Message understood? Key considerations and steps when providing financial advice to vulnerable clients

The nature of the client/adviser relationship means advisers may be uniquely placed to provide advice which acts as the ultimate protection for vulnerable clients.

Introduction

Amidst an overall increased media and regulator focus on financial consumer protection, especially post the Hayne Royal Commission, the spotlight on ‘vulnerable’ financial consumers has become especially intense.

Our population is ageing and becoming more culturally diverse at a time when financial products remain as complex as ever, and as we stand on the cusp of the largest intergenerational wealth transfer ever witnessed.

Throw in a pandemic which has left thousands isolated, out of work and even seen a rush back to the parental home, and the number of people who are contextually, or situationally, vulnerable to financial harm has never been bigger.

The enormity of this issue has not been lost on ASIC, who have made the protection of vulnerable financial consumers a specific focus in their current Corporate Plan[1].

Nor should it be lost on financial advisers.

There are a number of reasons why protecting vulnerable consumers is very much a ‘live’ issue for Australian financial advisers:

- advisers’ existing obligations around best interests and informed consent may be more challenging to fulfil when dealing with vulnerable clients

- the nature of the adviser/client relationship puts them in a unique position to identify when consumers are at risk of financial harm from other parties, and

- advisers will need to adopt and comply with any new consumer protection regulations introduced in the future.

The protection of vulnerable customers has implications for every aspect of the advice value chain, including compliance, complaints handling, and client engagement and communication. As such, it is an issue which should be high on the list of risk management priorities for both AFSLs and individual advisers.

Who are vulnerable financial consumers?

While there is no regulated definition of vulnerable financial consumers, there is general agreement that it encompasses those who are at heightened risk of suffering adverse consequences when interacting with financial products and services, because of:

- personal, social, and cultural factors

- age (very old or very young)

- poor physical and/or mental health

- cognitive impairment

- cultural attitudes to money

- remote living

- lack of family support

- speaking a language other than English, and

- situational/temporary factors

- loss of employment

- illness or injury

- relationship breakdown

- domestic violence

- death of a loved one.

What does financial harm look like?

Whilst we see vulnerable customers suffer adverse consequences across all financial product types, in recent times, regulators have focused their particular attention on a handful of areas including credit products, investment scams, elder abuse and financial control, and the mis-selling of financial products.

Credit products

From unsolicited credit card upgrades to personal loans made to people with no capacity to repay, the stories of truly vulnerable customers being saddled with crippling debts are – sadly – too many to mention. These stories were the catalyst for the 2009 introduction of Responsible Lending laws, a consumer protection designed to put more responsibility on lenders to establish creditworthiness. (Their potential repeal, in a bid to free up the flow of credit during the pandemic, remains the subject of intense current debate[2].)

More recent developments in the credit market, such as payday loans, and wage advance apps (such as MyPay Now) are coming under increased scrutiny for their high interest costs and the fact that they are currently unregulated.

And the buy now, pay later industry, despite introducing its own code of conduct in March 2021[3], continues to be at the centre of calls for it to be regulated in the same way as other credit products, with research showing around 1 in 5 users have missed payments[4].

Investment scams

The dark side of the digitalisation of our lives is that it easy for the wool to be pulled over our eyes, whether it be a dating scam preying on those vulnerable through their loneliness, or TikTok finfluencers spruiking the ‘next big thing’ in investing. Indeed, the number of investment scams reported during the COVID-19 pandemic has increased dramatically since pre-pandemic.

In one of its regular updates, ASIC reported that in early 2021 it received almost 10 times the amount of misconduct reports compared to the pre-pandemic average (75% of which related to crypto-asset scams)[5].

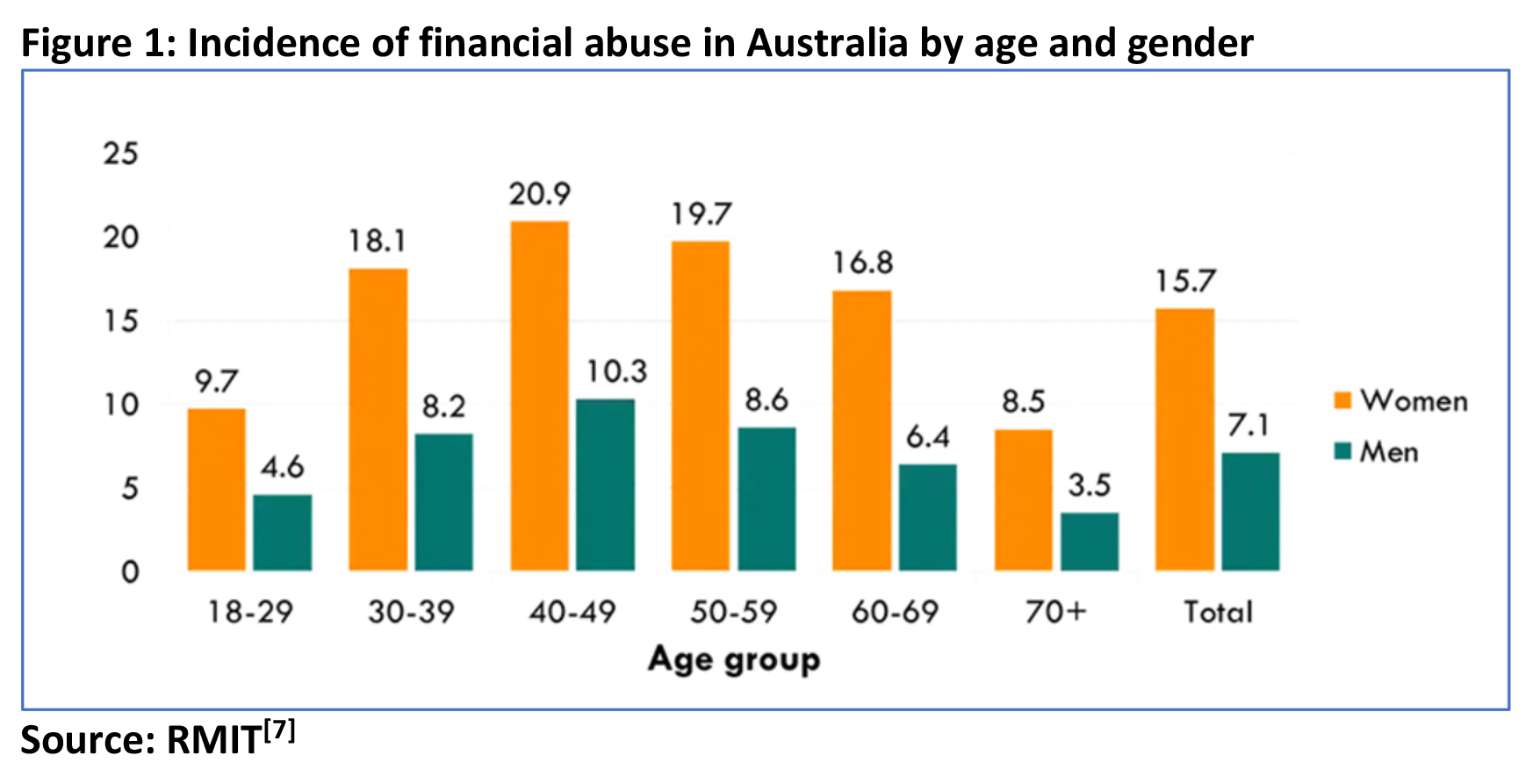

Financial abuse

Financial (or economic) abuse occurs when someone takes away another person’s access to money, manipulates their financial decisions, or uses their money without consent. It is now recognised as a form of family violence in law in Victoria, South Australia, Tasmania, and the Northern Territory. Abusers can be partners, siblings, parents, children and friends. (Perhaps even more alarmingly, financial abuse can be facilitated, or even perpetrated, by financial service providers.)

According to RMIT University About 16 per cent of Australian women and 7 per cent of men will experience some form of financial abuse in their lifetime[6].

Financial abuse can take many forms, but according to White Ribbon Australia[8], common warning signs that a person may be financial abusing their partner include:

- controlling all of the household spending

- refusing to include their partner in financial decisions

- the withholding of money

- forbidding their partner to work

- monitoring what their partner spends

- taking out a loan in their partner’s name.

Elder abuse

The elderly are particularly susceptible to financial abuse, becoming more vulnerable due to their increasing frailty, increasing dependency and diminished capacity.

In many cases the abuser is a family member or carer, whose illegal or improper use of an older person’s funds or resources might include:

- mismanagement of their funds or investments

- pressuring relatives for early inheritances

- pressuring the older person to accept lower-cost aged care or forego medical treatments in order to preserve an inheritance

- living with the older person and refusing to contribute money for expenses

- forging or forcing an older person’s signature

- persuading the older person to change the terms of an existing contract, the clauses in a Will or a POA through deception or undue influence

- convincing the older person to sign over the title/s of property they own or to sell their properties below true market value.

Evidence suggests financial elder abuse has increased during the pandemic, as people losing their jobs are forced to move back in with their parents, or their adult children.

Although there are countless examples, the potential for such abuse is powerfully summed up in a recent NSW Civil and Administrative Tribunal case[9], where a NSW woman is alleged to have paid her mother-in-law $3 for three vacant blocks of Sydney land worth more than $3 million!

Product mis-selling

Whilst mis-selling of financial products to vulnerable customers has been widespread across many categories, it has been particularly common in the insurance sector, with high profile examples including:

- selling of funeral insurance plans to indigenous communities, vulnerable because of their language and literacy skills

- marketing of funeral insurance to poorer, emotionally vulnerable elderly Australians, and

- selling of add-on insurance and credit card insurance to customers who felt obligated to take out an insurance product as gratitude for having their credit application accepted.

ASIC have made mis-selling of add on and credit insurance a particular focus, estimating that over the years, around 450,000 credit insurance customers and 245,000 add on insurance customers were essentially sold products with ‘little or no value’[10].

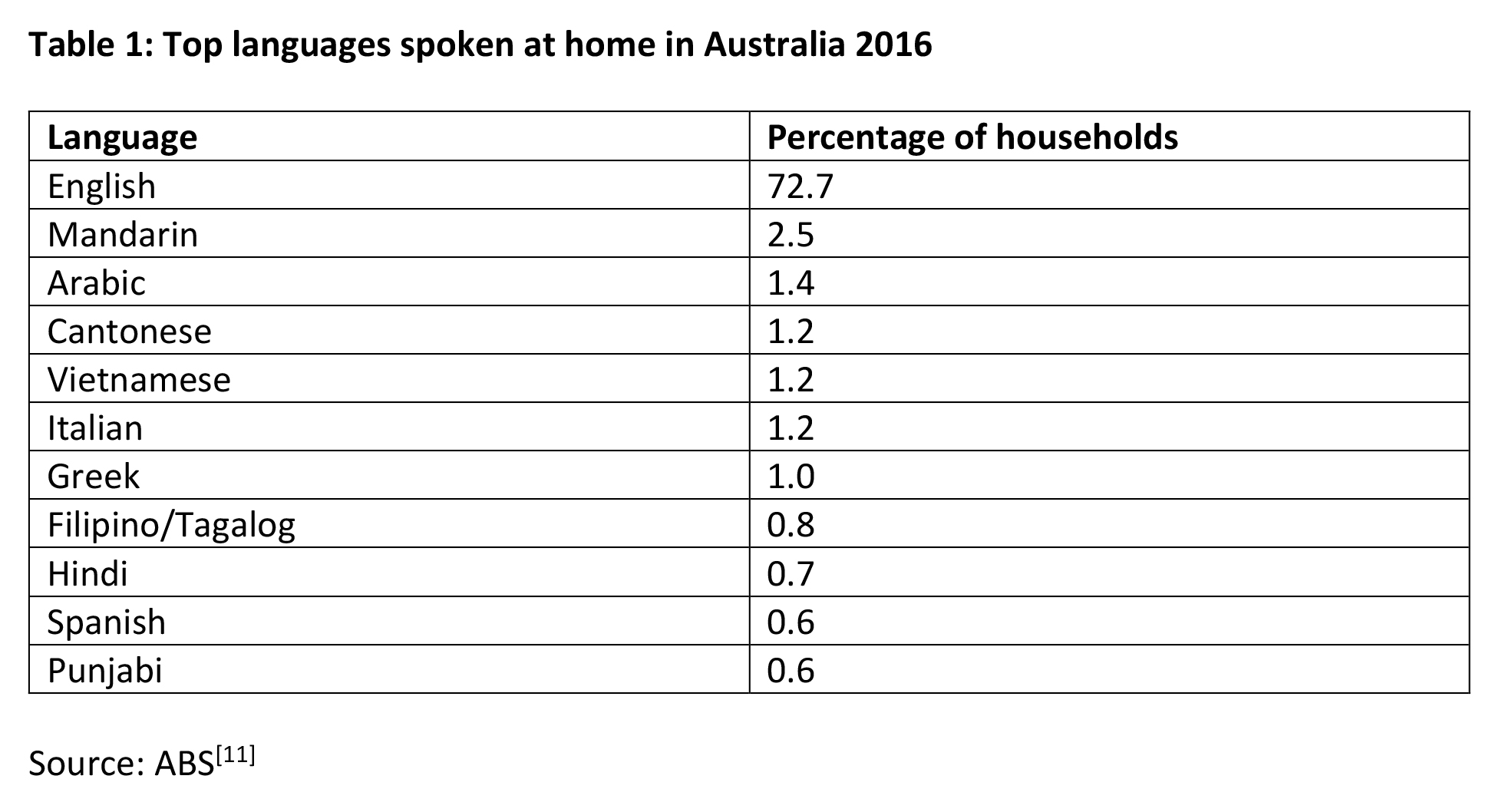

The challenge of language

With around a quarter of Australians speaking a language other than English at home, and research showing these people are more likely to exhibit overconfidence in their financial literacy, the extent to which language barriers create and reinforce vulnerability is arguably deserving of more focus by regulators.

The language used around financial communication, disclosure, and advice itself, is steeped in complex legalese, and as such is challenging even for native English speakers with high levels of literacy.

And yet aside from the odd firm who may translate a specific brochure into another language (Chinese being a common example), the reality is that financial services are overwhelmingly provided in English.

Adding to the complexity is that many languages, have many different and distinct dialects (Mandarin alone has 93 dialects). Nor should we assume that people are literate in their native tongue.

ASIC has never mandated that disclosure documents are provided in any language other than English, and certainly doing so would create enormous logistical and expense challenges for product issuers and distributors.

The challenge for advisers is that adviser obligations under both the Corporations Act and the FASEA Code of Ethics implicitly assume that advisers have taken their own steps to overcome any language or literacy barriers that may undermine a client’s understanding of the advice they have received.

The case study below, whilst involving legal, not financial, advice, provides a salient reminder of just how fraught this issue can be.

Case Study – advice undone by dialects

The husband Mr Bilal and wife Ms Omar signed a financial agreement in February 2007. Three years later, Ms Omar pleaded her alleged lack of understanding of the financial agreement as a reason for it to be set aside. She claimed that she did not understand the legal advice provided by her solicitor prior to signing the agreement.

Ms Omar had no English skills. She only spoke a Lebanese dialect of Arabic and was also illiterate in her native tongue.

Ms Omar’s solicitor provided her with verbal advice in Arabic, though he spoke this in an Egyptian dialect (which Ms Omar claimed at trial not to understand). However, the solicitor also arranged for an Arabic interpreter to explain the financial agreement to Ms Omar after the meeting.

The trial judge ultimately found that since the solicitor was not present at this later session and could not have known what the interpreter had said, he effectively failed to “inform and give legal advice” to his client.

Source: Law Institute of Victoria[12]

Regulatory and industry interventions to protect vulnerable consumers

An important pillar of financial consumer protection is regulatory intervention into product design, distribution, and disclosure.

The general protections for consumers of financial products and services are contained in the ASIC Act and include unconscionable conduct, misleading or deceptive conduct. unfair contract terms, bait advertising, referral selling, harassment or coercion, pyramid schemes, and the offering of gifts and prizes.

In addition to this and other overarching legislation, examples of interventions designed to protect vulnerable consumers in particular include (but are not limited to):

- Design and Distribution Obligations (DDO), intended to ensure products are designed and sold to a pre-identified segment of appropriate customers

- Responsible Lending Laws

- a proposed national register of enduring documents (including Powers of Attorney)

- anti-hawking and deferred sales models for some classes of insurance products.

At an industry level, the FSC, Australian Bankers Association, and AFCA, have each released various codes and guides, including:

- FSC Guide to the Prevention of Elder Financial Abuse

- ABA Industry Guidelines on Protecting vulnerable customers from potential financial abuse, and

- the AFCA Approach to financial elder abuse.

A further word about AFCA

When it comes to protecting vulnerable customers, the Australian Financial Complaints Authority (AFCA) is facing its own challenges. There is an increasing recognition that vulnerable financial consumers find it harder to access AFCA’s services, due to language, literacy, or technological barriers.

According to their CEO, David Locke, “The people who historically would go to an Ombudsman are white, middle class, well educated, and computer savvy[13]”. And yet those who are in more need of protection and redress are people within Aboriginal communities, non-English speakers, and people with physical and mental disabilities.

Recent steps AFCA has taken to address this imbalance include the release of videos featuring their own staff speaking in their native tongue and increasing its translated resources from 14 languages to 20. AFCA now also offers a free interpreter service in 75 languages.

AFCA has seen a spike in vulnerable client-related complaints due to COVD-19 [14] and has released various tranches of guidance on the topic, expressing a particular concern with vulnerable clients who may not be as proactive in driving their complaint, thus requiring more active monitoring by financial service providers.

Adviser obligations and challenges with vulnerable clients

Vulnerable clients are obviously an issue in a financial advice context.

Providers of personal advice to retail clients in relation to relevant financial products, must comply with the FASEA Code of Ethics[15], requiring they:

- act with integrity and in the best interests of each of their clients

- not advise, refer, or act in any other manner where they have a conflict of interest or duty

- provide to a client any advice or financial product recommendations that are in the client’s best interest and appropriate to the client’s individual circumstances

- be satisfied that the client understands their advice and the benefits, costs, and risks of the financial products they recommend, and

- consider the broader effects arising from the client acting on their advice, and actively consider the client’s broader, long-term interests and likely future circumstances.

The requirement to avoid conflicts can present its own challenges when dealing with vulnerable customers. Examples where conflicts may arise include:

- being pressured to provide advice for a vulnerable client by an existing client

- recognising that the client is vulnerable and proceeding with the advice without taking the appropriate precautions, and

- providing advice to a couple whilst suspecting one of them is a vulnerable client.

Practical steps for advisers dealing with vulnerable clients

Generally, when dealing with a vulnerable client, advisers should consider taking extra steps to ensure they are not disadvantaged. These could include:

- being alert to signals that suggest they are likely to be vulnerable

- if there are red flags suggesting the client may be the victim of financial abuse, the adviser must make the client aware and report the issue to the relevant parties, which may include the client’s bank

- allowing a longer time for them to make decisions

- taking extra steps to ensure they understand the recommendations being made to them

- asking extra questions to test their understanding of the recommendations and their basis

- asking the client to explain back key elements of the advice

- third party input

- encouraging them to seek input from a trusted friend or family member, and offering to meet and explain the recommendations to the family member

- extra education

- providing more education tools before allowing the client to trade

- recommending the client undertake education tailored to the client’s capacity to understand

- demonstrate understanding of client’s circumstances

- showing they had concerns with the vulnerability of the client, and the steps taken to address this.

- consider if simpler or lower-risk products would be more appropriate to the level of the client’s understanding

- do not recommend products that require client control or intervention (for example, SMSFs

- don’t allow clients to trade using their SMSFs unless they can show a high degree of financial literacy

- rethink the accessibility of your communication and engagement strategies

- including those around third party communication (superannuation statements, investment updates, insurance renewal notices)

- document every step and action you have taken.

Conclusion

Financial products and concepts are complex and can prove challenging even for highly educated, financially literate consumers, let alone for those consumers who, due to language, cognitive, cultural, or physical difficulties, have heightened vulnerability to financial harm and need elevated levels of consumer protection.

As Australia ages, and becomes more culturally diverse, advisers are increasingly likely to engage clients who, at various times, would be regarded as ‘vulnerable’. It is increasingly imperative therefore that advisers:

- know how to identify vulnerable clients, including those who may be experiencing some form of economic abuse, and

- are able to provide advice in a way that recognises the special needs of such clients, whilst adhering to legal and ethical obligations.

Whilst we have seen various regulatory and industry interventions specifically intended to protect vulnerable financial consumers, the nature of the client/adviser relationship means financial advisers may be uniquely placed to provide advice which acts as the ultimate protection for such clients.

———