QAR and the future of Limited Advice

To the extent that limited advice can overcome consumer barriers to advice would be a game changer.

QAR – are we closer to solving the limited advice conundrum?

One of the most longstanding and contentious issues within financial advice is that of limited (or scaled, or episodic) advice. For some time now there has been a philosophical gap between ASIC, who have publicly encouraged the provision of more limited advice, and licensees who feel that regulatory ambiguity represents too much of a risk to take. The main losers from this disconnect, are consumers, who have a proven preference for limited advice, a preference driven mainly, but not solely, by cost factors.

The widespread reluctance to provide limited advice represents a major barrier to making financial advice more accessible to Australians, a fact recognised and called out in the recently released Quality of Advice Review (QAR) Final report. While some of the proposed changes to advice regulation will undoubtedly increase the appetite to provide limited advice, the scope of the Review excluded the FASEA Code of Ethics, leaving a major barrier to limited advice unaddressed. In the absence of any certainty, the future of limited advice therefore remains somewhat cloudy.

In this article we will review issue of limited advice from several perspectives: the consumer demand, ASIC’s guidance, and the FASEA standard that has been interpreted as a regulatory roadblock to making limited advice more widely available.

Michelle Levy on limited advice

A search of the Final QAR report[1] will reveal 17 mentions of the term ‘limited advice’. While this may not seem much in a 267-page document, the context in which that term appears leaves no doubt that Michelle Levy recognises that solving the limited advice conundrum is absolutely central to improving the accessibility of financial advice in Australia.

“High quality advice is not always, and perhaps not often, comprehensive advice – it is advice that responds to the needs of consumers. Many consumers need incidental, simple, and limited advice, sometimes frequently. It is in the interests of consumers to be able to get financial advice as and when they need it.”[2]

Michelle Levy

Consistent with this importance, many of her proposals are designed to facilitate the improved accessibility and flexibility of advice.

Consumer demand for limited advice

As referenced by Levy, consumer demand for limited advice is significant, and likely to grow further due to two structural shifts in the investor landscape – the beginning of the intergenerational wealth transfer, and the surge in new share market investors, a trend which began during the pandemic, and which has been particularly strong amongst millennials.

The consumer preference for limited advice has been well documented for many years.

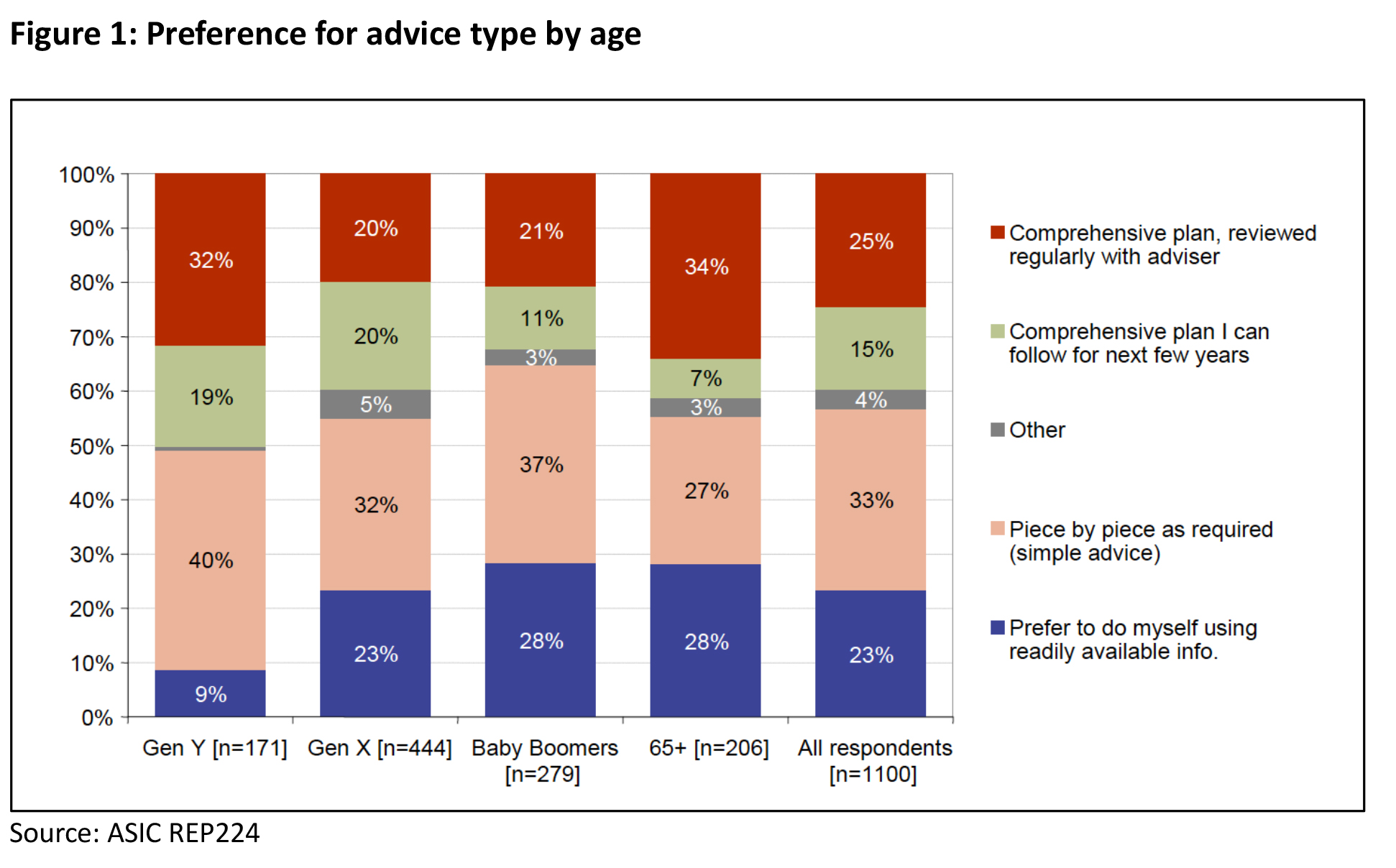

In 2010, ASIC Report 224 ‘Access to Financial Advice in Australia’[3] uncovered several themes:

- In aggregate, more consumers prefer limited (‘piece by piece’) advice over comprehensive ongoing advice

- The preference for scaled advice was highest amongst Millennials (whose lower income levels would make the affordability of comprehensive advice more challenging)

- Under 65s had an overwhelming preference for one-off – rather than ongoing – engagements with an adviser (regardless of whether that engagement was for limited or comprehensive advice).

Fast forward several years, and these findings have been validated by more contemporary data.

- Research by the Conexus Institute found that 40 per cent of consumers wanted advice on a topic-by-topic basis, while 35 per cent wanted a comprehensive plan which was reviewed from time to time. A smaller proportion (22 per cent) wanted a comprehensive plan that they could follow for the next few years.[4]

- Research by Investment Trends in 2021 found that 11 per cent of consumers wanted comprehensive advice, while 38 per cent wanted limited advice.[5]

- Also in 2021, an Investment Trends survey of High-Net-Worth clients found that just over half (52%) were happy to use the services of a financial adviser, but only to validate their own thoughts (via limited advice)[6].

Where do licensees and advisers sit on scaled advice?

A longstanding supply-side reluctance/inability to meet market demand for limited advice has been amplified in recent years.

There are three main drivers of this:

- advice has become more expensive to provide

- perceived lack of regulatory certainty around the legality of limited advice

- declining adviser numbers are reducing the competitive imperative to provide scaled advice (the remaining advisers can stay busy purely focusing on clients seeking comprehensive advice).

Economic barriers

In 2021, KPMG benchmarked7 the cost to produce comprehensive advice at $5334. With an average advice fee charged to the client of around $2,000 less than this, comprehensive advice is a loss maker.

The prevailing view amongst most licensees is that, in order to be compliant, the same amount of work needs to go into producing scaled advice as comprehensive. To the extent that scaled advice would likely involve less opportunities to recoup the loss made on the initial advice, the economic challenges of scaled advice become clear.

Perception that limited advice contravenes FASEA standards 2 and 6

The KPMG research mentioned above, revealed a firm belief among many licensees that scaled advice contravenes standards 2 and 6 of the FASEA Code of Ethics, which requires an adviser to collect extensive information on a client’s circumstances beyond needs, objectives and wants, in order to consider the broad consequences of any single piece of advice.

The research concluded that:

“Concerns with these standards results in risk adverse (sic) licensees imposing greater obligations on advisers to make greater inquiries and consider matters broader than the client’s intended advice needs and scope. Respect of client needs is paramount as they often wish to limit the disclosure of information at first advice and feel more comfortable disclosing more information once they get to know their adviser. It is the view of research participants that the Code does not permit scaled advice.”[8]

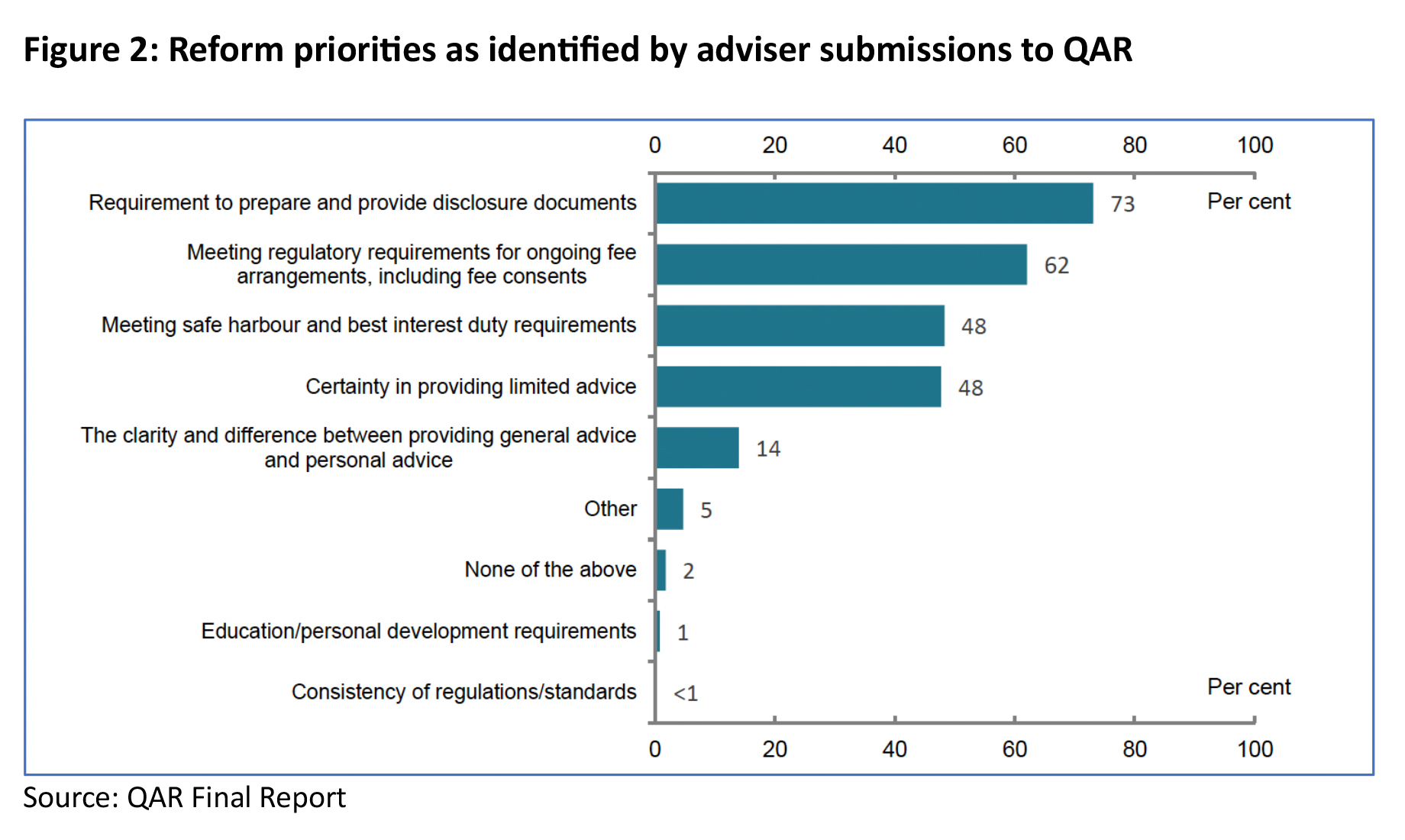

This general lack of confidence in providing limited advice was displayed in the QAR Final Report, which highlighted ‘Certainty in Providing Limited Advice’ as a major way the regulatory burden on advisers could be reduced.

Why Limited Advice isn’t just about providing cheaper advice

Cost isn’t the only barrier to advice that can potentially be overcome by limited advice.

Across numerous studies undertaken locally, and around the world, over a number of years, consumer cite two other major reasons for not engaging an adviser:

- the lack of complexity of their situation, or size of their investment, doesn’t warrant advice

- they enjoy managing finances themselves.

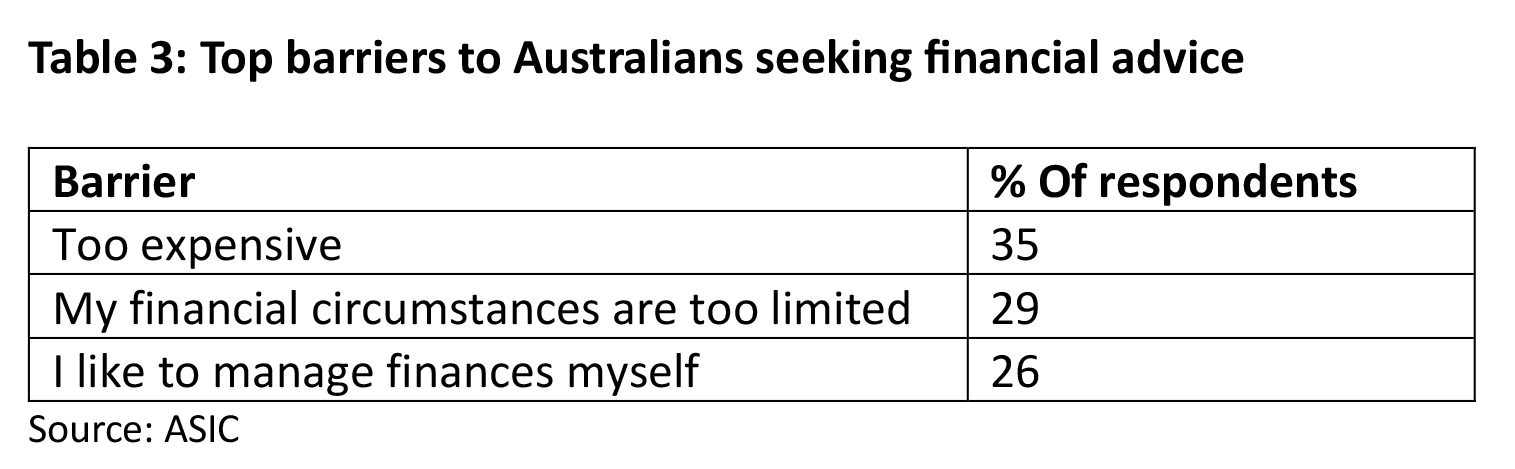

This was quantified by ASIC in their 2019 study[9] of attitudes towards financial advice:

Could it be then that there is a problem in the structure of advice that needs to be solved?

it is tempting to look at the barriers to people getting advice – cost, the desire for more control, not having complex enough affairs to justify it – in isolation of each other and set out to fix them accordingly.

But is the underlying issue actually one which combines all these elements?

Is the real problem the fact that financial advice is perceived as an all or nothing proposition? A proposition where the advice relationship is seen as one in which:

- Tthe advice must be comprehensive complex and ongoing

- the adviser has total control over initial and ongoing investment decisions

- a recurring fee of thousands of dollars is charged.

And is limited advice the offering that overcomes all these barriers at once? Michelle Levy certainly hopes so.

For its part, ASIC encourages limited advice

In 2020, ASIC Commissioner Danielle Press reiterated the corporate regulator’s belief that limited advice should play a crucial role in the industry, and questioned the extent to which licensees and their compliance divisions playing it too safe was actually to the longer-term detriment of advisers and their clients[10].

Recognising and reacting to industry feedback on the lack of clarity around how to provide limited advice in a compliant way, ASIC issued Information Sheet 267: Tips for Giving Limited Advice in December 2021[11].

INFO 267 provides tips and summarises the relevant guidance from RG 175 (Licensing), and RG 244 (Giving information, general advice and scaled advice). It includes information on what advice providers can do to meet their obligations under the law, including the best interest’s duty and related obligations as well as the FASEA Code of Ethics when giving limited advice.

Commenting on the launch of INFO 267, ASIC Commissioner Danielle Press said:

“ASIC recognises that many consumers prefer to seek limited and specific advice rather than comprehensive advice. We also understand that industry faces some barriers to providing limited advice, including a lack of clarity about the regulatory requirements.

We expect this guidance will provide regulatory certainty to industry and help reduce compliance costs. It will assist financial advisers in their efforts to make these forms of advice more available to consumers and assist them in delivering quality advice in a timely, affordable, and compliant manner.”[12]

The detail of INFO 267: Tips for giving Limited Advice

INFO 267 has two sections. First, the overview of giving limited advice, covering

- What is limited advice?

- Best interests duty and related obligations when giving limited advice.

- The safe harbour.

Second, ASIC’s tips for limited advice, covering:

- using professional judgement when identifying subject matter and scope

- communicating the service you are providing and scoping implications

- taking active steps to identify and inquire about your client’s relevant circumstances and obtain complete information

- using processes and systems.

INFO 267 also includes a sample limited advice SOA.

Advisers considering providing Limited Advice are encouraged to remember the following:

- you can limit the scope of all types of advice, including advice about complex issues

- limited advice can include advice on a single topic or advice on multiple topics

- you can adjust the level of your inquiries to reflect the nature of the advice sought

- you should not reduce the scope of advice to exclude critical issues that are relevant to the subject matter

- you must explain what advice you are providing and what advice you are not providing

- limited advice is not lesser quality advice

- while processes can be used to help you provide limited advice, you need to use your expertise, skills, and professional judgement as an advice provider to deliver good-quality limited advice and comply with your obligations.

What does the future hold for Limited Advice?

In her final report, Michelle Levy makes a total of 21 recommendations designed to ultimately make advice more accessible. Largely these recommendations revolve around reducing the amount of complexity and the compliance burden, with the two ‘Headline Recommendations” being the scrapping of SOA, and a requirement to give ‘good advice’, which essentially would see the scrapping of the Safe Harbour provisions – one of the major barriers to limited advice.

The Report notes:

“The good advice duty will make it easier for financial advisers to exercise their expertise and professional judgement when providing advice to their clients. They will no longer feel obliged to follow the safe harbour steps regardless of the nature, scope, or content of the advice they are providing. They will be able to follow the process they consider will most effectively and efficiently allow them to comply with their obligation to provide good advice to their clients. This flexibility will also ensure that the good advice duty does not inhibit the provision of limited advice in the same manner as the current best interests duty”.

Recognising the issues with FASEA, Levy goes on to say:

“Advisers have told us the Code of Ethics, especially Standard 6, is also an impediment to the provision of limited advice for financial advisers. While the contents of the Code of Ethics are outside the scope of this Review, I do urge the Government to consider this issue as part of its review of the Code of Ethics.”[13]

Financial Services Minister Stephen Jones has asked Treasury to consult on the Code in 2023, after the Government has considered its response to the Quality of Advice Review14.

Conclusion

Despite strong consumer demand and the exhortations and guidance of ASIC, many licensees are still choosing not to provide limited advice, for a combination of economic and risk management reasons. Many of the same licensees have said they would like to increase their provision of limited advice if these barriers could be overcome.

Should the QAR recommendations be accepted and implemented by the government, it is hoped this will go a long way to mitigating some of the financial and compliance challenges, with eyes now turned to the yet to be commenced FASEA Code review and the potential to remove perceived contradictions and inconsistencies.

To the extent that limited advice can overcome numerous consumer barriers to advice – not just cost – a more limited advice friendly regulatory regime would indeed be a game changer.