2022 Financial Adviser Regulatory Agenda – Key dates and developments

2022 will still see plenty of action on the regulatory front.

The collective sigh of relief from advisers, licensees, and industry associations when the calendar turned over to 2022 could be heard all around Australia.

After the tumult of 2021, which saw advisers face almost unprecedented levels of reform (including DDO, IDII, new fee disclosure and consent rules, and the removal of grandfathered commissions), the pace in 2022 promises to be slightly more relaxed.

But of course, everything is relative, and 2022 will still see plenty of action on the regulatory front, as well of course as a Federal Election and all the curve balls we may see in its aftermath.

As well as a number of important reforms becoming effective this year, several government reviews and consultations directly impacting financial advisers are also due to commence, and this article – summarising key dates and developments for 2022 – is intended to ensure advisers stay on top of all the important issues that will shape the future landscape.

FASEA becomes FSCP; the debate around adviser professional standards continues

After all the hype and bluster, the death of FASEA came with a whimper rather than a bang. On 1st January 2022, as per the terms of the Better Advice Act[1], Federal Treasury assumed responsibility for FASEA’s standard-setting obligations, while ASIC’s Financial Services and Credit Panel (FSCP) had its responsibilities expanded as it became the industry’s new Single Disciplinary Body. Administration of the financial adviser exam also passes to ASIC.

With the FASEA site now archived, advisers seeking information about the mandatory Code of Ethics, or other professional development requirements, must now visit a new Financial Adviser Standards site, hosted by Treasury.

Whilst ASIC is yet to issue guidance on the operation of the FSCP, a statement at the end of December 2021 clarified that “The powers of the FSCP under the act include the power to direct financial advisers to undertake specified training, counselling or supervision and to report certain matters to ASIC”[2].

Furthermore, “An FSCP may also: suspend or cancel a financial adviser’s registration; issue infringement notices in specified circumstances; recommend that ASIC commence civil penalty proceedings; and enter into enforceable undertakings with financial advisers.”

But whilst this simplification of adviser oversight may represent some welcome certainty, it seems that the professional development landscape remains as changeable as ever. With politicians on both sides mindful of the continually shrinking adviser population (which fell below 19,000 in late 2021, a 5-year low[3]), a proposal by the Federal Labour opposition to scrap degree requirements for advisers with 10 years or more professional experience was quickly matched by the Federal Government, who have released a consultation paper on the topic[4].

Interestingly, these announcements split the adviser community, with many decrying them as a backward step on the journey to improve the professionalisation of advice and rebuild consumer trust.

Another dialogue which remains live and ongoing in 2022 is that around the problematic Standards 3 (conflicts) and 6 (limited advice) of the Code of Ethics. As the new Code custodians, it is now Treasury with whom the various lobby groups will be engaging.

Compensation Scheme of Last Resort (CSLR)

The 2017 Ramsay Review[5] into Financial Services external dispute resolution made 3 key recommendations around a compensation scheme of last resort, primarily to cover uncompensated client losses resulting from failures in personal financial advice.

(The Hayne Royal Commission subsequently recommended giving effect to all three of Ramsay’s proposals).

One of the key drivers of the need for such a scheme was the instance of claims against insolvent AFSLs who were no longer covered by professional indemnity insurance.

Data released by the Financial Ombudsman Service (which folded into AFCA) showed that historically, around 55% of unsettled determinations related to financial advice, and 13% related to Managed Investment Schemes[6].

Despite this, MIS are not in scope, with in scope products those that are authorised to be provided by AFSL and Australian Credit Licence holders that are required by legislation to be Australian Financial Complaints Authority (AFCA) members.

Excluding MIS will see most of the burden – around 76% in fact[7] – of funding the scheme borne by financial advisers.

Whilst the expected annual cost per adviser is relatively modest (around $300 according to official figures[8]), against a backdrop of many other cost increases facing advisers (including recent steep rises in the ASIC Levy), the proposed funding model has attracted widespread condemnation from various stakeholders including individual licensees and industry associations.

One of the more vocal critics has been Don Trapnell of Synchron, who noted that the 5-year-old data used by policymakers was no longer representative of advice complaints landscape. According to Trapnell, AFCA data to the end of June 2021 showed that of 70,510 total complaints, only 997 (1.4%) involved financial advice, and of those, only three went unsettled[9].

To this stage, such complaints have fallen on deaf ears, and the design of the scheme – currently before Parliament and expected to become law at some stage during 2022 – has largely remain unchanged from that originally proposed.

The maximum payout under the scheme would be capped at $150,000[10].

Quality of Advice Review

Courtesy of Hayne, conflicted remuneration is very much on the agenda in 2022, across life insurance, general insurance, and mortgage broking. The Life Insurance Framework (LIF) review, originally intended as a standalone review conducted by ASIC, has now been rolled into the broader ‘Quality of Advice’ Review, to be conducted by Treasury in 2022 (exact timings TBC).

The Terms of Reference for the review[11] – intended to examine issues outstanding from Hayne as well as the effectiveness of historic reforms – were released in December 2021, and include the following areas

- Financial advice disclosure requirements including statements of advice

- Recent reforms to introduce annual renewal for ongoing fee arrangements

- The life insurance remuneration reforms, and the impact of the reforms on the levels of insurance coverage

- The level of demand for advice and the needs and preferences of consumers

- Opportunities to reduce compliance costs on industry, while maintaining adequate consumer safeguards.

According to some experts, the dialogue around advice has changed markedly since the Royal Commission, with the retreat of the banks, new professional development standards and a number of reforms contributing to a clear improvement in advice standards, as measured by AFCA complaints[12]. Furthermore, the penny has also dropped in terms of the dire consumer impact of the dramatic shrinkage in adviser numbers. The accessibility of advice is decreasing while the costs are increasing, leaving policymakers on both sides of politics worried. The about face on degree requirements, discussed above, is just one example of how thinking is evolving.

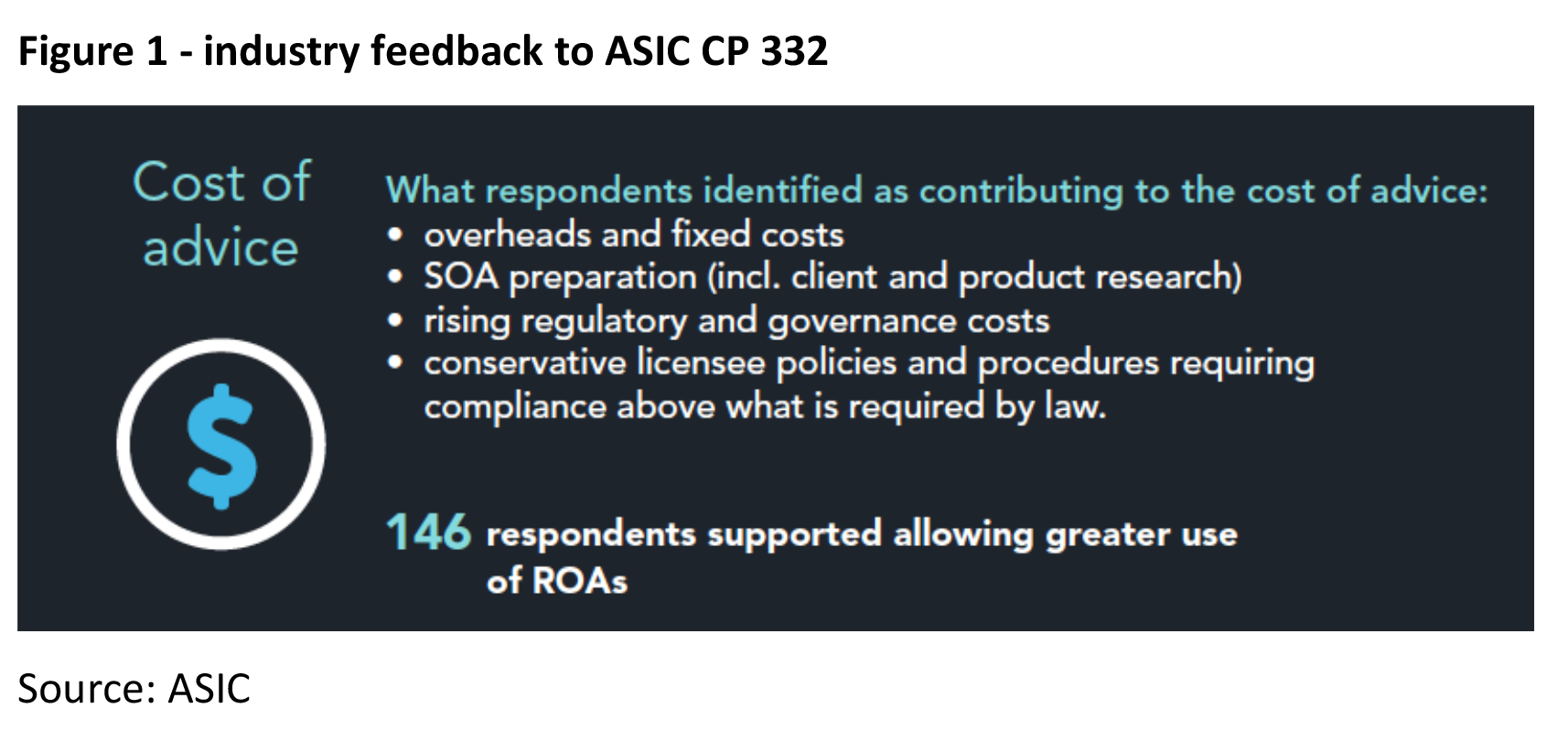

The Quality of Advice (QOA) Review could thus end up focusing more on the affordability of advice, rather than the quality per se. ASIC, who will be contributing to the review, already have a solid base of stakeholder feedback to input into this process as a result of their 2020 Consultation Paper 332 Promoting access to affordable advice for consumers. A high-level summary of this feedback was published as an infographic[13], an extract from which is included below:

The outcomes of the QOA review will have far reaching consequences for advisers.

A complete reset of compliance requirements in advice is possible, and indeed ASIC has already signalled that a broader use of ROAs is on the agenda[14].

On the life insurance front, the outcomes could potentially be even more seismic, with the future of life insurance commissions to be decided. Whilst the rhetoric of Hayne, consumer advocacy groups and sections of the media was very much about the abolition of commissions, the downward trend in adviser-initiated policy replacements since the 2018 implementation of LIF[15] may have softened the position of some. Certainly, shadow Financial Services Minister Stephen Jones (who could be in the big chair depending on the Federal Election outcome) has toned down his previously strident position and following consultation appears more open to consider commissions as a way of balancing the “need for consumer protection with the need to retain a financially-viable financial advice industry.”[16]

With an abundance of research[17] reinforcing the inability and/or unwillingness of most life insurance customers to pay an out-of-pocket advice fee, the abolition of life insurance commissions would drive a dramatic drop in life insurance advice, and overall insurance uptake. Even the retention of commissions at existing rates wouldn’t necessarily be cause for celebration amongst advisers, with the current 60% upfront seeing life insurance advice a loss maker for many. Only a dramatic reduction in the cost of providing such advice would right a ship that has been sailing on very choppy waters for the last few years.

Commissioner Hayne recommended the review be complete by 31 December 2022 at the latest.

Other key 2022 milestones

July 1st Retirement Incomes Covenant (RIC) heralds a wave of new product releases

One policy instrument that has flown under the radar is the Retirement Incomes Covenant. Effective July 1st, 2022, the RIC will formalise requirements for super funds to offer regular, lifetime, income-based solutions for retiring members. (Members are not obliged to use these solutions).

On a practical level, advisers are likely to notice a deluge of new retirement income products coming to market and an increase in the demand for advice around such products. To the extent that some larger funds may choose to develop their own products, based on their own fund’s experience data, the breadth and variation in underlying offerings certainly comes with its own set of challenges for advisers as they seek to become familiar with the evolving landscape.

July 1st APRA Superannuation Prudential Standard (SPS) 250 effective

Another change stemming from the Royal Commission is APRA Prudential Standard SPS 250, which aims to improve member outcomes in relation to life insurance. SPS 250 will require trustees to:

- Strengthen arrangements to protect members from potential adverse outcomes caused by conflicted life insurance arrangements, including robust decision-making in the negotiation and ongoing review of insurance arrangements

- Obtain an independent certification of related party insurance arrangements before entering into, or materially altering, an insurance arrangement and on a triennial basis; and

- Strengthen data management to improve analysis of member outcomes across different groups of superannuation fund members.

In practical terms, members could expect to the changes to facilitate easier opt-out processes and exert downward pressure on premium rates.

October 1st – IDII 5-year contract terms

Deferred from the original 2021 launch date[18], the last of the major APRA interventions into individual disability income (IDII) comes into effect on October 1st, 2022, when new income protection policies will be subject to a maximum contract term of 5 years. Under this intervention, designed to improve the sustainability of income protection by allowing insurers to adjust policy terms in response to major, unforeseen, social, and economic developments, life insurers must issue policyholders a new contract at the end of 5 years. Whilst policyholders will not be subject to health underwriting under this process, there is a definite possibility that the terms of the new policy may well be less generous than the one being replaced – representing a major departure from the usual convention that policyholders never be left worse off when being moved to new contracts. Policyholders of course can choose not to take up the offer and seek coverage elsewhere (subject to underwriting of course).

Note that this change does not mean that benefit periods are limited to 5 years.

Just like the RIC, this change will herald both a new set of market offerings to become familiar with, and an increase in the demand for related advice.

Other conversations to stay abreast of

There is always something happening in financial services, and in addition to the locked in dates and reviews and new legislation described above, there are many other industry dialogues on which advisers should keep a keen eye.

These include the Australian Law Reform Commission process to simplify financial services law[19]. Due to hand down recommendations in 2023, this process could see many significant outcomes, including the creation of a new legislative category for financial advice (which is currently bracketed with other ‘financial products’). This process is very much live, and advisers should expect much media commentary over the coming months.

Also worth keeping an ear to the ground for is the developing story around the Sophisticated Investor definition. Modelling conducted by Australian National University found that the percentage of Australians meeting this definition has grown from 1.9% in 2022 to 16%, or around 3 million people[20]. Projections suggest this could blow out to nearly half the population in the next 20 years. And the reason why? Real estate prices. The lack of indexing in the test and spiralling real estate prices mean more and more people are meeting the threshold ($2.5m in net assets or annual income of $250k). Any dramatic increase in people accessing riskier products, with lower disclosure requirements and lower protections against inappropriate advice and conflicted remuneration, is fraught, and comes with with major ramifications for investors and advisers alike. This is one story advisers should definitely keep an eye on.

Conclusion

Although, in relative terms, 2022 might give advisers the opportunity for a brief, regulatory, breather, there is still much for advisers to be aware of, understand, and implement. The year will see key legislation and regulations launched which will herald a proliferation of new products across life insurance and superannuation. A major review into advice has the potential to dramatically reshape the landscape. And, bubbling away in the background, are a number of other dialogues with potentially far-reaching consequences. Advisers staying abreast of these developments will far better equipped to serve their customers, meet their compliance obligations, and remain agile enough to adjust their business model to the new opportunities and challenges these changes developments could bring.

———