The tide is turning: Shareholders have been rewarded with a record level of dividend payments from the 2020-21 financial year.

The most recent reporting season affirmed how the global COVID-19 pandemic impacted businesses and sectors in different ways and as expected, announcements of dividend payments for the next 12 months will likely be back in line, or ahead of, those that paid pre-COVID. Max Cappetta, CEO of GSFM investment partner Redpoint Investment Management discusses the outlook for, and sources of, dividends in the coming year.

Shareholders have been rewarded with a record level of dividend payments, more than $35 billion, from the 2020-21 financial year. It’s a stark turnaround from a year ago, when dividend payments were slashed as many companies chose to stockpile their capital rather than distribute it to shareholders.

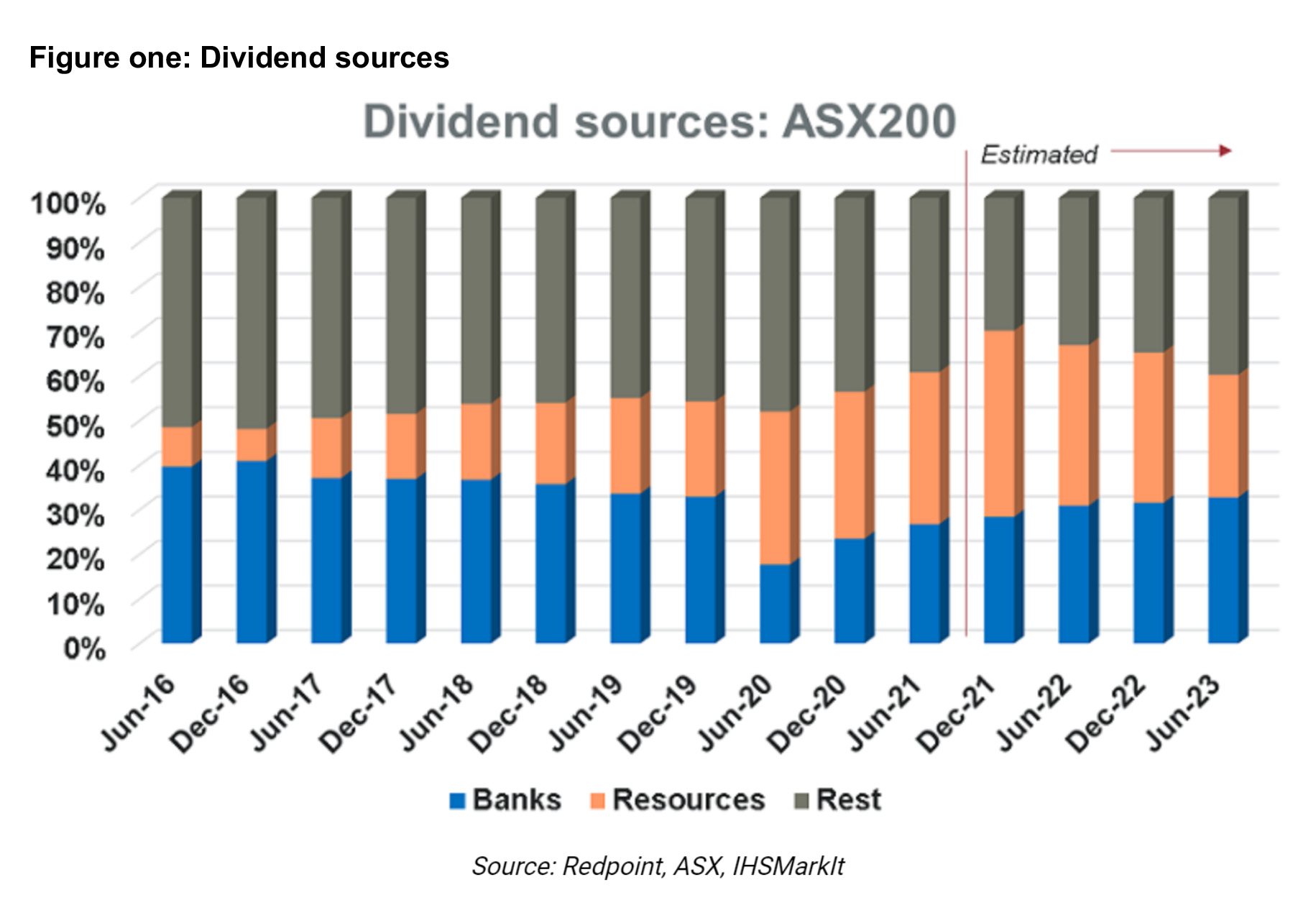

And while dividends are rapidly returning to pre-pandemic levels, the sources of these dividends are likely to be different to previous years.

Inclusive of franking credits, the ASX200 has delivered an attractive yield relative to term deposits over the long term – and especially over the past decade. Driven by underlying economic growth, the resilience and rise in share prices is also a characteristic of dividend payments through time.

Furthermore, Australian corporates continue to favour higher payout ratios due to Australia’s policy of attaching tax credits to dividends for the tax paid on profits earned by companies.

This important policy pillar supports the retirement savings system and will enable appropriately constructed equity portfolios to play their part in an effective retirement income strategy. The Australian Government’s 2021 Intergenerational Report is forecasting that over 40% of retirees will be self-funded by 2060, and less than 25% will be drawing a full government pension (versus 50% today).

A growing need for retirement income

There’s approximately $750 billion in today’s retirement super pool that, over the next decade, will move into a retirement phase. This is a huge amount of capital that will transition from an accumulation approach to a strategy more suited to retirement. In retirement, people need income, however, they also want their capital to grow over their retirement period. This helps shield them from longevity risk, or the risk of outliving their retirement savings.

Many people in retirement have sought low risk investments, namely cash and term deposits. For example, Australia’s SMSF sector has nearly $150 billion sitting in cash and term deposits, 18 percent of the $822 billion in SMSF assets, at 30 June 2021 (source: ATO).

In the current environment, and potentially for the foreseeable future, the low-risk or no-risk investment has in fact become the low return or no-return investment. When inflation is factored in, cash does not provide a positive return and it becomes challenging to maintain the purchasing power of retirement capital over the longer-term.

For retirees to achieve a growing income stream, as well as ensure that their capital stays in line with purchasing power and inflation, equities are an obvious solution.

Over the long term, the total return delivered by Australian equities can be divided into an income return of approximately 40 percent from dividends, and the remaining 60 percent from capital growth.

High capital growth is important for the accumulation phase where earnings are taxable; most investors prefer to actually have their assets growing. However, in the retirement phase, most investors prefer income to capital growth. In an ideal world, retirees would prefer up to 75 percent of the total return from equities delivered as income.

Retirees still need growth to ensure their capital maintains its purchasing power throughout 25-30 years of retirement. So, how can you turn the total return components of the Australian equity market, in many ways, upside down?

The response from many investors would be to focus on those companies paying the highest dividends relative to their price. However, that can be a dangerous approach because that can result in an investment in companies that are potentially stressed with low share prices are today, relative to previous higher dividends. High dividends may also indicate that a company is not growing, and so they choose to pass off their cashflow to investors as dividend income.

Therefore, investing for equity income and a reasonable total return that can keep up with inflation over the long-term is a multiple objective strategy. While investors should pay regard to previous dividends, it is also important to look at a company’s future earnings and profitability. This provides an indication of where the dividend income opportunities may be in future periods.

Dividends returned in 2021

Australia’s mining sector was set to be the star of the corporate reporting season in Australia and did not disappoint. Record profits were expected from companies involved in iron ore mining, thanks to record high prices. Companies such as Fortescue, Rio Tinto and Mineral Resources delivered record dividends.

Government financial support during the pandemic and ensuing lockdowns ensured that retail spending remained robust. Retailers such as JB Hi-Fi and Kogan have been beneficiaries and rewarded investors with growing dividends. Supermarkets have also benefited from the ‘stay-at-home’ thematic, with Coles and Metcash paying a growing dividend stream over the past two years. More recently Woolworth’s shareholders were rewarded with an increased final dividend and the opportunity to participate in a $2.2b share buyback.

Healthcare has also delivered on dividends, with plasma giant CSL, protective-wear specialists, Ansell, and equipment manufacturer Fisher and Paykel Health all growing their dividends (albeit this growth has not translated to share price growth for CSL, which currently trades at 10 percent below its pre-COVID highs).

The IT sector has also been a standout winner in the past year, driven by low interest rates and the perceived stability in their revenues, irrespective of whether workers are in the office or at home. Global logistics software specialists Wisetech more than doubled its dividend payments in 2021 versus 2020. Similarly, global security specialist Codan has grown dividends by 50 percent in 2021 versus 2019 levels. Both companies pay fully franked dividends, albeit they are a low yield.

This highlights that income-focused investors need to ensure their income generation also provides some exposure to earnings and dividend growth, and not simply focus on high yield alone. Wisetech has almost doubled in price recently after a strong earnings result, while Codan, having fallen back from recent highs, now trades at $13, more than 50 percent above its pre-COVID high of $8.50.

For the banking sector, Australia’s banking regulator, the Australian Prudential Regulation Authority, dropped restrictions that banks limit dividends to 50% of profits in mid-December. This enabled an increased dividend from all four of Australia’s largest banks in the first half of this year.

CBA further increased its dividend in August after being more cautious in February, with the remaining three seeing economic conditions improve in early 2021 before paying increased dividends in May. The rollout of product innovations and divestments in the sector could be a catalyst for earnings growth moving forward.

On the other side of the ledger, COVID-19 has been devastating for industries such as tourism and travel. After promising signs through the start of 2021, the subsequent lockdowns meant ongoing tough operating conditions. Now that lockdowns are lifting, circumstances will improve for tourism and travel businesses. Investors also need to be aware of the potential for mergers and acquisitions as trading conditions improve. One such example is the current takeover offer for Sydney Airport.

Just like driving: look forward, not back

Being distracted by a high historic yield can be detrimental to investment outcomes. High yields can often hide low growth, business stress or a failure to properly reinvest to support future growth.

Research indicates that a focus on historical yield has consistently underperformed the ASX200, and by taking a forward-looking approach to dividend yields, opportunities can be found. A track record of consistent or growing dividend payments is a sign of reliability and can be an indication that investing in the company will provide a reliable income stream in the future.

Don’t focus only on high yields

A company that is producing dividends or that has a high dividend yield is not always a good investment. There have been cases where a company’s management has used dividend payments to make up for a lack of growth and placate frustrated shareholders. To avoid ‘dividend traps’, it’s important to understand the company’s dividend strategy.

In some cases, market movements can artificially inflate the dividend yield. A good example of this was the GFC, when the dividend yields of many stocks were driven higher because of falling share prices. Although these dividend yields may have looked good, many of those companies experienced a steep fall in profits, which then impacted the company’s ability to pay any dividends at all.

The market goes through phases where dividends and companies that pay dividends are in demand, and other periods when they are not. The past 15 months are a brutal reminder of investor appetite for growth and risk versus cashflow and dividends.

Some income-focused strategies commence with defining an investible universe based on higher dividend yielding stocks. Some strategies start with a specific income style and then seek to identify the highest yielding stocks within that sub-group. This can be rewarding at times when dividend-paying companies are in greater demand but can be harmful to overall returns at other times.

Being constrained to invest in just a subset of the market can also lead to less consistent dividend capture if particular sectors of the market are impacted by a change in business conditions while others are not. This is where risk management and a diversity of stock selection views can deliver an investment edge versus a singular focus on high yield alone.

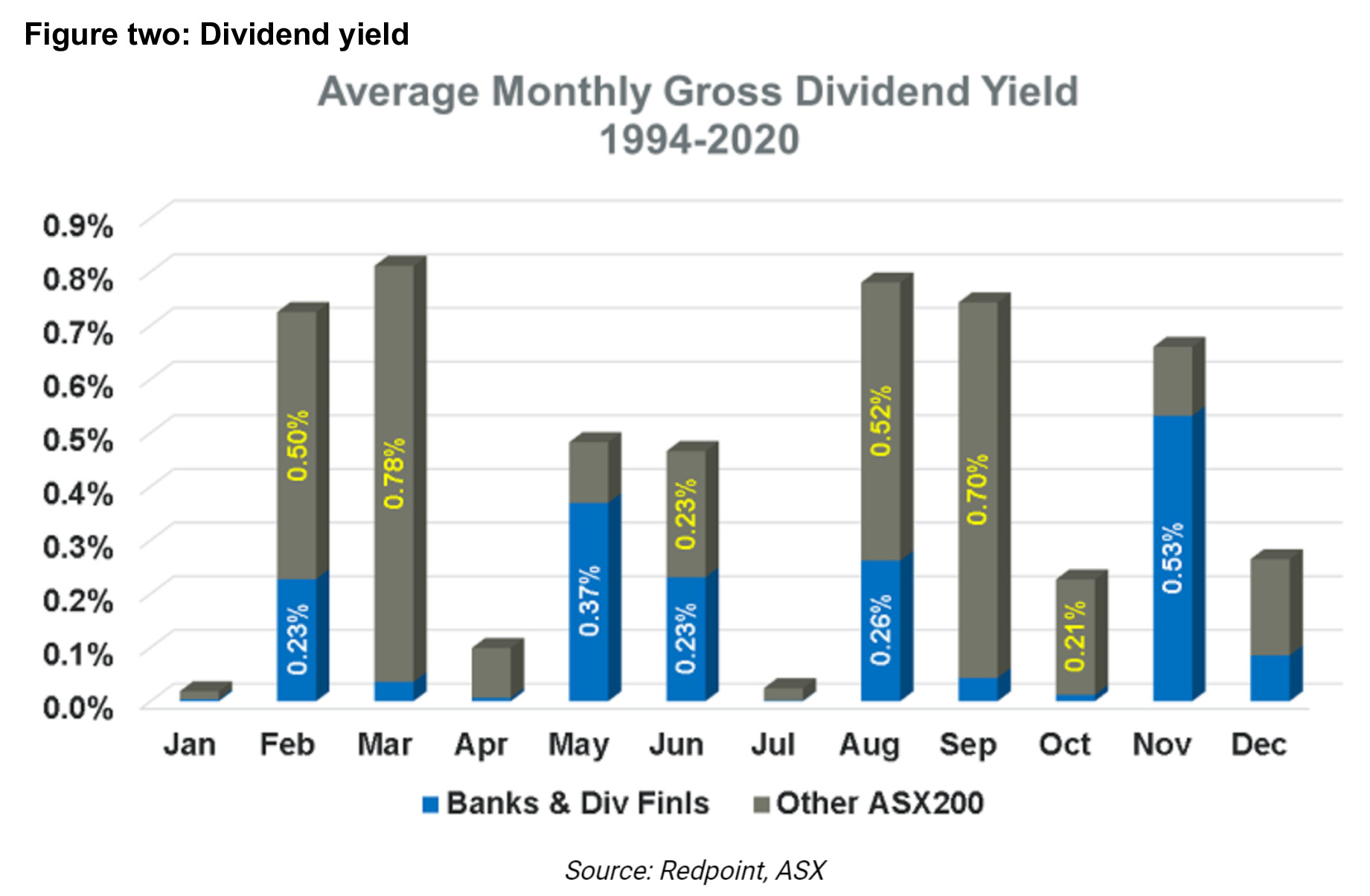

Different companies pay dividends at different times during the year. There is an opportunity for a dynamic approach to trade across these different periods to capture an overall above-average income yield while retaining exposure to higher growth stocks. Of course, investors need to abide by holding period rules to ensure they not only capture the cash dividend but also any tax credits attached.

Capturing a consistent dividend yield from equities cannot be a set and forget endeavour. Building a portfolio from last year’s best-yielding stocks has delivered above average dividend income but has consistently underperformed the index overall.

Looking ahead to 2022

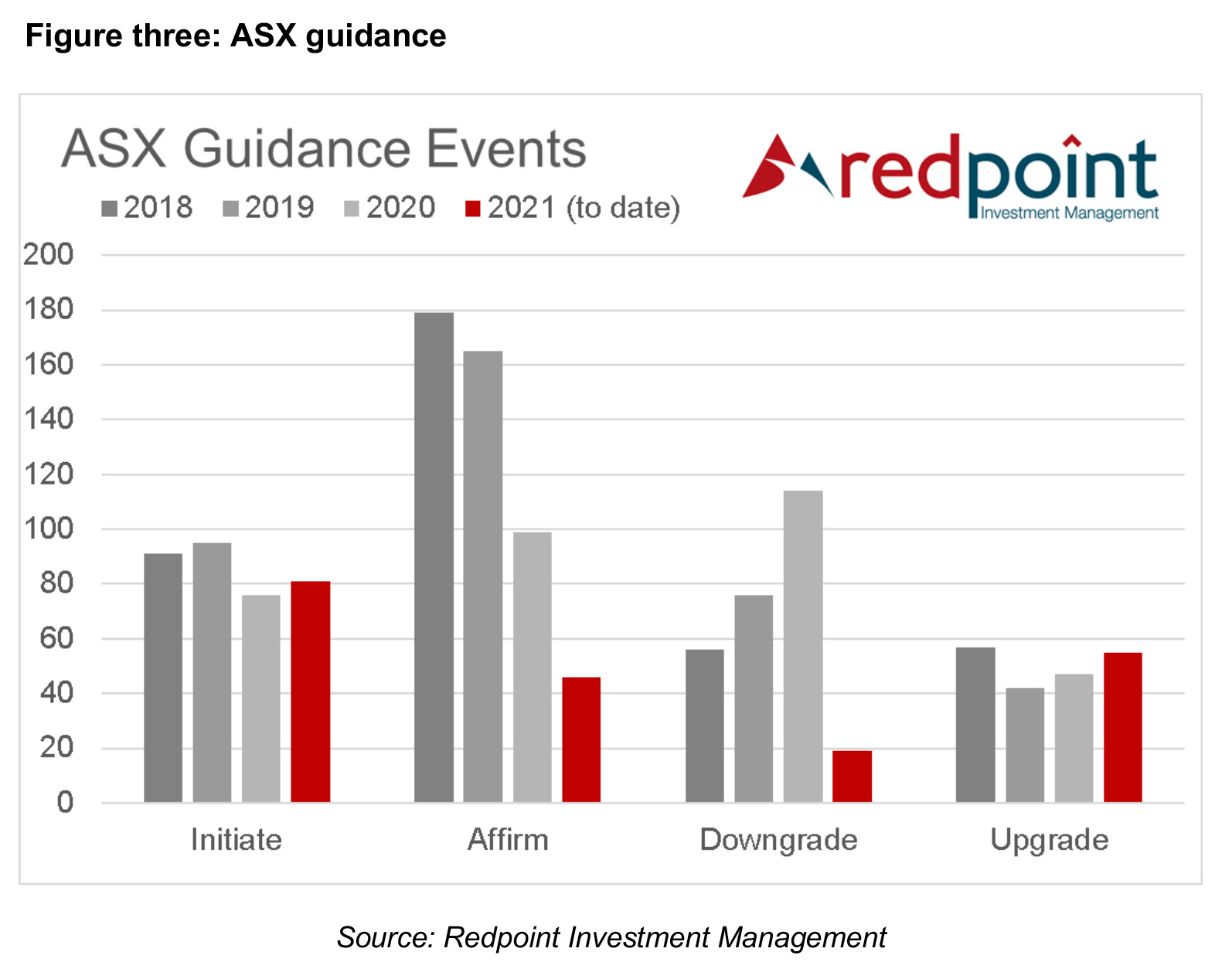

Figure three indicates the number of distinct events where company management has either initially provided a profit expectation and then have subsequently affirmed, downgraded or upgraded their guidance. It shows that 2020 was an interesting year: earnings guidance was not affirmed as many companies simply withdrew their earnings guidance, and there were many more earnings downgrades due to the unknowns of the COVID-19 pandemic.

So far in calendar 2021, there have been few downgrades as companies are reinitiating with conservative expectations, but we still have the upcoming AGM season where there may be some downgrades due to the impacts of extended lockdowns in NSW and Victoria.

Investors need to be wary of downgrades or a lack of guidance from companies trading at high valuations as no news – or bad news – could lead to a share price de-rating. For example, companies such as JB HiFi, Bunnings and Officeworks owner Wesfarmers, and Carsales Ltd may guide more conservatively for 2022 if COVID reopening and a shift in consumer spending back towards services and leisure is expected to slow their revenue growth next year.

Investors also need to watch the number of companies affirming any guidance they presented at their 30 June results announcement. For example, Redpoint will be keeping an eye on those companies with a 31 December balance date, including energy and mining giants Woodside, Oil Search, Santos and Rio Tinto, Engineering group Cimic and car dealer Eagers Automotive.

The other key area to monitor will be commentary regarding costs as an indication of whether inflationary pressures are expected to be transient or ongoing.

From a dividend perspective, in the year ahead, further rises in profitability and dividend payments are expected from:

- mining companies, including BHP, Rio Tinto and Woodside

- James Hardie, driven by ongoing growth in the US market

- offshore toll road owner Atlas Arteria, which owns toll roads in the US and Europe (France and Germany) and will benefit from increasing mobility over the Christmas period and into 2022

- healthcare group Healius, which is well placed with its network of pathology labs and diagnostic testing facilities and is expected to see increased activity into 2022.

The goal for most income-seeking equity investors should be to earn a consistent and above average yield on their capital and including an appreciation of the calendar and industry profit cycles can assist with this goal. While the last year has been one of the most challenging in history, it has also highlighted the opportunities for a more dynamic perspective into how investors should seek to capture income from equities.

This is the approach adopted by the Redpoint Australian Equity Income Fund, a diversified Australian equity portfolio that aims to capture an above average income yield for investors who are in retirement or at a zero tax rate. The focus is on delivering a growing income over time, as well as being able to keep up with inflation and the cost of living for retirees over their entire retirement period.

—–