IDII changes – rethinking the role for trauma in risk strategies

As the new era of income protection beds down it’s time for advisers to rethink the role for trauma cover as part of a comprehensive life insurance strategy.

Since its introduction to the Australian market over 20 years ago, trauma (aka crisis or critical illness) cover has become an important part of the life insurance product universe.

Designed to pay a lump sum in the event that the life insured suffers a traumatic illness or injury, the trauma cover claim rate is second only to income protection, reflecting a likelihood of a claimable event that is around 3 times that of death cover and twice that of TPD cover[1].

Naturally, this morbidity rate is reflected in much higher premiums compared to other lump sum products, creating an affordability challenge for policyholders, especially beyond the age of 50. This challenge is exacerbated by the lack of tax deductibility of trauma premiums, and the inability to take trauma cover through superannuation. These factors, amongst others, explain why numerically, trauma is the least held of all retail lump sum policies.

However, APRA mandated changes to Individual Disability Income Insurance (IDII), including a reduction in income replacement ratios, may well be a catalyst for advisers and customers to rethink the role for trauma cover as part of a comprehensive life insurance strategy.

In this article, we will examine a number of critical issues around a reimagined role for trauma cover, including the market context, its ability to act as an income replacement mechanism in some circumstances, product design trends, and strategic considerations when constructing tailored life insurance portfolios.

The rise of ‘living insurance’

At the heart of the trauma insurance value proposition lies a ‘bad news – good news – bad news’ story. The bad news is that serious – traumatic – health conditions are prevalent. The good news is that survival rates for most serious health conditions are improving all the time. The bad news is that the treatment and recovery costs associated with serious health traumas can be very expensive.

Therein lies the role for trauma cover – providing a lump sum in the event you suffer a health condition which is serious, but which you are increasingly likely to ‘live with’, rather than ‘die from’.

To illustrate this context, consider the figures below.

The Australian Institute of Health and Welfare expects over 150,000 Australians to be diagnosed with cancer[2] during 2021. The most common of these will be breast cancer, prostate cancer, and melanoma. According to Zurich’s Cost of Care whitepaper[3], there is a heart attack every 10 minutes, and 96 people will suffer a stroke each day (69 of whom will survive).

Happily, thanks to ongoing improvements in medical techniques, these conditions are being detected earlier and treated more successfully, seeing survival rates continue to increase, dramatically in some cases.

The death rates from stroke[4], for example, decreased by 70% between 1979 and 2010, whilst heart disease death rates[5] decreased by a staggering 600% between 1968 and 2015. Cancer survival rates have improved dramatically too, as illustrated in Figure 1, below.

But the cost of surviving a serious health trauma can be significant. Whilst Medicare certainly covers a substantial proportion of the cost of treating major health traumas, there is almost always a significant out of pocket burden, potentially a longer term one if medication and ongoing treatment is required.

For example, the average lifetime cost for cancer sufferers aged 15 years and older, can range from $20,360 for melanoma to $95,460 for head, neck, and thyroid cancers[6]. The lifetime out of pocket cost for stroke sufferers averages over $30,000[7]. And according to the Heart Foundation[8], the average cost of a heart attack to an individual and their family over a lifetime is $68,000.

Trauma claims

For the 12 months ended December 2019, life insurers paid 4815 claims to retail (advised) trauma policyholders. In volume terms this was second only to income protection (11, 797) and almost as many as death (3539) and TPD (1495) combined[9].

On a base of around 800,000 in force trauma policies, this equates to a claim rate around twice that for TPD and three times that for death.

Whilst most trauma policies on the market are comprehensive, covering in excess of 50 specified health conditions, the vast majority of claims are for the ‘big 4’ conditions – cancer, heart attack, stroke, and coronary artery bypass surgery, although this does vary greatly by gender, as shown below. Typically, around 80% of female trauma claims are for cancer, whereas as for males this is closer to 50%.

Keeping up with the science – the trauma design challenge

There are a number of product design challenges unique to trauma insurance, most of which stem from the rapid advancement of medical diagnosis and treatment techniques, and the often highly complex conditions contained in many trauma definitions.

For example, the way heart attacks are detected and treated – and even defined – has changed significantly in the last decade. This can be problematic if the definitions contained within trauma policies don’t reflect contemporary medical and scientific practice, as was seen a few years ago with high-profile media coverage around insurer definitions of heart attack and multiple sclerosis.

In the case of the heart attack definition, the reliance solely on a definition based around elevated levels of a cardiac enzyme (troponin) was found to be unfair after it resulted in a major insurer denying a claim by a man who, they admitted, had suffered a ‘severe’ heart attack.

Experts at the time declared the definition to be out of step with current medical practice, with the President of the Cardiology Society of Australia and New Zealand, Professor Andrew MacIsaac, saying it was not possible to diagnose the severity of a heart attack based on Troponin levels alone[11].

The controversy effectively put life insurers on notice, and in response they worked with the Financial Services Council to develop a system of minimum standardised definitions for cancer, heart attack and stroke. These definitions are codified in the Life Insurance Code of Practice, launched in 2017[12], as is a commitment to review – and if necessary, update – them at least once every three years.

The lottery effect

A further challenge arises from ongoing improvements in medical treatments and recovery times.

For example, treating heart conditions through open heart surgery – which could take weeks and even months to recover from – has become far less common, replaced by far less invasive ‘keyhole’ techniques which are much quicker to recover from.

Thyroid cancer can often require as little as 1-2 nights in hospital and is treated via medication rather than chemo or radiotherapy[13].

These are just two examples from many that have contributed to the ‘lottery effect’ in trauma insurance – so called because the amount of claim benefit paid often far exceeds the physical and economic impact of that trauma.

As well as the elevated moral hazard that stems from such a phenomenon, the mismatch between claim amount and severity is problematic from a pricing perspective, as premiums need to reflect increasingly overgenerous and unnecessary claims payouts. For those who win the lottery, fantastic, but for everyone else, it means trauma cover is more expensive than it needs to be.

Severity based trauma

Whilst trauma products have not experienced the same pricing sustainability challenges seen in IDII, they are easily the least profitable of all lump sum products, and in the last few years have been subject to more price increases than death and TPD[14]. (Recent comments[15] at an industry forum suggest insurers are keeping a close eye on claims experience across their trauma portfolios so as to avoid another APRA intervention.)

One of the most significant and recent innovations in trauma insurance – designed to directly address this ‘lottery effect’ – is the advent of severity-based trauma products.

The intent of severity-based products – which are proving very popular in overseas markets – is to have a better match between the physical and financial impact of the trauma on the life insured, and the benefit paid. In the event of severe cases of specified conditions, the full benefit is paid. For less impactful conditions, a proportion of sum insured is paid.

In practical terms, severity-based products generally apply a scale of impact to the health condition suffered, and with the ability to pay out anything from 5% to 100% of the sum insured, severity-based policies usually have a much lower threshold of claim eligibility. Simplistically, they are designed to pay lower amounts, more frequently. Of course, for severe levels of illness, or as a condition deteriorates, higher payments are made.

In the UK, for example, one insurer estimated that – compared to a traditional trauma policy – severity based policy holders were three times more likely to be eligible for any type of claim, 116% percent more likely to be eligible for a cancer claim, 34% more likely to be eligible for a claim for heart attack and 25% more likely to get a pay-out for stroke[16].

The severity-based approach allows policies to cover a much broader range of health conditions, at a substantially lower cost than traditional trauma policies.

Whilst in Australia severity style products are yet to come into their own, it seems likely that pricing pressures and ongoing medical advancements will see them become the dominant offering.

Trauma as a substitute for income protection

In an ideal world, clients would hold fully featured income protection with the shortest possible waiting period and the longest possible benefit period, as well as trauma, death and TPD cover. Regrettably, the ideal world doesn’t exist, and for various reasons a client may be unable to obtain, or afford, a fully comprehensive suite of life insurances.

Part of the financial adviser’s role is to tailor a risk portfolio that optimises the client’s situation, including using products as complements and substitutes for one another. Compromises – or informed trade-offs – come with the territory.

Whilst income protection and trauma are quite different in their core purpose, trauma is often used to fill a gap for those clients who, perhaps because of their occupation and/or income profile, are unable to obtain income protection.

Whilst this still means the client is uncovered for those relatively minor health conditions which may leave them unable to work for a few weeks or months, it can at least see them protected for those health events major enough to see them unable to work, but which fall below the threshold for TPD.

The legitimacy of such a strategy is reinforced by claims statistics which show that around one third of income protection claims are for cancer, cardiovascular conditions, and sickness (and a third are for accidental injury)[17].

Trauma as a complement to income protection

The new wave of APRA friendly income protection products has seen benefits pared back in several key areas, including monthly benefit limits.

With a maximum income replacement ratio of 90% for the first 6 months of claim and 70% beyond that, most new products set a maximum benefit at application of 70% of income. Some products have set this to 60% from the start, while others drop to 60% after 2 years on claim.

Many ancillary benefits – such as lump sums for trauma or specified injury – have also been stripped out.

Many products also switch to an ‘any occupation’ definition of disablement after 2 years on claim.

In this context, there is perhaps a more important role for trauma to play as a complement to income protection.

For example, it could be used to help boost any income protection payout to 100% of income for the first 2 years of a claim (data[18] suggests that the average income protection claim length is 12 months, 14 months for cancer related claims).

For higher income earners, the inability to secure monthly benefits in excess of $60,000 per month may also create the opportunity for trauma to act as some sort of ‘top up’ in the event of disablement due to serious health trauma.

Another opportunity might be to pull back on the benefit period for income protection, in order to achieve a substantial premium saving, and instead supplement with trauma, providing support for instances where – due to a trauma – the client is still off work after 2 years, but doesn’t qualify as disabled under the any occupation definition.

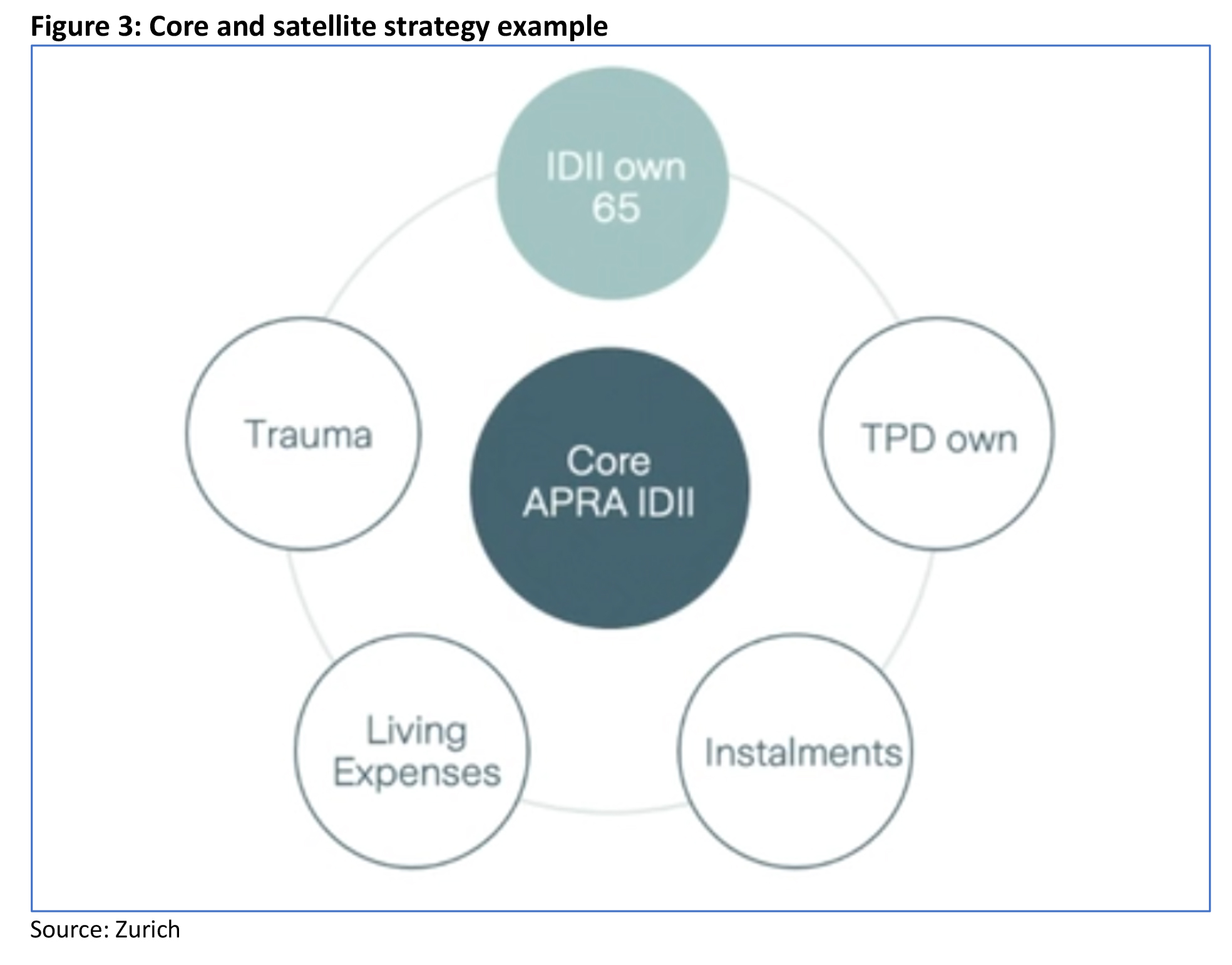

Zurich refers to this approach as the ‘core and satellite’ strategy, where one product – often income protection – sits at the centre of the strategy, and then other covers and options are added around it so as to achieve the optimal balance of coverage and value. (Decisions around disablement coverage inside and outside super are also an integral part of such a strategy).

Other strategies with trauma

Another opportunity to optimise value and affordability is the combining of stepped and level premiums for trauma. Given the steep rate of increase for trauma premiums when a client is 50 or older, this strategy is about ensuring the client can always afford a base level of cover. An example might be locking in $50 k or $100k (or more) as the base trauma amount, at level rates, then topping up the required balance at stepped rates. If the stepped rates become unaffordable, at least the client is able to keep the core cover, the cost of which has remained largely unchanged (notwithstanding any indexation).

Several insurers also now offer the opportunity to receive trauma benefits as instalments rather than as a lump sum, usually for a small premium discount.

Calculating sums insured can be a highly subjective topic. To the extent that life insurance is intended to return people to their pre claim position (rather than make them better off), trauma sums insured need to reflect the loss of income and extra medical and rehabilitation expenses that would be incurred in the case of a trauma. Sums insured designed to pay off large debts are likely to be out of step with the core purpose of the cover and will only entrench the ‘lottery’ perspective of trauma.

Conclusion

As the new era of income protection beds down, the pared back design of APRA friendly products – with lower income replacement ratios, fewer ancillary benefits, and changing disablement definitions – creates new challenges for advisers seeking to optimise the balance of coverage, value, and affordability for their clients. In this context, now might be the time to reconsider the role for trauma cover in life insurance strategies. As a highly versatile product, its importance as a complement to, and in some circumstances a substitute for, income protection, is likely to increase substantially going forward.

![]()

———–