Insurance and business succession planning

For the smooth and orderly handover of a business from one owner to another, a Business Succession Plan is essential.

A Business Succession Plan is a strategy for the smooth and orderly handover of a business from one owner/manager to another in particular circumstances, such as the planned or unplanned departure of one partner from the business.

This article from Zurich examines the importance of both a sound succession plan and having the appropriate insurance policies in place to protect all parties.

What is Business Succession Planning?

A Business Succession Plan can be simply described as a strategy for the smooth and orderly handover of a business from one owner/manager to another in particular circumstances, such as the planned or unplanned departure of one partner from the business. A plan minimises disruption and avoids the necessity for additional borrowing or asset depletion in what may be already adverse circumstances.

At some time, an owner of a businesses will either want to, or be forced to, withdraw from the business. In such circumstances most owners want the business to continue. They will also want any benefits that might arise from their departure or disposal of the business to flow to themselves and their families.

Owners who willingly decide to withdraw from the business can choose their own time to do so and the mechanism for withdrawal. Owners who are forced to withdraw from the business because of ill health will usually have fewer options about how and when they withdraw. If the death of an owner occurs, the problem of what to do with the business is shifted to the family or the estate of the deceased. Where business partners are involved the situation can become even me complicated.

Unfortunately, far too many family businesses are ill-prepared to execute a succession plan. According to Deloitte[1], 64% of next generation leaders will assume control of their family business without a formal succession plan.

“Many of the world’s most successful businesses are run by multigenerational families. But while over 70% of Australian businesses are family run, only 30% survive the transition from first to second generation and just 12% making it to the third generation.”

Source: SmartCompany

The financial adviser’s role in succession planning

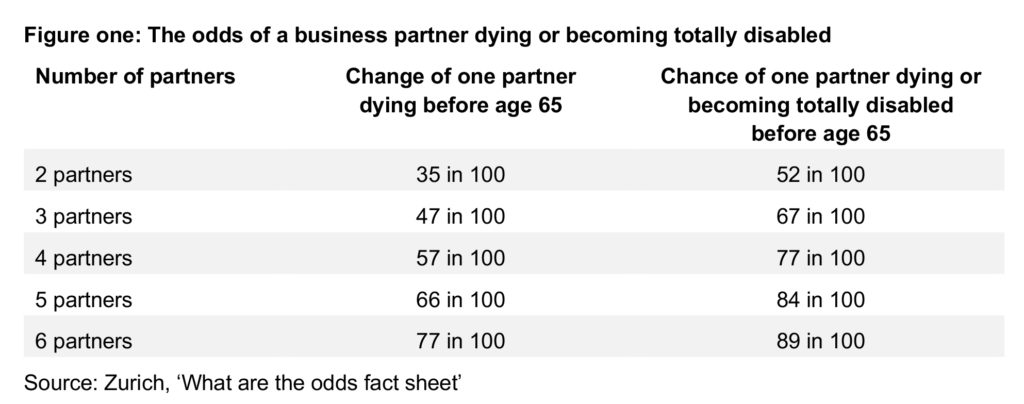

A financial adviser is ideally placed to initiate and support an effective Business Succession Plan. You may find clients are resistant to the idea; after all, many Australians ascribe to the ‘she’ll be right mate’ philosophy and, as a result, tend to be underinsured. Some sobering statistics (figure one) might help argue that succession planning is imperative for all businesses.

The first stage in any Business Succession Plan is to identify the client’s objectives and needs. These may include:

- Identifying issues of management and ownership succession well before retirement

- Developing appropriate structures for the selection and development of successors

- Devising strategies to ensure continuity of the business during ownership transition

- Maintaining business value.

Without a Business Succession Plan, a business may fail in the face of a tragic event. As well as the affected owner, the remaining owners can lose their business and livelihood.

The implementation of a Business Succession Plan often requires the assistance of other advisers, including specialist lawyers and the business’s accountant. Accountants are generally trained to value the business and have specialist knowledge regarding the ownership structure of the business. Specialist lawyers are trained to attend to reviewing the proposed strategy and advising of the tax issues and preparing the documentation. The financial adviser is in the best position to identify the risks to the business and will also have oversight of the client’s estate plan.

What is the value of a succession plan?

Business owners need to understand the value of a success plan and the importance of detailed exit strategies that plan for when and how to leave their business in the event of a voluntary or sudden involuntary departure due to ill health or death.

There are numerous benefits from implementing a Business Succession Plan, including:

For the remaining owners

- Eliminates claims to management rights of the business by the estate of departing owners

- Prevents unwanted introduction of new owners with incompatible philosophies and agendas

- Protects against control of the business being ‘frozen’ because of probate difficulties or legal restrictions if an owner loses legal capacity

- Provides assurance of the opportunity to buy shares from an affected owner should they suffer a tragic event

- Predetermines funding for the purchase, as well as the price of the business

- Assures continuity of the business with minimal disruption

- Provides security for suppliers, staff, creditors and other stakeholders.

For the outgoing owner or their estate

- Removes pressure to remain involved in the business

- Assures purchasers will buy the business

- Provides fair price for the business interest

- Reduces delay between suffering a tragic event and receiving funds.

For the adviser

- You can gain a locked in and loyal client

- It’s harder for competitors to take over your client

- Increases your professionalism

- Protects your client base for the long term.

The importance of a Business Succession Plan

Some events, if not planned for, can destroy a business and possibly the livelihood of the proprietors and their families. Specific problems that may occur include:

- The estate/family of the departed proprietor may demand involvement in the business with the existing shareholders or partners.

- The estate/family may make unrealistic demands on the value of their equity or may want the business wound up and the proceeds distributed.

- Creditors may call in outstanding amounts, particularly where the departed proprietor had a significant impact on the perceived creditworthiness of the business.

- Lending institutions may limit the continuing availability of finance if they perceive the business’s financial capacity has diminished.

- The departed proprietor’s estate/family may be placed in the position of accepting less than the business is worth.

- Clients and customers may take their business elsewhere if they perceive a reduction in the ability of the business to service their needs.

Case study one – Business Succession Plan

David and Alberto ran a chain of butcher shops and employed 24 full-time staff. The business was in its tenth year of operation and both partners were beginning to see the fruits of their labour.

The business was very successful and in a profitable position. Just when everything was going perfectly, tragedy struck. David, after complaining of back pain, finally decided to visit his GP. After some tests, he was sent to a specialist and diagnosed with cancer.

David immediately stopped working to undergo treatment. Unfortunately after three months, the treatment was unsuccessful. The diagnosis was just too late. David left all of his assets to his wife Lisa. This included his interest in the business.

Lisa had never been involved with the business and now wasn’t the time to start. She was very conscious of the fact that David and Alberto weren’t just business partners, but also good friends. However Lisa needed to convert her half ownership into usable funds; she had relied on David’s wage and she needed money to support herself and her three children.

Alberto would have been happy to pay Lisa her share of the value of the business if:

- He knew what the business was worth

- Lisa agreed with the value

- Alberto could find the money to pay her

David and Alberto – with their adviser, accountant and tax lawyer – could have prepared a Business Succession Plan to deal with a principal dying, becoming disabled, retiring or resigning. Lisa could have then expected Alberto to purchase her share of the business for an agreed predetermined price. Alberto could have required Lisa to sell her share of the business to him for the predetermined price. This would have been in the best interests of both parties.

The need for a formal buy/sell agreement

Any agreement, whether oral or written, can be binding on all parties.

However:

- It may be difficult to prove an enforceable oral agreement exists if a tragic event occurs, such as the death of one of the parties

- A letter of intent may also be insufficient when a tragic event occurs, given the complicated concepts that underpin a buy/sell agreement.

A Business Succession Plan deals with the difficult issues involved in the writing of insurance, the tax implications and the knowledge of the business structures. The majority of banks’ fine-print clauses on security for a business loan, the death or disability of a guarantor or co-surety to a business is an ‘event of default’. This means that if any person who is a party to a bank’s security dies, becomes disabled or suffers a traumatic event, the bank is able to and could seek repayment or to renegotiate the loan facility.

The prudent solution here is to have business debt protection in place, so in the event a business owner (or principal) dies, proceeds can be used to pay off any outstanding debts. This is a form of ‘key person insurance’ (as distinct from insurance for a Business Succession Plan).

How is a buy/sell agreement funded?

Even with a Business Succession Plan to ensure the transfer of a business interest upon death, all problems are not solved. Where do the remaining owners get the money to buy out the deceased’s family’s interest?

A number of funding mechanisms are available. The most successful is a combination of:

- Life insurance

- Total and Permanent Disability (TPD) cover

- Trauma insurance

The use of insurance as a funding source for the buy-out provides greater certainty for all parties. With the right policies in place, and as long as the premiums are paid, all parties know where the funds for a buy-out will come from.

A fair value clause should, however, be included in any agreement as a ‘backup’ to the previous two valuation methods. This clause is only invoked should the parties be unable to agree upon the value of the business when applying those methods. Disagreement may be either during a yearly valuation or upon a trigger event occurring.

Insurance and financial underwriting

To facilitate financial underwriting of any insurance for business succession it is important to understand and be clear on:

- The purpose of the cover

- Who is to own the policy (and effectively have the insurable interest)

- Who owns the business?

- What are the roles and duties of the owners in the business?

- Does it make sense and sound reasonable?

The answers to these questions will determine the financial and/or business requirements (as shown in figure two). If the insurable interest is held by the client who is also the policy owner and 100% business owner it may be considered as personal cover for financial underwriting purposes.

Key person insurance

Key person insurance is designed to protect a business in the event of the loss of a person who makes a significant contribution towards the profitability and stability of the business. Key people are the people who provide the ideas, drive, initiative and skills which, in turn, generate the profits needed for the survival and growth of the business.

The sudden loss of a key person, for any reason, can have an adverse effect on the business. Finding a suitable replacement may take considerable time and money. In the meantime the profitability and value of the business may decline, while costs remain. In addition, the loss of a key person can have a negative impact on goodwill and even the credit rating of the business.

Essentially, key person insurance protects the business while business succession planning protects the owners. Key person insurance addresses the potential loss of business expertise – business succession planning addresses issues to do with the change of ownership of the business.

Despite the differences, the objective of key person insurance is the same as business succession planning; that is, to ensure a business remains healthy despite the loss of one of its key people.

Types of key person insurance

There are two types of key person insurance depending on the intended purpose.

Revenue purpose key person insurance is used to:

- Cover the cost of replacing the income loss resulting from the death or trauma suffered by the key person.

- Compensate the equity owners in the business for the loss of profits they would otherwise suffer due to the effect of the loss of the key person’s efforts.

Capital purpose key person insurance is used to replace capital losses suffered by the business as the result of the death or trauma suffered by a key person. For example to:

- Repay all or part of any debt owed by the business to secured creditors (e.g. banks) or equity participants

- Provide release of guarantee by creditors holding the benefit of personal guarantees.

- Provide discharges of security over a guarantor’s property.

Each type of key person insurance provides a different outcome and attracts different tax and legal considerations.

Types of key person insurance cover can include:

- Life insurance

- Total and Permanent Disability insurance

- Trauma insurance.

Note that it is the business that owns the policies, pays the premiums and is the beneficiary of insurance payouts.

Business debt or guarantor protection

Banks generally insist on small to medium business owners personally guaranteeing the borrowings of the business. Where there is more than one business owner this is referred to as “joint and several liability”.

Business debt or guarantor protection is a further form of business insurance. It closely resembles key person insurance, as it protects the financial health of the business itself as well as that of the owners.

Business debt protection can cover any type of commercial debt the business has, including commercial loans or mortgages, an overdraft or director’s loans. Often a business owner will secure loans to the business with their personal assets, for example, the family home. Only when the loan is repaid in full is the guarantee extinguished.

Business debt protection ensures that upon the death, traumatic illness or total and permanent disablement of a business owner providing a guarantee for a loan, the loan can still be repaid in full.

This not only benefits the business owner(s) but also the guarantor(s) and their estate as it protects their personal assets.

It is common for two or more business owners to have entered into what is known as joint or several guarantees for a loan. This means that all guarantors are liable for the loan regardless of their share of the business or which of the owners took out the loan.

Therefore, a tragic event could entail personal hardship not only for the owner who has died or suffered a traumatic illness, but for the surviving owners as well. It could also place a financial burden on the business and have a negative impact on the business’s capacity to continue.

Estate equalisation

Estate equalisation is about creating wealth to offset assets which are not easily divided in the case of the death of the owner.

Where an asset such as a business is not easily divisible, making provision for beneficiaries to receive a payment equal to the value of their share by other means may need to be considered.

There are a number of reasons why an asset such as a business creates difficulties in its division and distribution upon the death of the owner. These include the following:

- A business cannot usually be easily broken-up.

- It may not be commercially viable for the business if all beneficiaries were to receive a part of it.

- Continuing the business may not interest all or any of the beneficiaries.

- It may be difficult to convert the business into cash.

- A Capital Gains Tax liability may arise if, after receiving the asset, the beneficiary disposes of it.

- Even though the beneficiaries may be interested in continuing to operate the business, they may not have the knowledge and skills to do so.

Estate equalisation can apply to any structure or size of business where you identify a need for your client to balance the interests of beneficiaries in the event of their death. Once the need to provide some form of payment to beneficiaries in lieu of the business itself has been recognised, the question of where the fund will come from arises.

Funding can come from one of several sources, such as cash on hand, readily convertible assets or a life insurance policy.

As with a buy/sell arrangement with partnership buyouts, there is a need to put a legal agreement in place (in this case a Will), and funding arrangements (either available cash or insurance) for this agreement to be workable.

Disposing of property by means of a Will

It is important to note that the only assets a person can dispose of with a Will are assets owned by them. Assets owned by a company or a trust cannot be disposed of by a Will. In relation to a company, a shareholder can only dispose of their shares in the company by means of a Will. In the case of a trust, the trustee has, within limits, the legal ability to dispose of the assets.

In addition, ownership of assets as “joint tenants” means that even in the of the death of one of the owners, their share automatically goes to the surviving owner or owners.

Case study – Estate equalisation

Greta has run a successful dairy farm since the death of her husband and business partner at the age of 45 years in a farm accident.

The principal assets are the land, family home, other buildings on the property, machinery and livestock.

Greta has three children, but only one of them, Simon, wishes to live and work on the farm. Greta wants to ensure that all her children receive their fair share of the inheritance when she eventually dies. How can she deal with this dilemma?

The alternatives

Greta could:

- Leave the farm to the three children, equally.

- Leave the farm to Simon but require that he buy out the other two children.

Both of these alternatives are unsatisfactory in this situation.

The solution

Greta could take out one or more life policies. On her death there will be sufficient money to provide funds to the two children who are not interested in running the farm, while the farm itself can be left to Simon, unencumbered by debt.

Business requirements

For the smooth and orderly handover of a business from one owner to another, a Business Succession Plan is essential. A plan minimises disruption and avoids the necessity for additional borrowing or asset depletion in what already may be adverse circumstances. It ensures the wishes of all parties are met and that no one suffers adverse financial consequences resulting from the changed circumstances.

[1] https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Strategy/gx-family-business-nextgen-survey.pdf

![]()