Stephen Miller

With a sparse event calendar this week, the focus of markets will be on the Kansas City Fed’s Jackson Hole Symposium this weekend.

The theme of this year’s conference is Structural Shifts in the Global Economy.

Federal Reserve Chairman Powell is due to speak at around midnight Friday (AEST).

As is always the case, the Federal Reserve (Fed) Chair’s address will be keenly parsed for clues regarding the state of the Fed’s thinking about the economy in general and (given its obvious topicality) in particular, inflation.

It is, of course, always useful to distinguish the structural from the cyclical. However, it may be that both structural and cyclical imperatives are pointing in the same direction when it comes to thinking about where the policy rate and bond yields might travel in the near-term.

The latter part of the (Northern) summer has seen a grind higher in bond yields, led in the main by the longer part of the maturity spectrum.

Cyclical developments argue for “high indefinitely” policy rate

With an eye on recent cyclical developments, the Fed will not regard that upward grind as unwelcome. That reflects a view among key Fed officials that despite the progress on inflation apparent in the consumer price index (CPI) data over the last few months, there is nothing to be gained by declaring “mission accomplished” on inflation. For one thing, the inflation genie might not yet be completely back in the bottle. For another, for the Fed to give credence to such a sentiment might result in a substantial easing in financial conditions occasioned by a sharp decline in bond yields as markets reflect a belief that inflation had been vanquished.

Any reticence to declare victory on inflation is underscored by considerable activity momentum in the economy. The labour market is in good shape and the Atlanta Fed gross domestic product (GDP) ‘nowcast’ is currently running at an eye-popping 5.8 per cent for the current quarter.

For my part, I suspect that progress in getting inflation down may be tracking at a slightly faster pace than embodied in the most recent Fed forecasts published in June. If there were enough Fed officials that come to share that view, then there may be some debate around the advisability of a further policy rate hike at the meeting on 19-20 September. However, even in that circumstance there remains ongoing utility in telegraphing a “high indefinitely” message. In other words, the policy rate is at best at a “plateau” rather than a “peak”.

This is what I suspect will be the tenor of comments from Fed Chair Powell: “that there is some debate around whether further hikes in the policy rate will or will not be needed, but that in any case, given the Fed’s current state of knowledge, the policy rate will stay at around current levels well into 2024 and potentially beyond.”

Such sentiments reflect the Fed’s current tactics given their assessment of where we are in the cycle.

Structural developments potentially point to upside in the ‘neutral’ rate

But what of the theme of the symposium: structural shifts in the economy?

Presumably, among the issues canvassed will be structural shifts in both inflation and interest rates.

I have mentioned a grind higher in bond yields.

That grind higher, against a backdrop of rising bond yields from the pandemic lows, has ignited some discussion around whether there has been some increase in the ‘neutral’ interest rate.

I think it is fair to say that the rates (‘neutral’ and otherwise) that prevailed through the period from the onset of global financial crisis (GFC) through to the end of the pandemic were abnormally low. That was because the US economy took some time to get back to a semblance of ‘normality’ after some 12-15 years of ‘abnormally’ slow growth during an extended convalescence post the GFC and then the pandemic. Certainly, the resilience of activity and the labour market during the current Fed tightening cycle is suggestive of the notion that ‘natural’ real growth rates have increased from that in the preceding 12-15 years and that, accordingly, the ‘neutral’ real interest rate should also have increased.

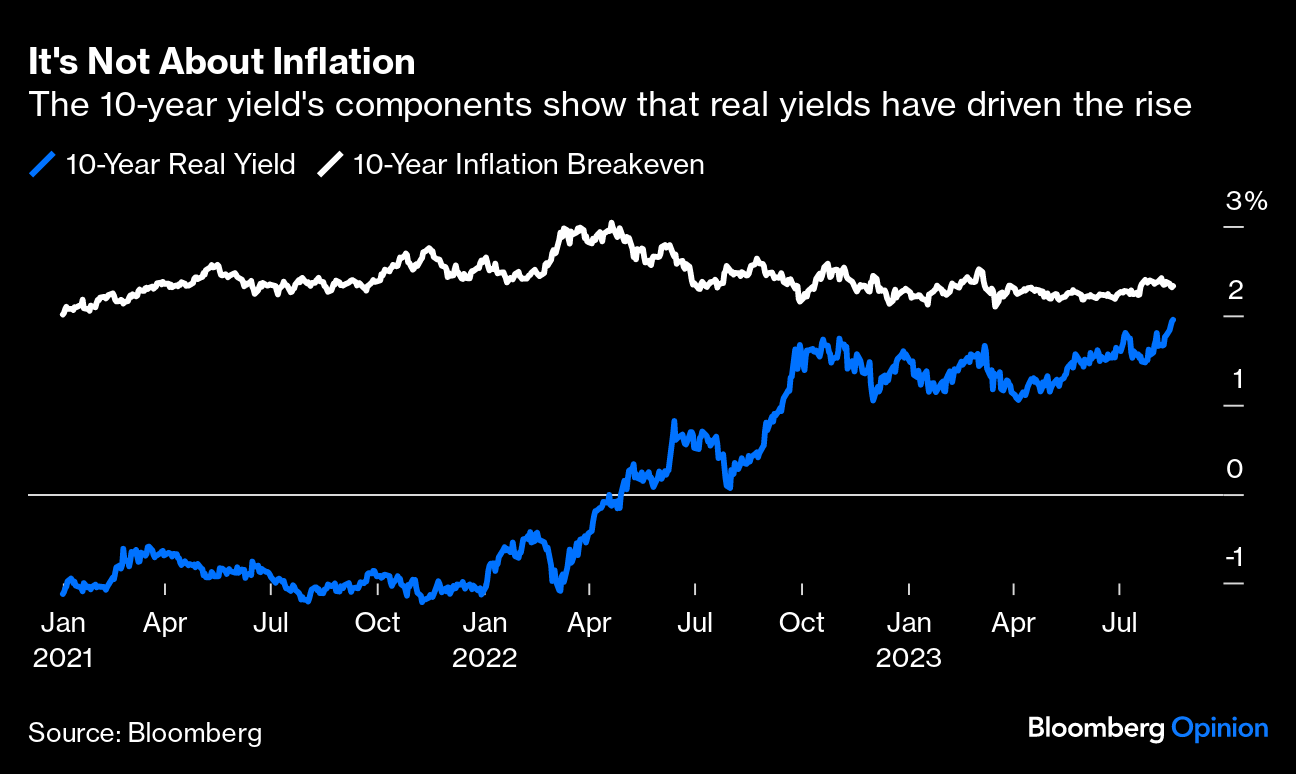

And the increase has largely been in the real interest rate. As this chart from John Authers at Bloomberg shows, if one were to break the US 10-year bond yield into its components of expected inflation (obtained by subtracting the yield on 10-year Treasury Inflation Protected Securities (TIPS) from the 10-year nominal yield), and the real 10-year yield (what’s left over), then inflation expectations have had little to do with it.

Other observers point to other emergent secular trends that might have pushed (and continue to push) the ‘neutral’ real interest rate upwards: larger government deficits; investment demands on the savings pool from clean energy investments; and boomer retirees de-accumulating savings.

But what about inflation? The forgoing would suggest that the Fed has successfully contained inflation pressures and expectations thereof by aggressively increasing the real policy rate.

Anchoring inflation expectations might be challenging

I think some of the reluctance of the Fed to declare “mission accomplished” on inflation has a structural element in addition to the cyclical / tactical considerations outlined above. I have canvassed many times the thesis first put forward by former London School of Economics Professor and Bank of England Monetary Policy Committee member, Charles Goodhart, and his Morgan Stanley colleague, Manoj Pradhan, that the ‘Great Disinflation’ that marked the period from the end of the 1980s until the pandemic is essentially over. In essence their thesis is that there are global structural currents that make elevated developed-country inflation rates more “sticky”. The globalisation of labour supply (after the fall of the Berlin Wall and the “export” of labour from large emerging market economies such as China and India) is abating; globalisation of goods markets is in retreat as governments everywhere introduce protectionist measures under the guise of “industrial policy” and “national champions”; domestic regulation of markets is increasing in scope (leading to upward price pressures); and baby boomer workforce participation is declining (limiting labour supply and lifting wages).

That means to keep inflation and more importantly inflation expectations anchored central banks everywhere will need to maintain higher real policy rates and real bond yields need to stay high, implying current nominal levels may be with us for a time yet. If markets lose faith in the ability of central banks to adequately meet these challenges that might lead to higher inflation premia leading to even higher 10-year bond yields. This is another reason the Fed remains particularly exercised to keep on top of inflation expectations.

These are structural elements that attach to inflation and interest rates that I expect the Fed may well be motivated to illustrate at this Jackson Hole Symposium.

Aside: Bonds again have a place in portfolios

The forgoing notwithstanding, the current level of US bond yields argues for probably a strategic neutral (whatever the benchmark) weighting of bonds in a portfolio.

The above is an argument as to why the current US policy rate and current US bond yields may need to stay around current levels for a time and why upside risks in the form of unanchored inflation expectations exist.

However, with US 2 and 10-year bond yields close to 5.00 per cent and 4.20 per cent respectively it is not a stretch to posit that bonds offer investors a modestly attractive enough yield without the prospect of significant capital losses.

The prevailing level of yields also opens the way for the Fed to respond to a crisis enabling bonds to potentially re-assume their sometime role as a mitigant to risk-averse sentiment.

It has been sometime since bonds were able to deliver these diversifying qualities to portfolios.

By Stephen Miller, investment strategist