What Britney Spears can teach advisers about guardianship and consumer protection

The increasing incidence of dementia has been likened to a ticking time bomb for financial advisers, as the reduced mental capacity of clients brings into question the validity of consents.

Introduction

If we were to ever appoint a Patron Saint of Financial Advice and Estate Planning, a pretty strong case could be made for Britney Spears. Because, thanks to the worldwide attention garnered on her involuntary ‘conservatorship’ case, people everywhere are starting to wake up to the archaic, arcane, and sometimes frightening consequences of having financial, lifestyle, and even healthcare decisions made on your behalf by a person, or an institution, you didn’t choose.

Closer to home, stories about guardianship gone wrong are, sadly, neither new nor uncommon. Recently however, a slew of stories about people involuntarily falling under the control of public trustees, and the devastating financial and personal consequences they suffered as a result, has put the issue very much front and centre of public discourse.

Financial Advisers play a central role in helping their clients grow, safeguard, and eventually distribute their wealth. In the context of an ageing population, and the associated increase in people with diminished decision-making capacity, they are often close to the centre of this discourse.

Amongst the many lenses this topic can be viewed through, one of the most important, and relevant, for financial advisers, is that of consumer protection.

In this article, we will examine the mechanisms and instruments that advisers should be aware of, and in some cases can facilitate, to protect the interests of their clients, including Powers of Attorney, Guardianship, and Special Disability Trusts. Scenarios where these mechanisms are especially relevant will be examined, as will be the ways advisers can gain confidence in the decision capacity of their clients, and why this is important.

A system designed to help those who can’t help themselves

Across Australia, tens of thousands of people[1] have had the ability to make decisions about their health, lifestyle and finances taken away from them, and given to state appointed guardians and trustees.

Guardianship is a system designed to protect the vulnerable. Representatives of the state — supposedly as a last resort — act as an administrator for someone’s finances and care in order to protect them from physical and financial abuse and neglect if there is no one else to do so.

Whilst the specific span of their powers varies from state to state, guardians are generally making decisions about where people can live, who can visit them, and what medical care they can receive.

Public trustees manage the finances of these people (currently worth about $15 billion[2]). They decide where their money should be invested and what personal items should be sold.

Sadly, however, it seems that in many cases, the system created to protect the most vulnerable in our society – especially the old and the disabled – is failing them badly.

Horror stories abound

People are being involuntarily moved into aged care, their health wishes ignored, their belongings sold, and their assets mismanaged. In some cases, contact with their family has been cut. Even more galling, they are being charged exorbitant fees for the privilege. And, akin to some dystopian nightmare, people under guardianship orders cannot be publicly identified, and should they try to ‘escape’ the system, the Public Trustee can use the individual’s own money to fight them.

One story, out of dozens that could be told, is that of Jan[3]. A previously active 81-year-old, Jan broke her hip, was taken into hospital, and declared by a bedside tribunal to be unfit to make self-care decisions due to dementia (a point disputed by her family). The Power of Attorney granted to her son was overturned, predicated on a disagreement he had with his sister about their mother’s care. Placed under state guardianship, Jan was put into aged care, where she spent the last 2 years of her life, sedated and medicated. The two and a half years Jan was under the authority of the public trustee cost her close to $100,000. The trust charged her around $22,000 in capital commission, $10,500 in accountancy fees, $25,000 in in-house legal fees plus another nearly $30,000 in external legal fees, and $4300 on gardening fees for her property.

Other stories include two recently reported by the ABC[4]. They told of Chris, refused access to his own half a million-dollar savings to formally fight his guardianship orders, and of Peter, a long-term brain injury sufferer now struggling to make ends meet after the Public Trustee liquidated his share portfolio and ate it all up in hard to explain fees, including $14,000 in realty fees to ‘manage’ 4 bush blocks that were only worth $20,000 in total.

Why this increasingly matters to Financial Advisers

Australian financial advisers will increasingly find themselves in involved in issues of guardianship, either on the periphery or even at their very centre.

This is a function of both the unique role advisers play in their client’s lives – privy to many deeply personal discussions about family, finances, and health – and some powerful societal trends related to our ageing population:

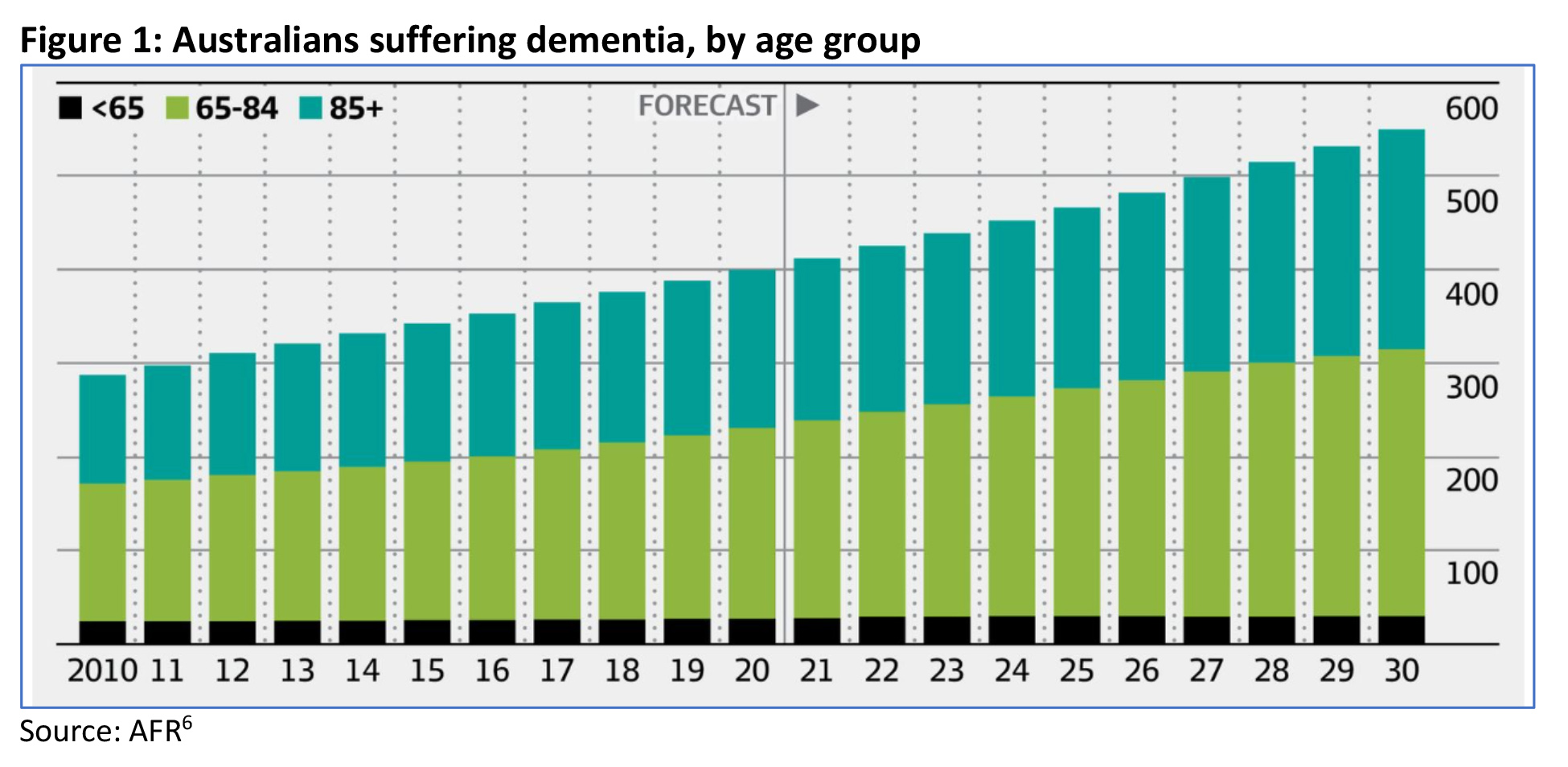

- the increased incidence of dementia (see Figure 1) means an increase in people of diminished decision-making ability

- changes in family structures mean that blended families are far more common, with an estimated 1 in 10 families ‘blended’ or stepfamilies[5]

- a multi trillion-dollar intergenerational wealth transfer is starting to take place.

The combination of these forces means that we will see increasing numbers of vulnerable people incapable of making their own decisions, and an increasing frequency of familial disputes around how to manage those people’s finances and health care. (According to some estimates, 80% of all legal actions are blended family disputes[7]).

In simple terms this means an increasing likelihood that your retiree clients, or your SMSF clients, or your small business clients, will either become need guardianship or become guardians themselves.

All of which will see the role of ‘living estate planning’ instruments take on an increasingly critical role in the adviser’s strategic toolkit.

Living Estate Planning Mechanisms

The essence of ‘living estate planning’ is the ability of spouses and children to easily – legally – make decisions on behalf of a person who has lost their capacity to do so themselves.

Instruments that can help give a voice to the vulnerable include:

- Enduring Powers of Attorney

- Enduring Guardianship

- Special Disability Trusts

- Advanced Care Directives.

Enduring Power of Attorney

Granting Power of Attorney (POA) to someone means authorising them to make financial and legal decisions on your behalf. This can include operating bank accounts, paying bills, investing money, selling, or buying property and instructing a solicitor to act in legal proceedings. It precludes any health care decisions (for which a dedicated Medical Power of Attorney can be made).

A general POA, which can be revoked by the nominator at any time, is only valid whilst the nominator retains their decision-making capacities.

An enduring POA on the other hand remains valid even if the nominator loses their decision-making capacity, and as such is the more appropriate and robust mechanism to protect clients.

A person is not able to grant any form of POA once their decision-making capacity is diminished, meaning these mechanisms need to be put in place in advance (typically at the same time as other estate plans are made).

Note: question of ‘capacity’ is a complex one, as different states have different definitions for what constitutes capacity.

Enduring Guardianship

Once a person loses their ability to make decisions for themselves, appointed Guardians can make decisions about:

- medical and dental treatment

- health care

- living and lifestyle arrangements

- the use of support services.

The nomination of an Enduring Guardian can only be made whilst the nominator still has decision making capacity. Meaning, if your client wants to choose who that Guardian is, they need to do so preemptively. Otherwise, an application will need to be made to the relevant state government authority, who will then decide who to appoint.

Whilst in normal circumstances this would be the family member or loved one making the application, the process can be long and expensive, and the outcome is not guaranteed. Some of the stories referred to above owe their roots in family disagreements, which in turn saw guardianship and trustee powers to granted to the state authorities.

Special Disability Trusts

Clients with disabled children will want to do their utmost to ensure that child’s interests are protected when the client themselves is no longer able to do so. Depending on the level of disability and the client’s capacity, consideration should also be given as to whether a special disability trust (SDT) might be appropriate.

An SDT can be established only for someone who is severely disabled. The majority of the funds must be used for care and accommodation and the trust is required to have either two trustees or a professional trustee appointed. SDTs can be created during a client’s lifetime, or as part of a client’s will to take effect on the death of the last surviving parent.

SDTs allow for capital (up to a threshold) and income to be exempted from means testing. This means parents and relatives are able to provide for a severely disabled beneficiary without it affecting any entitlement to the disability support pension.

The trust beneficiary (the child) can have up to $700,250 (correct @ 1/7/21 and indexed July each year[8]) of exempt assets – that is, assets exempt from the Centrelink assets test. Their principal residence is also exempt.

Eligible family members who gift assets up to $500,000 to the trust (in total) may receive an exemption from the usual Centrelink gifting rules. This may help to increase their own entitlement to Centrelink.

Advanced Care Directives

An Advanced Care Directive formalises a person’s Advanced Care Plan, setting out their wishes, needs, values and preferences around their future care, including medical treatment. They are used in the event the individual does not have capacity to communicate their wishes. Details covered generally include resuscitation, medication, and a substitute decision maker. Whilst the exact requirements differ from state to state, Advanced Care Directives are generally legally binding.

The ticking ‘capacity’ timebomb

Many experts believe trends around dementia and other conditions that impact mental capacity increase the risks of poor financial decision making and consumer harm. In the context of best interest duty and informed consent this could become increasingly problematic for financial advisers, especially as many lack the training to be able to spot cognitive decline.

The extent of this problem could be exacerbated amongst ageing SMSF Trustees, more than half of whom are over 60, with the highest percentage between 65 and 74, according to ATO analysis[9].

Experts believe this a potential ‘recipe for disaster’ because of the risk they will suffer some form of mental impairment while still controlling the bulk of the $800 billion invested in SMSFs around Australia.

As discussed above, the best strategy for protecting long-term interests is to put plans in place and appoint an attorney who is known, and implicitly trusted, before the onset of cognitive decline. In the context of SMSFs this seems particularly vital, with one expert going so far as to suggest the appointment of an enduring POA should be compulsory for anyone wishing to establish an SMSF[10].

How to spot cognitive decline

Advisers can face many challenges when working with clients who they believe may have limited capacity.

As well as being a complex area, with definition and assessment guidelines varying from state to state, it is also a highly sensitive topic which can place strain on relationships with clients and their family members.

Whilst it is clearly not the role of advisers to decide the mental capacity of their clients, the nature of the financial decision-making means advisers should be alert to the red flags that may suggest a deeper problem. Commercial law specialist Peter Townsend suggests a number of steps[11] advisers can take if they have concerns about their clients:

- Is there any reason to believe – based on objective evidence – that the client does not have full mental capacity?

- If possible, obtain additional evidence or assessment of the situation from independent third parties, which may include the client’s doctor and lawyer.

- At meetings with the client, have an independent witness with you who can attest to what was said by the client and their apparent capacity.

- To assess their capacity, ask questions that require a considered response, rather than simple yes/no questions. For example, rather than asking a question like ‘you want to give your daughter $30,000, is that correct?’, instead ask, ‘why are we meeting today?’ and ‘how much do you want to give your daughter?’, and ‘why that amount?’.

- If you firmly believe the client is not mentally capable your next question is whether anyone has their enduring power of attorney and can make decisions about their financial strategies. If not, and if it would be materially detrimental to the client to put your recommendations on hold, advise the client’s family that they should make an application for the formal appointment of a guardian to look after the client’s interests. There are 8 separate guardianship jurisdictions in Australia (six states, two territories) with different requirements in each.

- It is not advisable for a financial adviser to apply to be appointed as their client’s financial guardian as the potential for accusations of self-interest is too high and the need to evidence complete independence too great.

The downside(s) of putting plans in place

The benefits – emotional, financial, and physical – of putting proper plans in place are self-evident. However, this does not things always go smoothly, even when trusted family members are appointed.

In the wrong hands, powers of attorney can clearly underpin financial abuse – allowing attorneys to make decisions in their own best interests. While this is not legal, it can be hard to detect.

Fortunately, Powers of Attorney can be overturned in certain circumstances, including if the attorney or guardian is not acting in the best interests of the nominator/principal.

Applications to revoke a POA can be made to the relevant state-based tribunal, or to the Supreme Court (a more complex, lengthy, and expensive option).

The other potential downside risk is for those who are actually appointed as Attorneys and/or guardians but who aren’t aware of some of the legal obligations that fall to them.

The Australian Law Reform Commission noted: “The key issue with private guardians and private financial administrators is a lack of knowledge and understanding of their roles and responsibilities. Abuse of older persons by private guardians or private financial administrators may therefore be inadvertent. For example, private financial administrators may be unaware of the requirement to keep the assets of the person separate from their own. Informal arrangements in place prior to the commencement of the order may persist, which may involve conduct in breach of the appointment.”[12]

Summary

The ageing of Australia’s population is proving to be the catalyst for a number of powerful emerging trends, including a burgeoning wealth transfer, the increased prevalence of dementia and similar conditions, and a growing incidence of family disputes. These trends threaten to put the adviser at the centre of a storm which can undermine the wellbeing of their clients.

The unique role financial advisers play in their client’s lives puts them at the very centre of a growing public discourse about elder abuse and diminished capacity. As such it is vital that advisers stay abreast of this discourse and make themselves aware of the tools and techniques, they can use to protect the interests of their clients.

——–