The end of the 90 day US tariff reprieve is over for now

Seema Shah

The U.S. administration has decided to delay its self-imposed deadline for implementing reciprocal tariffs until August 1. Reciprocal tariffs, originally announced on April 2, also known as “Liberation Day,” saw U.S. import tariff rates rise significantly for over 50 trade partners before being temporarily lowered to 10% until July 9 to allow for negotiations.

Since then, only a few tentative trade frameworks have been agreed upon, with agreements limited to the U.K. and Vietnam, as well as a truce with China. In an effort to accelerate talks, the administration has begun sending letters to various countries, informing them of their tariff rates if a deal cannot be secured.

The move signalled the administration’s willingness to move forward with significant country-specific punitive tariffs consistent with the initial announcement before the tariff delay. However, as these reciprocal tariffs exclude products subject to sectoral tariffs, they were not as meaningful as initially anticipated. As a result, while Japan and South Korea were hit explicitly with a 25% tariff, only 20% of their trade is exposed to these additional duties.

President Trump also recently announced an additional 50% sectoral tariff on copper. Though the U.S. is highly reliant on imports and the move would likely be counter to rejuvenating domestic manufacturing, the experience with Steel and Aluminium tariffs, where exclusions were not only revoked and derivative products included, but also increased to 50% from 25%, is a possible signal of the administration’s determination on sectoral tariffs.

Market reaction

Despite all the tariff upheaval of the past few months, equity markets have hit new all-time highs and credit spreads are close to historic tights. This likely reflects the widespread view that the administration has been willing to soften its stance multiple times to prevent a lasting market sell-off. Moreover, with Trump’s tariffs having a limited macro impact so far, markets may also be looking through trade policy and instead focusing on factors that can change economic fundamentals, such as corporate earnings.

The new status quo

Despite President Trump’s comments that there will be no further extension after August 1, that is likely not the end of the story. Trade deals typically take between 18 months to three years to finalise, making deadline extensions and renewed tensions still possible. Ongoing legal challenges also have the potential to limit the staying power of broad-based tariffs. Finally, the administration’s liberal use of tariffs as a negotiating tool to extract non-economic concessions means that tariff noise will likely remain a permanent feature of the economic backdrop.

Even through all the tariff noise, negotiations, legal challenges, and trade spats, we can be certain of three factors:

- Tariffs are here to stay. The administration views tariffs as a key source of tax revenue to fund its fiscal expansion plans—tariffs are unlikely to disappear entirely.

- Peak tariffs are behind us, particularly for China. A return to a 145% tariff on China’s imports would result in a trade embargo between the two nations, sharply raising U.S. recession odds again, making it politically unfeasible.

- An increased focus on sectoral tariffs. As the administration prioritises reshaping global manufacturing toward the U.S. domestic industrial base, it will likely increasingly pivot to sectoral tariffs. While sectoral tariffs generally take longer to implement, they carry less legal ambiguity than other trade mechanisms, suggesting they have longer staying power.

With these three factors in mind, our baseline expectations include:

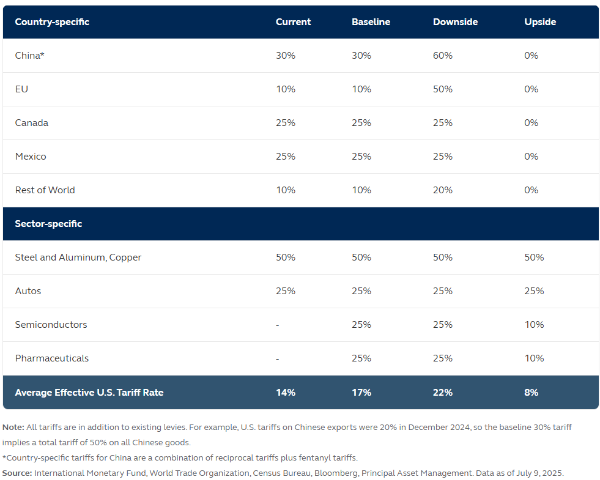

- Global reciprocal tariffs maintained at 10% on average.

- Country-specific universal tariffs on the following countries maintained near current levels: EU 10%, China 30%, Mexico 25%, and Canada 25%.

- Current exemptions (i.e., United States-Mexico-Canada Agreement (USCMA) and energy) maintained

- Sectoral tariffs broadened to include 25% duties on semiconductors and pharmaceuticals, while 50% duties on steel and aluminum are expanded to copper. The 25% duty on autos is maintained.

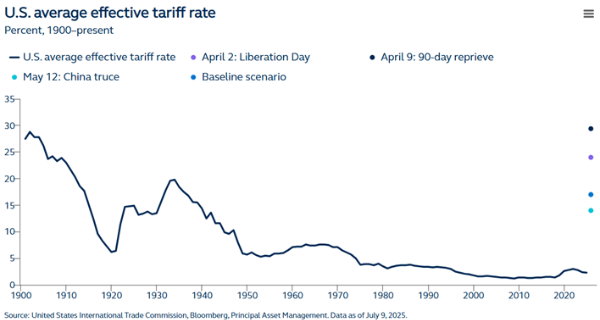

These baseline expectations imply that the average effective U.S. tariff rate will ultimately settle at around 17%, the highest level since the 1930s Smoot-Hawley tariffs, up from the current 14% and meaningfully higher than the 2% at the start of 2025.

Macro effects of the U.S. tariff baseline scenario

U.S. impact

The overall impact would result in a 1.7% drag on annual U.S. GDP growth over the next few years. It is important, however, to note that there is significant variability around this estimate. While we assume that substitution effects—which see some tariffed goods trade flows replaced by domestic sources—could mitigate some of the adverse effects, other factors, such as behavioral or preference changes and currency movements, could also increase or reduce the growth impact of tariffs.

This scenario also results in a one-off tariff-induced boost to inflation of 1.6%, likely bringing core inflation up to 3.5% by year-end. While unlikely to lead to a persistent inflationary impulse, the Federal Reserve is rightly concerned that the impact could further fuel inflation expectations, especially as overall price stability remains elusive.

Although the overall impact is not as severe as seemed likely a few months ago, tariffs will remain a sizable headwind to the U.S. economy over the next few years.

Global impact

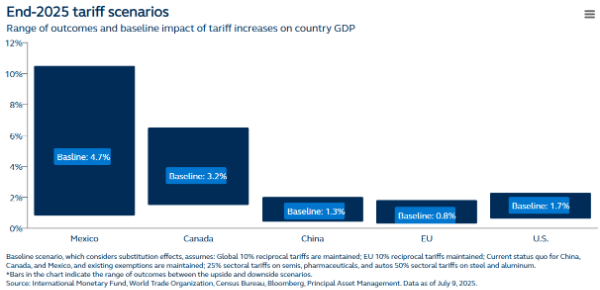

The subsequent decrease in export volumes and tariff retaliation for impacted economies would also create a negative growth impact outside the U.S., albeit the range of outcomes is broad. Countries most dependent on the U.S. for trade are like to see the largest impact: punishing Mexico and Canada while being milder for China and the EU.

Additional levies on China in our baseline scenario are limited because current tariff levels already imply an almost 50% decline in imports from China as U.S. demand shifts to other lower-priced alternatives or is destroyed altogether. Meanwhile, the overall tariff impact on the EU could be quite punitive when sectoral levies are taken into account. Indeed, tariffs on pharmaceuticals, which account for nearly 30% of the EU’s exports to the U.S., would have a meaningful negative impact on growth.

However, it is also worth noting that Mexico and Canada would be relative beneficiaries in our baseline scenario, as the existing USMCA framework is likely to persist going forward, given deeply the integrated supply chains between the U.S., Mexico, and Canada.

Alternate tariff scenarios

As noted, with trade negotiations still ongoing and Trump emboldened by the success of tariffs as a negotiating tool to extract non-economic concessions, trade policy is likely to remain highly fluid from here. With many possible paths toward an endgame, we outline downside and upside scenarios as the potential range of outcomes for trade policy.

The downside scenario is likely triggered by renewed hostilities, which also lead to retaliation by trade partners, and the average effective U.S. tariff rate could increase to 24%. Yet, the administration is likely to steer clear of outright freezing international trade flows, so even in this downside scenario, it’s unlikely that tariffs surpass levels seen around Liberation Day, particularly the 145% tariff rate implemented on China in mid-April. The resulting drag on U.S. GDP would climb to over 2% while the inflation impact would also total more than 2%, pushing inflation further above the Fed’s 2% target.

In contrast, the U.S. administration’s ability to successfully extract significant concessions from trade partners, including massive purchase guarantees or investment commitments, could see a significant tariff de-escalation. In this upside scenario, average effective tariffs would fall to 8% from the current level of 14%. The resulting drag on U.S. GDP would be worth just 0.6%, with an equally moderate inflation increase.

Investment outlook

While the extension of negotiations through August 1 may suggest that more trade deals will materialise, investors should expect trade barriers to remain higher for the foreseeable future, suggesting there is likely to be some economic scarring. In the near term, risk-on sentiment may need to contend with an economic outlook of slowing growth, elevated inflation, and ongoing policy uncertainty. Indeed, even in an optimistic upside scenario where trade hostilities dissipate, the average effective tariff rate is still expected to triple compared to its level at the start of the year. Beyond the short term, it is worth remembering that market disruptions from policy uncertainty are typically short-lived if companies continue to deliver earnings. In turn, investors should expect continued gains in the S&P 500 if corporate earnings continue to grow.

With trade policy volatility likely to persist, it could create headwinds for the U.S. dollar, keeping it vulnerable to further downward adjustment. Yet it’s important to point out that a sharp downward spiral is unlikely. The dollar’s safe haven status remains secure for now, as over half of global trade is invoiced in dollars, and the depth and liquidity of U.S. capital markets remain unmatched.

For investors, diversification across geographies and sectors will be critical. A weakening dollar could further reinforce the case for continued international exposure, particularly as more active policymaking in other global economies invigorates growth momentum. As with any shock, trade policy volatility should create winners and losers amid increased sector bifurcation, with active management playing a key role in identifying opportunities.

Overall, despite the narrow range of outcomes with respect to trade policy, investors should not be complacent about risks stemming from abroad and the restructuring of global trade, both in the near term and the longer term.

By Seema Shah, Chief Global Strategist at Principal Asset Management