Ethics and your peers

What are some of the behaviours that feed ethical behaviour and how these can be advanced in the advice practice, so all employees act ethically?

Ethics and the values that underpin them provide a moral compass by which people live their lives. This article, proudly sponsored by GSFM, examines ways that a financial advice practice can support ethical behaviour across its business to provide quality financial advice that is always in their clients’ best interests.

The Ethics & Compliance Initiative (ECI) is a global organisation focused on research. Through this, ECI identifies the practices that improve ethics and compliance program effectiveness and build institutional culture strength.

In 2016, the ECI convened an independent panel comprised of ethics and compliance practitioners and academics, and challenged the group to identify common traits that typify “gold standard” ethics and compliance programs. The case for continually improving ethics and compliance practices and policies are underpinned by two key findings:

- The stronger the culture, the greater the impact; the importance of business culture is discussed in detail in the most recent article in this ethics series.

- The higher the ethics program quality, the stronger the ethics culture; 85 percent of employees working for organisations with a strong ethics culture indicated observing favourable outcomes.

As well as building a strong business culture with ethical practice at its foundation, it’s important that this does not extend only to advisers – this is reinforced by finding number two above. Ethics needs to be embraced by all members of your business, from your receptionist and administration team, advisers and paraplanners, IT and other support personnel. Each person has an important role to play in developing and maintaining a positive and ethical business culture.

Global Business Ethics Survey

ECI has conducted a longitudinal, cross-sectional study of workplace conduct from the employee’s perspective since 1994. This research, the Global Business Ethics Survey®, consistently demonstrates that the quality of a company’s ethics and compliance program and the strength of the company’s ethics culture are key when it comes to achieving desired ethics outcomes[1].

While there are many factors that influence ethical behaviour, the interplay of four major ethics outcomes are tied to the daily micro decisions employees make with respect to how they behave in the workplace. These ethics outcomes are as relevant to a financial advice business as to any other that the ECI has been tracking for the past 25 years.

These four major ethics outcomes are:

- Pressure in the workplace to compromise ethical standards.

- Observations of misconduct.

- Reporting misconduct.

- Retaliation perceived by employees after they report misconduct.

Higher-quality ethics programs are linked with strong organisational culture. According to ECI, the single most significant influence on employee conduct is culture; in strong cultures, wrongdoing is significantly reduced.

It is important that companies:

- Hold employees accountable for misconduct.

- Ensure employees trust that leadership will keep their promises and commitments.

- Ensure employees set a good example of ethical workplace behaviour.

As ethical culture strengthens, employee conduct improves: those companies with strong cultures are 467 percent more likely to demonstrate a positive impact on employees. This impact includes employees recognising and adhering to corporate values, feeling prepared to handle key risks and report suspected wrongdoing, and overall, reduced levels of misconduct[1].

Supporting your peers

As demonstrated by the ECI survey, a strong ethics and compliance culture is important to promote positive and ethical decision making. However, despite good intentions, some companies set themselves up for ethical problems by creating environments where people feel compelled to make choices they know, or suspect, are not right. This could be recommending an in-house product when it’s not in a client’s best interests, using a platform to minimise time on administrative tasks although it’s a higher fee load for a client with few assets, or following a licensee’s ‘cookie cutter’ advice model.

This can also result in ‘motivational blindness’, which is defined as the tendency to not notice unethical actions of other people and colleagues when it’s against our own best interests to notice. This is particularly applicable to support staff who might, in some circumstances, consider questioning an approach or decision, but in an advice business where that is not welcomed, are unlikely to speak out.

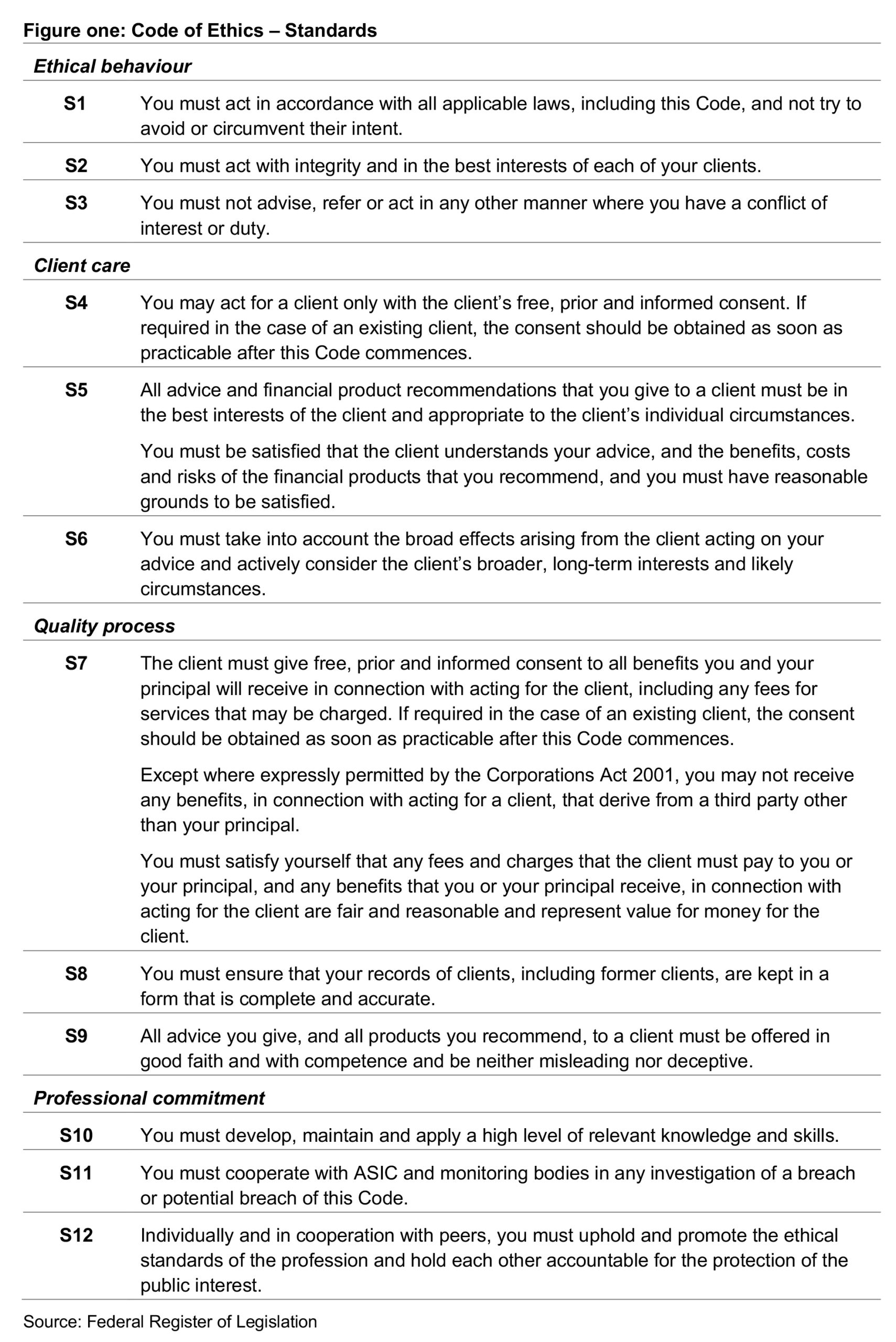

There are five ways companies might unintentionally trigger good people to make unethical choices[2]. Each of these is examined through the lens of the financial adviser Code of Ethics (Code) (figure one) and illustrates how a weak business and ethics culture can lead your peers to actively or passively make decisions that potentially breach, or support a breach, of the Code.

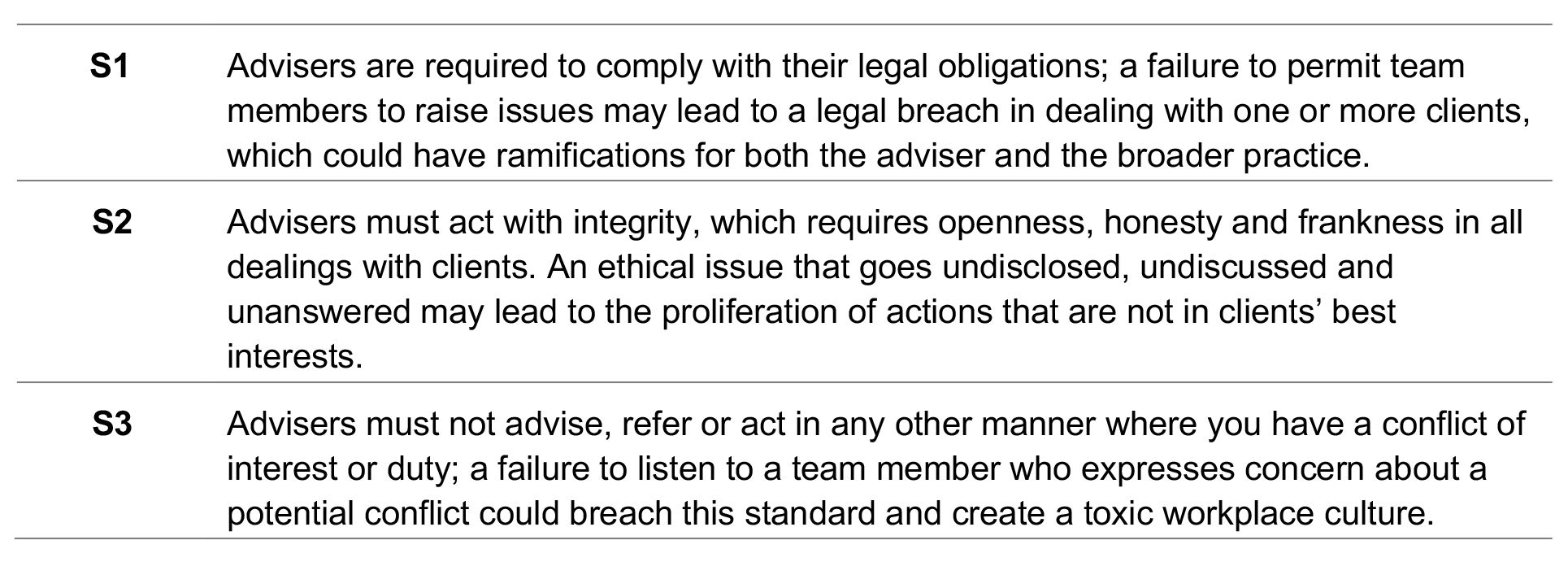

1. Create an environment where it’s psychologically unsafe to speak up

Managers and team leaders need more than an open door policy; they need to encourage their staff to raise and discuss ethical concerns. Creating a culture where your team can speak freely is essential if you’re to avoid misconduct in your practice. Equally important is that those team members are listened to.

Appropriate mechanisms for your team to communicate are crucial, as is an environment in which each team member is comfortable to speak up. Importantly, any issues raised must be addressed; a feeling of futility or a negative reaction to an issue that’s raised does not create a supportive environment and is likely to stultify future discussions.

Failing to provide a safe environment for your team to discuss ethical issues or dilemmas can ultimately have a negative impact on clients and could potentially result in the breach of several standards of the Code of Ethics, including:

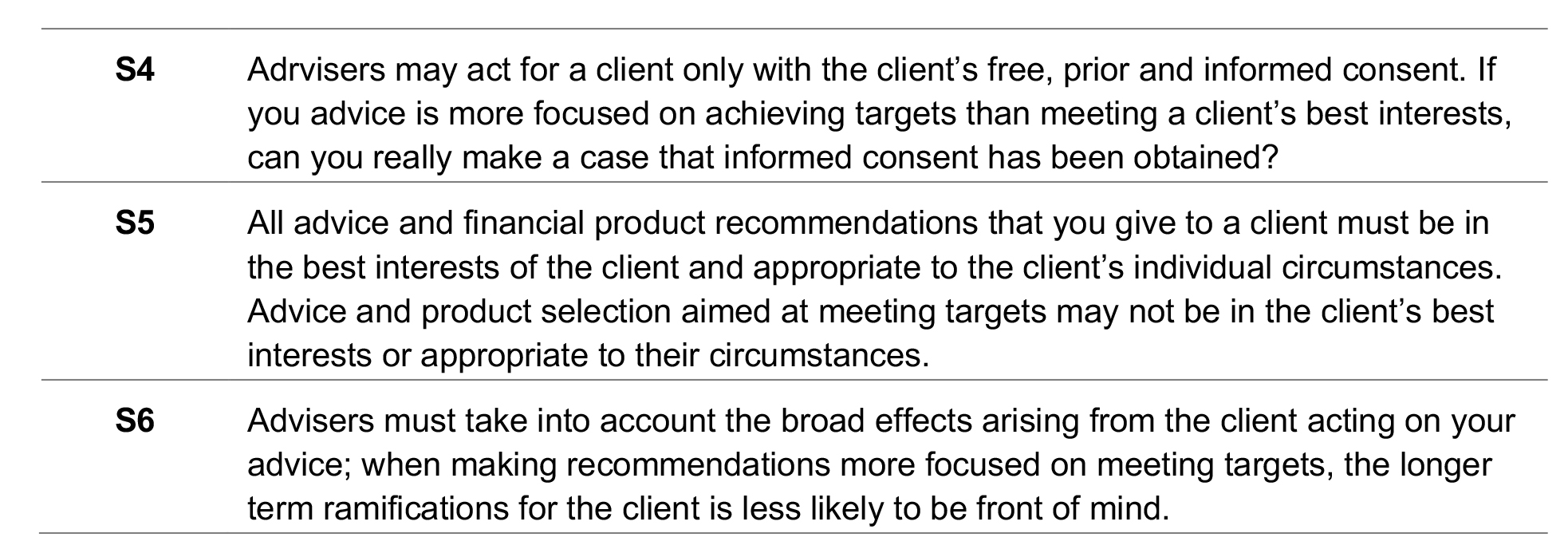

2. Avoid pressure to reach unrealistic performance targets

Performance targets can be financial targets such as profitability or assets under management or focus on client acquisition or retention. Research from Harvard Business School suggests “unfettered goal setting can encourage people to make compromising choices in order to reach targets[2]”.

The standards that comprise the Code of Ethics focus on doing the right thing by clients – obey the law, act in client best interests and act professionally. The 2018 Hayne Royal Commission heard a number of cases in which performance targets may well have influenced actions, such as those to ‘churn’ clients or move them into in-house products or platforms.

While it is common business practice to have a range of performance targets, it’s important that they are both realistic and achievable without having to compromise the advice provided to clients. Targets that are client and service centric can lead to ethical outcomes for those clients.

While striving to reach performance targets can result in breaching several standards of the Code, it’s the ‘Client Care’ standards where it is most likely to cause a breach.

3. Discussing ethics once there’s been a transgression

Too many leaders assume that talking about ethics is something you do once there’s been a client complaint, an obvious transgression or an AFCA investigation. Previous articles in this series have discussed the importance of ethics, business culture and ongoing ethics training in your financial practice. It is not solely a matter of how you behave, but how you and each of your team members conduct business. That’s why it’s important to educate and reaffirm, on a regular basis, the importance of ethical practices in your business.

This is particularly important for considering issues that don’t fall neatly into right and wrong. While the ‘grey zone’ – that area that exists on a continuum between right and wrong – can provide challenges for your business, it can also provide benefits. Being aware of the grey zone and using examples and case studies that aren’t black and white provide an excellent opportunity for training and discussion. List the situations that your team may encounter in their day-to-day work that might not be black and white. Once such situations are identified, you can take a proactive approach with training.

This grey zone reinforces the importance of all employees of a financial planning business being aligned with its values and practices. If you are transparent about how to deal with ethical issues, if you discuss them regularly and not just when there’s an issue, there’s a lower chance of breaching the Code of Ethics and, therefore, less likelihood of facing enforcement action.

This will help maintain professional commitment and uphold standard 12.

4. A positive example isn’t being set

Positive leadership is crucial and all leaders in your business must accept their responsibility in setting that positive example. They must be vigilant about their intentions and also be mindful of how their peers and subordinates might interpret their behaviour.

Leaders must take care with how they react to external and internal factors, as these demonstrate how it’s acceptable to respond. These factors might include:

- a client complaint or negative review on social media

- lower than expected revenue or poor financial performance

- losing a valued staff member to a rival practice

- a change of licensee

- a systems issue or breakdown

- regulatory change or challenge.

Leaders need to model ethical behaviour. In an advice practice, this includes compliance with the standards that comprise the Code of Ethics. Failure to do this not only sets a poor example, it could set the business on problematic path.

In a letter to investors in 2019, veteran investor Warren Buffet made the following comment:

“Over the years, Charlie and I have seen all sorts of bad corporate behaviour, both accounting and operational, induced by the desire of management to meet Wall Street expectations. What starts as an “innocent” fudge in order to not disappoint “the Street” can become the first step toward full-fledged fraud…And if it’s okay for the boss to cheat a little, it’s easy for subordinates to rationalise similar behaviour.”

All leaders need to set a positive example for their team, particularly where an ethical dilemma that arises is not clearly defined.

5. Avoid cultural numbness[3]

Cultural numbness creates a situation that, irrespective of how principled you are, over time, the bearings of your moral compass will shift toward the culture of your organisation. Situations where an ethical leadership is lacking are often those where good people can make poor decisions. Cultural numbness is described as a state where the ‘warning bells have stopped ringing’, where a culture of ethics does not exist, and positive examples are not set by business leaders.

In an advice practice, it could be the difference between acting in your or the practice’s best interests rather than the client’s. It could be skirting legal boundaries (breaching standard one), failing to manage conflicts of interest (breaching standard three) or simply recommending products without taking into account the long-term ramifications of the client acting on your advice (breaching standard six).

The standards that comprise the Code of Ethics are not prescriptive, are not intended to provide definitive guidance. Individual circumstances will differ in practice and there is allowance for differences of professional opinion on how the ethical rules of the profession should apply in a particular case.

This is where positive leadership and an ethics centric business culture will stand an advisory practice in good stead, particularly in those circumstances where you encounter ethical decision making that is not black and white. Doing what is right will depend on the particular circumstances and requires you to exercise your professional judgement in the best interests of each of your clients.

Supporting ethical behaviour in your business

In any profession, most people set out to act ethically. However, as previously noted, ethical practice is not always black and white.

As defined by the Oxford Dictionary, a grey zone is:

“An intermediate area between two opposing positions; a situation, subject, etc., not clearly or easily defined, or not covered by an existing category or set of rules.”

In ethics, this is where right and wrong become blurred and generally requires the application of some form of moral judgement to decide on the appropriate action. And, while most companies have ethics policies that get reviewed and signed annually by all employees, is this enough to ensure ethical behaviour?

Most people are confronted with a wide range of ethical dilemmas on a regular basis. While what’s right is usually clear, the circumstances can impact how each makes decisions about their behaviour and choices. In business, pressure to be successful, competitive and profitable may lead people to confront issues and decisions that are in the grey zone, one in which conflicts of interest can arise and good decision making may become impaired. Good people can end up acting in a questionable manner.

Some of the actions you can take to support business-wide ethical behaviour and maintain a strong ethical business culture, include:

- Establish a practice-wide code of conduct, one which encapsulates your business’s values and the Code of Ethics. Your code of conduct should set clear expectations about your employees’ behaviour when carrying out their duties, including how to deal with difficult issues where a decision could result in a breach of one or more ethical standards. You need to ensure all staff understand each of the twelve standards in the Code of Ethics and how each standard may specifically intersect their role.

- Lead by example, because employees will look to the key individuals in the practice to understand what behaviour is and isn’t acceptable. Senior advisers and personnel will set the tone for ethics in the practice; accordingly, they need to demonstrate your business’s code of conduct in all they say and do.

- Workplace training is a positive way to ensure all staff understand both the practice’s values and the obligations of the Code. The use of case studies to discuss ethical dilemmas can reinforce the practice’s standards of conduct and clarify behaviours and practices that do and don’t work within your code of conduct.

Importantly, ethics training should not be a once off and does not solve a problem. Ideally, training should teach team members to make good decisions that are compliant with the law and consistent with your practice’s values.

This training could be incorporated as part of regular team meeting; as suggested above, by using a variety of case studies which could address common ethical dilemmas across the financial planning industry. The AFCA website[4] is a good source of cases and decisions made by AFCA and its predecessor organisations to form the basis of discussion.

- Ethics should be a key performance indicator (KPI); by reinforcing and potentially rewarding staff for embodying your values, adhering to your practice’s code of conduct and behaving in a way that makes ethical behaviour central to their work will create an ethical practice. Although a values driven KPI can be harder to quantify than one with specific and measurable outcomes, it will highlight to staff the importance of values and ethics to your business.

- Create a feedback loop within your practice. Encourage staff to provide honest feedback about the processes, conversations and client interactions to ensure you are aware of all issues as they arise. Surprises can potentially compromise your business.

Bringing your peers on the ethical journey is important. The licensee and adviser will carry the responsibility of any breach of the Code, but by implementing strategies such as those outlined above can help mitigate the risk of a breaching ethical standards.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or AFCA (or its predecessor organisation). For each, potential breaches of the Code of Ethics are identified. These case studies represent examples of those that would be of value for the business to discuss as part of its workplace training.

Case study one: Inappropriate advice

Will and Debbie are co-directors of the corporate trustee of a self-managed superannuation fund (SMSF) and jointly brought a complaint against their financial adviser, Darren, an authorised representative of ACME Corporation.

The complainants say the advice they received to establish an SMSF, invest in two joint ventures, and enter into associated loan and insurance contracts, was inappropriate. This is because the strategy did not meet their risk tolerance and was too costly, leading to an unnecessarily adverse impact on the SMSF’s balance. Further, they claim they were charged fees for ongoing service they did not receive.

An AFCA investigation found that Darren had failed in the basic elements of providing personal financial advice to Will and Debbie as retail clients. Had he acted in their best interests, the SMSF trustee and SMSF would never have been established.

In addition, the insurance advice was inappropriate; while the income protection (IP) advice was appropriate to Will’s circumstances, the life and total and permanent disability (TPD) recommendations were excessive and left him over- insured.

In all, AFCA found that Darren:

- did not act in the complainants’ best interests

- failed to properly identify objectives, financial situation and needs

- did not conduct a reasonable investigation into suitable financial products

- ignored diversification in his advice

- recommended a strategy which was not in the complainant’s best interests

- did not perform regular reviews but charged for ongoing advice

- falsified some of his file notes.

Further, AFCA found Darren’s conduct fell far short of the industry’s own expectations and the complainants should be compensated as a result. However, their willingness to blindly accept his recommendations contributed to the loss and it is therefore appropriate that the complainants accept some responsibility for the losses they have suffered.

The determination was found partly in favour of the complainants and, as a result, ACME Corporation had to make a range of financial payments to the SMFSF within 14 days of being advised the complainants had accepted the determination. These reparations included sums for investment losses suffered, overpaid insurance premiums and fees changed for no service (plus interest).

Darren potentially breached the following standards of the Code of Ethics:

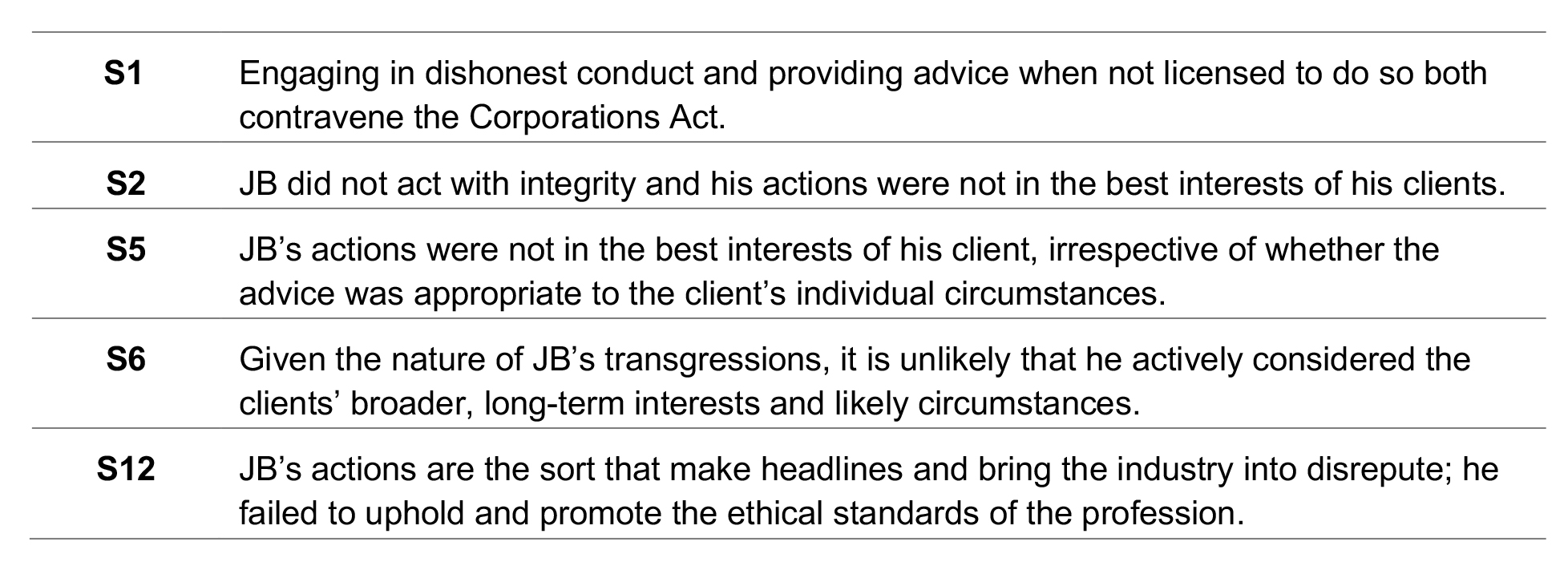

Case study two: Dishonest conduct

Case study two: Dishonest conduct

Adviser JB operated a small financial planning practice on Sydney’s northern beaches. After a client complaint, an ASIC investigation was launched. It found dishonest conduct in relation to a financial product or service.

Following an ASIC investigation into JB and his company, JB Finance Pty Ltd, it is alleged that he obtained $472,890 from 67 clients over a two year period. ASIC alleges the adviser used the funds for his own benefit rather than for investment purposes that had been agreed with his clients. At the time of the offences being committed, ASIC alleges JB was not licensed to provide financial product advice.

Engaging in dishonest conduct in relation to a financial product or financial service in the course of carrying on a financial services business is an offence contrary to section 1041G of the Corporations Act with section 1311.

The matter is still before the courts, however the maximum penalty is 15 years imprisonment or the greater of $945,000 or a fine of three times the total value of the benefits, or both.

JB potentially breached the following standards of the Code of Ethics:

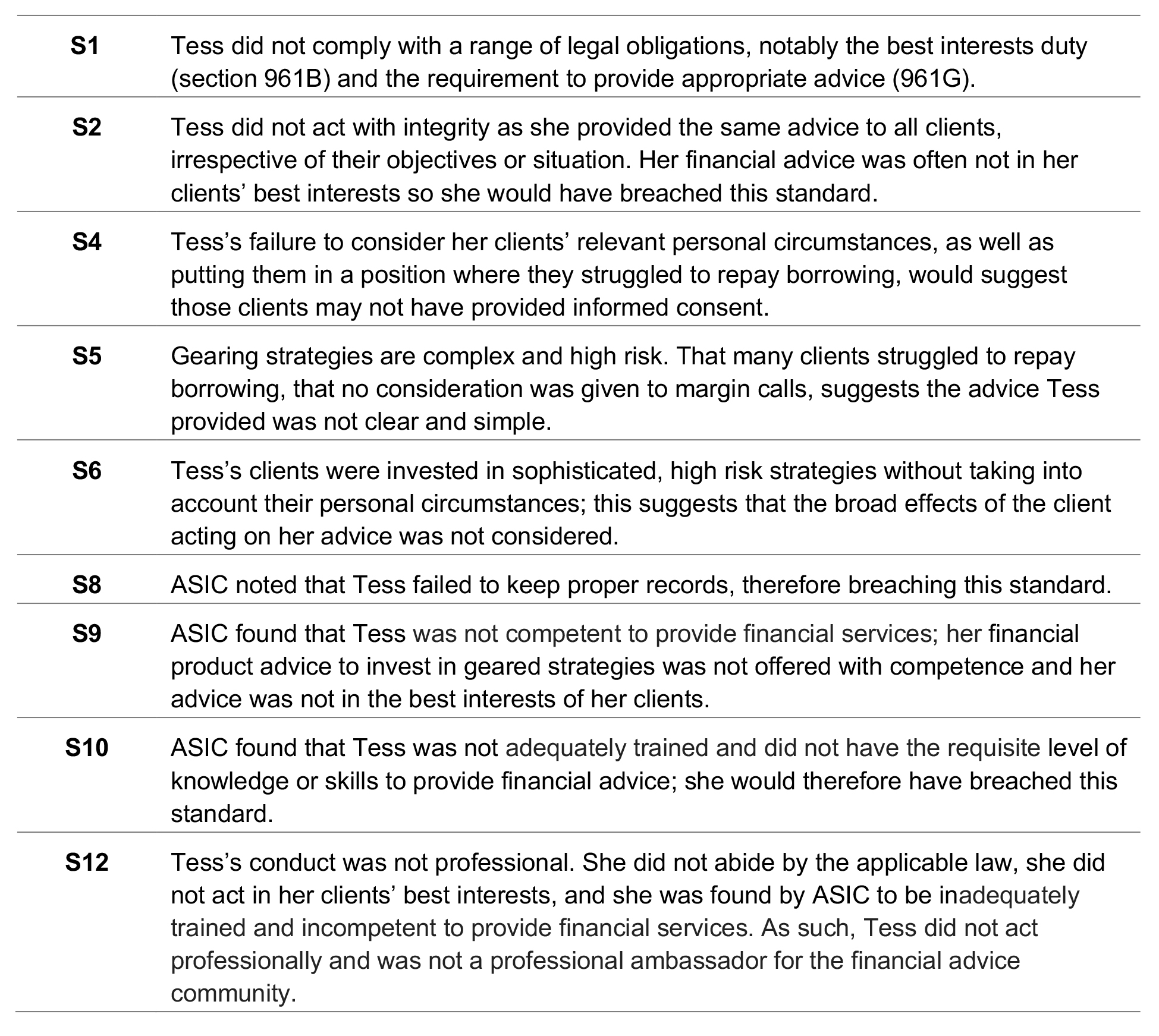

Case study three: Gearing negatively impacts clients

Tess was a sole operator on Queensland’s Gold Coast and an authorised representative of a large national licensee. She had been a financial adviser since 2009 and had worked as an authorised representative of several AFS licensees.

An ASIC review found that Tess failed to act in the best interests of her clients. She provided advice that was inappropriate when her clients’ relevant personal circumstances were reviewed. She repeatedly recommended her clients engage in gearing strategies they did not understand and in many cases, could ill afford. This approach was adopted by Tess across a number of years and licensees.

In providing advice to her clients, ASIC found that Tess failed to consider their relevant personal circumstances, their cash flow or their ability to cover margin calls. She also failed to consider an exit strategy from the gearing arrangements for her clients and did not recommend or implement appropriate personal insurance cover.

Additionally, ASIC found that Tess failed to keep proper records and that she was not adequately trained or competent to provide the financial product advice that formed the basis of her recommendations. Her lack of understanding about her legal and professional obligations as a financial adviser created additional risks to her current and future clients.

Tess received a five year ban from ASIC with respect to providing financial services, carrying on a financial services business or controlling an entity that carries on a financial services business.

Tess’s approach to working with clients would have seen her potentially breach the following standards of the Code:

Ethical values provide the moral compass by which people live their lives, make decisions and react to circumstances. Ethical decision making is important for financial advice practices because the wrong decisions – or decisions which have been implemented badly – can have a significant impact on the financial wellbeing of your clients and their families, as well as the reputation of your business.

Running an ethical business is not only the right thing to do, but it is also good for your business, your staff and your clients. By operating with integrity, transparency and fairness, businesses can build trust with their clients, team and other stakeholders, leading to long-term success and sustainability. While it may require effort and investment, the benefits of running an ethical business far outweigh the costs. Ultimately, by prioritising ethical considerations in decision-making and actions, businesses can demonstrate their commitment to creating a better future for all.

———-