment or recovery to be moderate, heavy or extreme[10].

Although healthcare in Australia is largely publicly funded, there are still significant out-of-pocket costs associated with cancer diagnosis, treatment and survival. These can include:

- GP and specialist gap payments

- Scans or tests outside of the public system

- Over the counter medications for pain relief and other purposes

- Complementary medicines or therapies

- Medical devices

- Travel

- Accommodation

- Personal care (e.g. managing ulcers during radiotherapy).

People who live outside major cities have 17 times the odds of reporting locational or financial barriers to care compared to those living in metropolitan areas[11].

The financial burden of cancer extends beyond the patient, with 72% of cancer carers reporting a negative financial impact of caring and more than half of carers who work full time need to take leave or reduce working hours[12].

Respiratory conditions

Even before the world had even heard of Covid 19, chronic respiratory conditions were a significant health issue for Australia, affecting more than a quarter of the population.

It is estimated that there are 2.5 million Australians living with asthma[13], and 1.5 million suffering chronic obstructive pulmonary disease[14] (COPD). COPD is a condition that limits airflow to the lungs and is not fully reversible with the use of medication.

There are 19 deaths per day from COPD, and three quarters of all COPD cases can be attributed to tobacco[15]. Of Australians with lung disease, COPD contributes to almost one-third of all deaths and costs patients an average of $9,020 in out-of-pocket (OOP) costs per year.

78% of people living with advanced COPD experienced economic hardship from managing their illness and 27% were unable to pay their medical expenses[16].

Cardiovascular disease

Cardiovascular disease (CVD), which covers a range of conditions affecting the heart and arteries, such as heart attack, stroke and high blood pressure, is responsible for one death every 12 minutes in Australia[17] and is one of Australia’s largest health problems. Despite medical advancements over the last few decades, it remains one of the biggest burdens on our economy.

Common risk factors like high cholesterol, smoking, obesity and diabetes play an important role in CVD. A 45-year-old man with two or more of these risk factors has a 1 in 2 chance of experiencing a major cardiovascular event by age 80. For women, the risk is marginally lower at 1 in 3, but the overall trend is the same – more risk factors equal greater risk[18].

Australian expenditure on CVD is enormous; more is spent on CVD than any other disease group.

In 2012-2013, $5 billion was spent on healthcare for people with CVD, which equates to 12% of all healthcare expenditure[19]. CVD is responsible for 84 million prescriptions per year at a cost of $3.3 billion[20].

The indirect costs of CVD are also hefty. Treating CVD often involves large surgical procedures, lengthy recovery periods, loss of independence and loss of income. In addition, many people who experience a cardiovascular event, such as heart attack or stroke, will take time off work, resulting in losses to their employer as well.

Even though rates of CVD are decreasing, expenditure is likely to increase in the future due to the ageing population and population growth. Spending on CVD is estimated to increase to $8.3 billion by the year 2033[21].

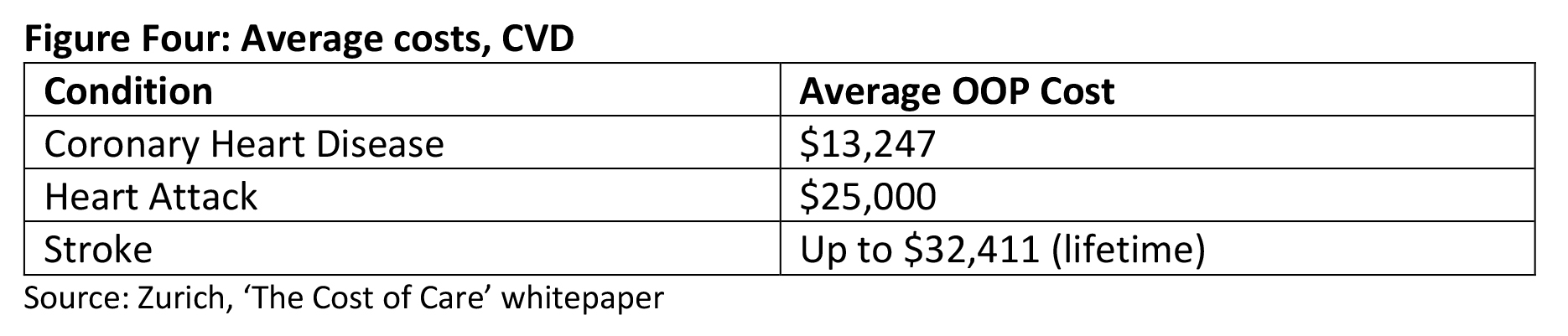

Costs to the individual also add up, with an average individual out-of-pocket spend of $2,520 in the first year following a stroke. Other CVD events, such as heart attacks, are associated with extensive surgical procedures and lengthy recovery periods (meaning time in hospital and time away from work).

The cost of serious illnesses can also arise in the years following the event, sometimes in the form of disability and restriction in daily living. For example, in 2009 it was estimated that over a third of people with stroke had a resulting disability[22]. Furthermore, a national survey found that 81% of stroke survivors reported significant levels of unmet need in the community after discharge from hospital[23].

Strokes have a significant impact on carers:

- 58% of primary carers of spend 40 hours or more per week in their caring role

- 21% report a decrease in income due to their caring role

- 24% incur extra expenses due to their caring role

- 31% have difficulty meeting everyday living costs.

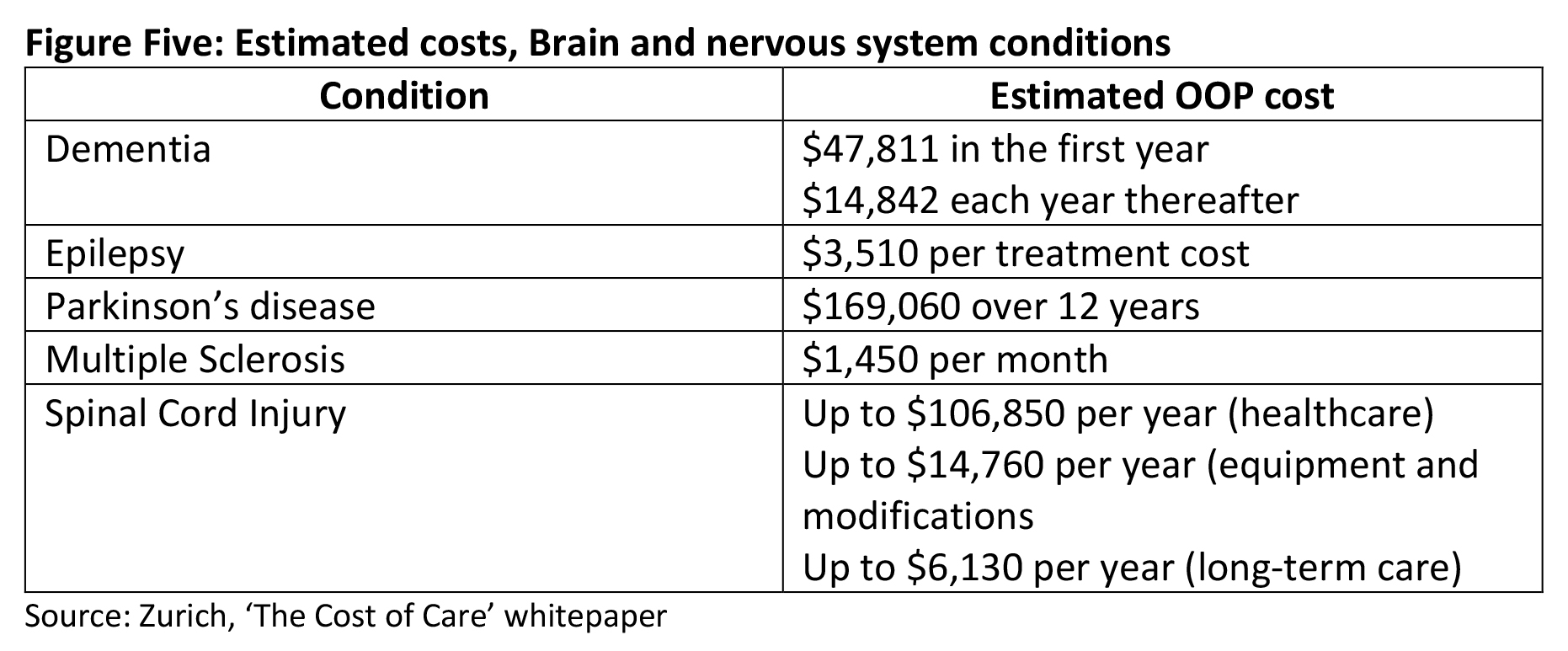

Brain and nervous system conditions

Conditions of the brain and nervous system include dementia, epilepsy, Parkinson’s disease, multiple sclerosis (MS) and spinal cord injury (SCI). There are approximately 802,416 Australians living with these conditions – more than half (425,416) are living with dementia[24] and one-third (250,000) with epilepsy[25].

Dementia is a term used to describe symptoms of a larger group of illnesses that cause a decline in a person’s functioning. These symptoms can include loss of memory, rationality, social skills and physical functioning.

One of the most commonly known types of dementia is Alzheimer’s disease.

Dementia is more common in women than men and is the greatest cause of disability in people over the age of 65 years, and the second leading cause of death in Australia overall[26].

Approximately 25,938 people are living with younger onset dementia. By 2056, this number is expected to increase to 42,252 people[27].

The likelihood of acquiring a condition of the brain or nervous system varies. The chance that an individual will develop MS during their lifetime is 0.3%, while the risk of developing dementia can be as high as 17% over the same period.

Due to the nature of brain and nervous system disorders, expenses are commonly incurred for formal care, mobility aids and assistance devices, pharmaceuticals and accommodation and travel.

Indirect costs are also incurred, resulting from the inability to work full time or at all in some cases.

An individual with dementia can expect to pay $47,811 in the first year and $14,842 each year thereafter to manage their condition, whereas a person with Parkinson’s disease may end up paying $169,060 over a period of 12 years. Figure Five summarises costs for common brain and nervous system conditions.

Kidney disease

Kidney disease affects around 1.77 million Australians, is responsible for 9 deaths each day and kills more people each year than breast cancer, prostate cancer or road traffic accidents[28].

It is estimated that 4 out of 10 individuals without chronic kidney disease (CKD) at age 50 years will eventually develop CKD[29].

In most cases, kidney function in people with CKD will continue to decline and the disease will progress despite treatment. Thus, almost all people with CKD will incur lifelong expenses to manage their condition.

The average cost of kidney disease at $3,897 per year[30]. Those with more advanced stages of the disease will ultimately incur higher costs due to dialysis, transportation to and from treatments and transplant care. In addition to direct treatment costs, regular dialysis can mean significantly reduced working hours or unemployment.

In a survey of people receiving dialysis for CKD, 71% said they experienced ‘financial catastrophe’ as a result[31].

Conclusion

Whilst advances in medicine and treatment techniques are improving the survival rates across most serious health conditions, there is a cost burden.

This cost burden – estimated at $30 billion and upwards each year – falls on all of us, as taxpayers and as individuals. And as good as our safety nets are, the out of pocket (OOP) cost impact to those affected by ill health can be crippling.

Depending on the condition, direct costs can range from hundreds to many thousands of dollars each year. Often these are compounded by the indirect costs – such as foregone income – impacting the sufferers and those who care for them.

Life insurance is a vital part of the ecosystem that helps protect the financial, emotional and physical wellbeing of Australians. But without a better understanding of how each of these systems interact, and a realistic appreciation of the true costs of poor health, we are ill equipped to judge the appropriate types and levels of support to best suit our circumstances, and to navigate a complex network of services and providers.

There is clearly one critical question advisers should ask of all their clients; are they financially prepared for the cost burden of experiencing, or caring for someone experiencing, illness or injury?

![]()

———-