Make your advice irresistible, and your clients will reap the rewards

It’s not all doom and gloom for advisers who truly care about their clients.

It’s easy to take a ‘glass half empty’ perspective when surveying the current landscape of financial advice; Increasing cost pressures, falling adviser numbers, a regulatory tsunami that politicians on both sides agree has been overdone. And of course, the ones ultimately paying the price for all this disruption are consumers, who are seeing the accessibility of quality finance advice reduce all the time.

But it’s not all doom and gloom for advisers who truly care about their clients.

According to analysis referenced in Zurich’s ‘Evolution of Best Practice’ Report (EOBP)[1], the average EBIT for advice practices is around 23%, with almost one quarter of practices surveyed reporting EBIT over 35%.

And then there are the outliers, the firms reporting big numbers in profit, new customer numbers, and sustained revenue growth.

What does these outlier firms have in common?

It’s not business model: Some are virtual only, while others remain more traditionally face to face.

It’s not target customer: Some are specialising in millennial females while other are focusing on young families or high-net-worth retirees.

And it’s not the way they charge for their services: Remuneration models vary from low-cost modular advice to monthly subscriptions through to commissions and fee for service.

What actually they have in common is that they have arrived at their advice proposition by taking an entirely different perspective.

Rather than primarily focusing on internal considerations such as compliance, documentation, or reducing the cost to serve, their starting point is the client, their pain points, and how to solve them. They don’t ask ‘how much are you willing to pay for advice?’, they ask ‘how do I make my advice so irresistible you would pay anything for it?’.

It’s a perspective which helps them shut out the noise that seems to distract many of their peers, allowing them focus on creating a true emotional connection with their clients. And by doing so they build a client base who are more loyal and less price sensitive. (In the words of the Zurich EOBP Report ‘Emotional connection is the antidote for penny pinchers’[2].)

Client connection trumps client satisfaction

When it comes to predicting consumer behaviour and business success, a growing body of research suggests that traditional metrics – such as customer satisfaction – can be significantly improved when there is an emotional connection between customers and businesses.

One such study[3], reported in the Harvard Business Review, found that emotionally engaged customers are:

- at least three times more likely to recommend your product or service

- three times more likely to purchase again

- less likely to shop around (44% say they rarely or never shop around)

- much less price sensitive.

Unsurprisingly, such clients are also more valuable to your practice over the longer term, with the same study[4] finding that fully connected clients are up to 52% more valuable than those who are merely ‘highly satisfied’.

Research by Forrester[5] reinforced these results, finding that companies that aim for emotional connection beat their competitors by 26% in gross margin and 85% in sales growth.

So, the numbers stack up. But how does one actually go about creating an emotional connection with clients? First, we need to understand what motivates them, not just in the context of advice, but more broadly.

What emotionally motivates clients?

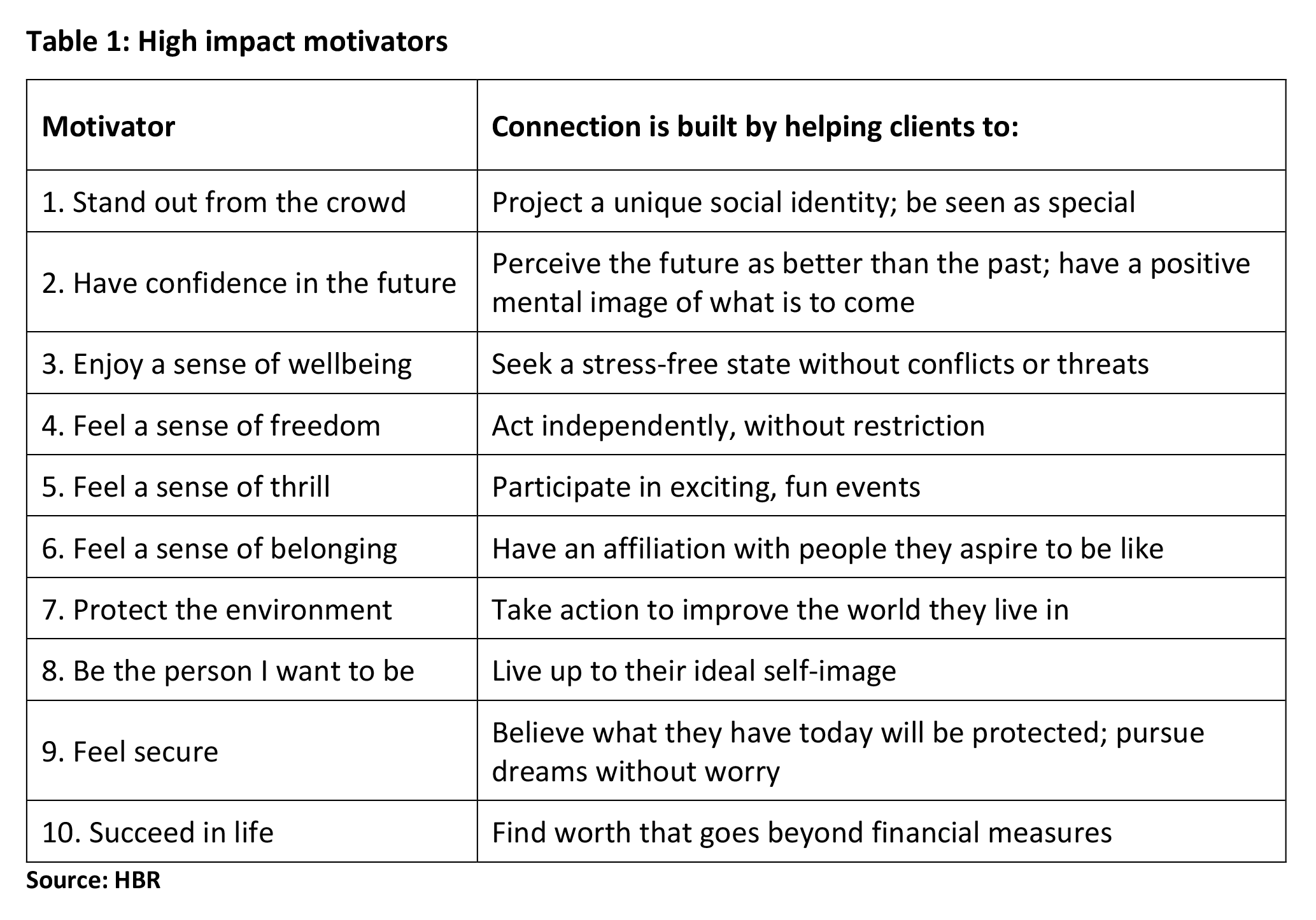

In exploring the nature of connection throughout the customer journey – across many different demographics and brands and categories – researchers Scott Magids, Alan Zorfas and Daniel Leemon found that consumers were influenced by literally hundreds of different emotional motivators, some internal and some external (more on that later). Deeper analysis[6] enabled them to distil these down to 10 ‘high impact motivators’ which, in their words, ‘provide a better gauge of a customers’ future value to a firm than any other metric, including brand awareness and customer satisfaction’.

These motivators, and the way businesses can tap into them, is shown in Table 1, below.

From a financial advice perspective, while it could be argued that all 10 motivators are relevant, there are some that stand out as particularly fertile ground for the adviser and client to connect on: terms such as ‘confidence in the future’, ‘sense of freedom and wellbeing’, and feelings of security and success would figure prominently in many client/adviser conversations. Taken literally, protecting the environment is also area advisers are increasingly helping clients with, as the demand for ESG investing continues to grow.

An alternative way at looking at client motivations – intrinsic and extrinsic

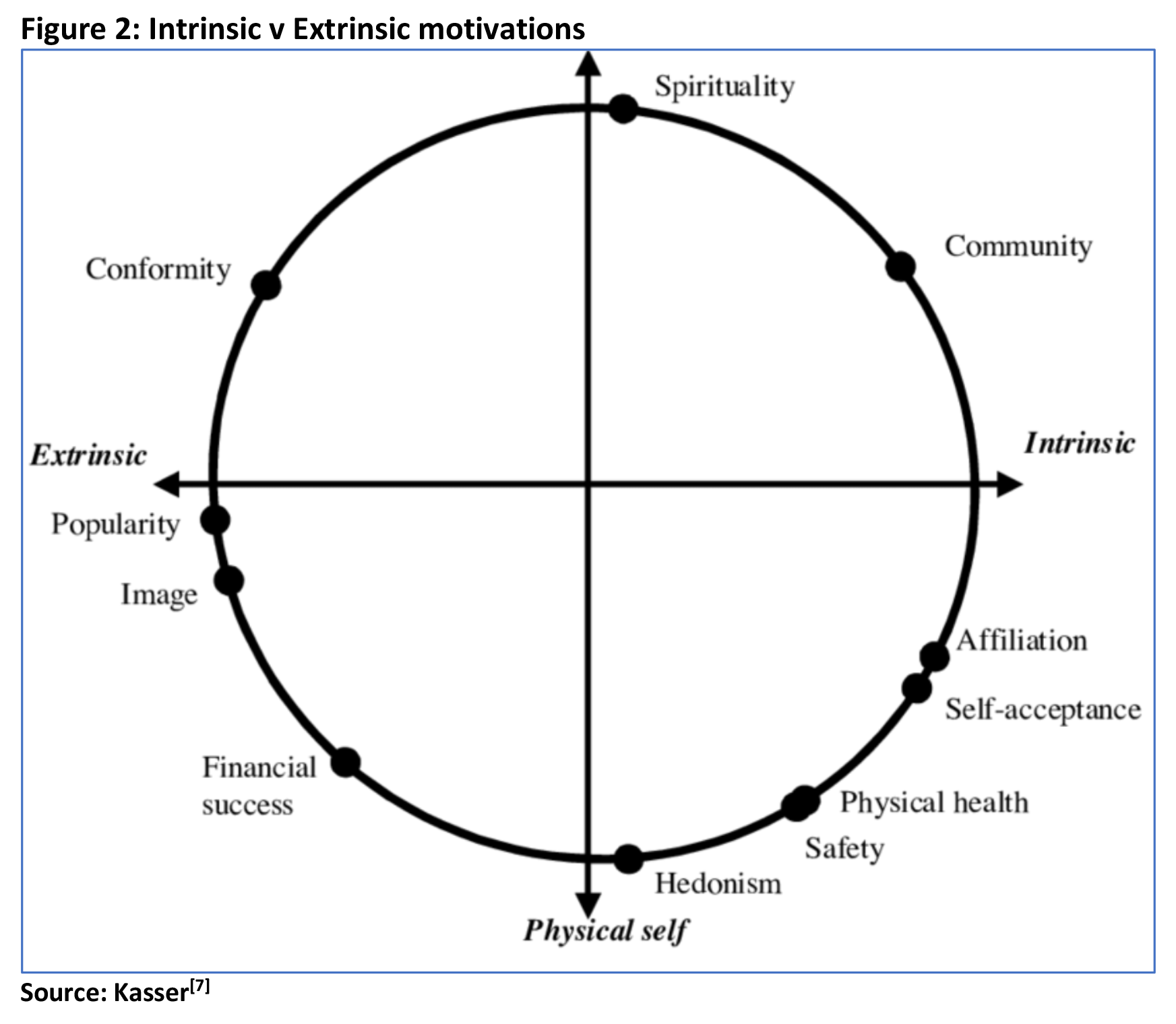

Some of the motivators listed in Table 1 clearly relate to how we are seen, and interact with, other people, whereas others are deeply personal. Professor Tim Kasser of Knox University has authored well over 100 pieces on the link between our finances, our happiness, and what he calls our ‘intrinsic’ and ‘extrinsic’ motivators.

Across his work, Kasser postulates that our sense of identity – who we are and want to become – influences our behaviours in four areas; our desire to conform, our sense of community, our physical and mental health, and our use of money and financial assets.

Those people who have high extrinsic motivation tend to be more pleasure seeking – hedonistic – and seek fame and acceptance of others. Put another way, they make career and financial decisions based on what other people might think of them, with the aim of achieving status and external validation.

High extrinsic motivation usually manifests itself in the form of spending money on things that don’t maintain or improve one’s financial wellbeing – expensive cars, big houses, exotic holidays.

People who have high intrinsic motivation tend to be more emotionally secure and have a greater sense of connection with other people and their community. Their spending tends to be focused on living a life based on what makes them truly happy and is aligned with what is important to them, rather than seeking the approval or acceptance of others. These people are said to be values led.

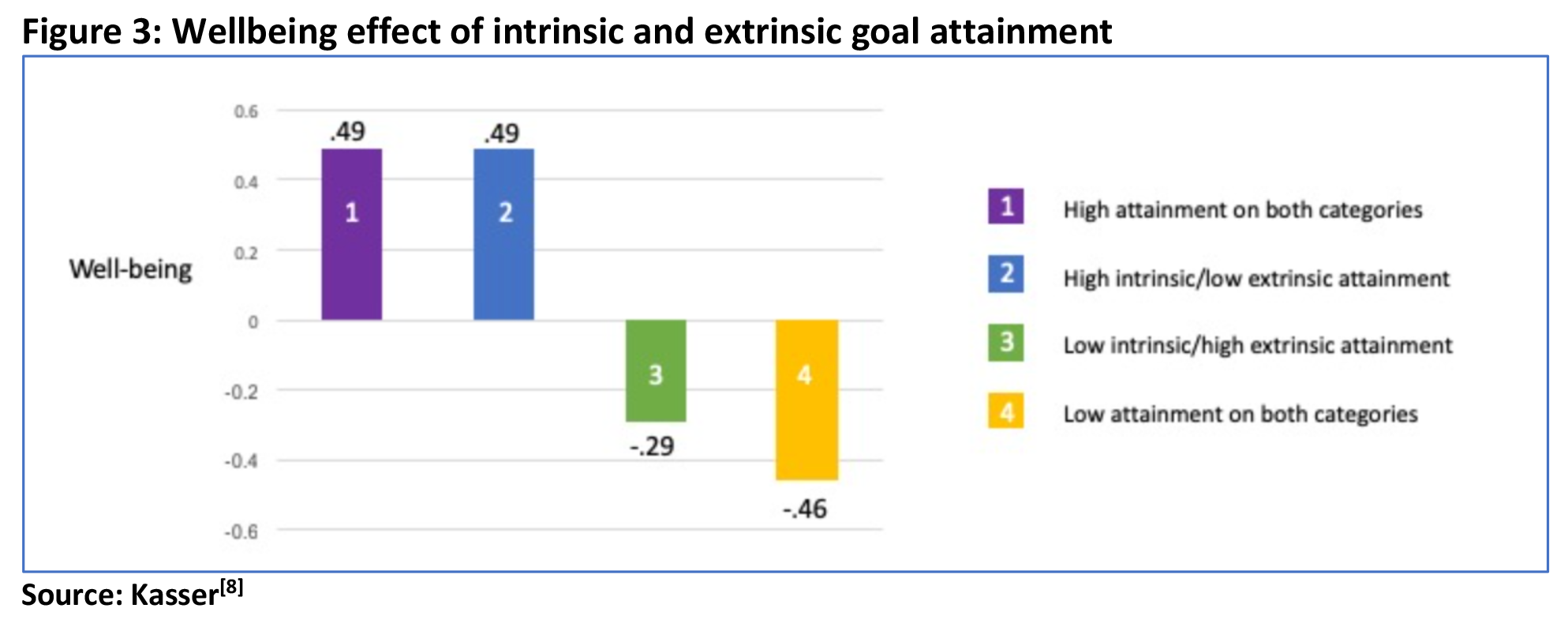

Interestingly, Kasser has also found that the wellbeing effect of achieving – or failing to meet – individual goals depended very much on whether those goals were linked to intrinsic or extrinsic motivations. The results of his study are shown below.

Two points can be taken away from Kasser’s research.

- Achieving extrinsic goals doesn’t impact your wellbeing that much (low extrinsic attainment as per bar 2 didn’t diminish the wellbeing effect); but

- If you don’t meet your intrinsic goals your wellbeing really suffers (bars 3 and 4).

Does this sound like financial advice in Australia? Research suggests so.

Whilst it may be tempting – for some – to dismiss the emotional concepts discussed above as being the domain of counselling, believing instead that the basis of client/adviser engagement should solely be about financial issues, the reality is that clients do share very personal issues with their advisers. And this is not just because of some simplistic ‘more money equals more happiness’ equation (which isn’t actually true), it’s about the positive impact the advice process, the advice outcomes, and advisers themselves, have on our most fundamental emotional drivers.

A 2020 study[9] by XY Adviser found that on average, almost half the time advisers spend with their clients is spent discussing non-financial personal issues. Specifically, the research found that:

- 83% of advisers had experienced a client becoming deeply emotional during a meeting

- 72% of advisers were told a secret by the client, and the adviser was the only one they had told

- 40% of clients had spoken to their adviser about marital issues

- 36% had spoken about conflicts with their children

- 18% had spoken about addiction issues.

A problem – clients sometimes don’t know what really motivates them

Unfortunately, individuals are sometimes uncertain themselves about what emotionally motivates them in relation to a particular product, service, or brand. Or, they know, but they can’t -or don’t want to – articulate it.

In the US, researchers Zorfas and Leeman, mentioned earlier, worked with investment advisory firm to quantify the value of emotional connection, identify its clients’ key emotional motivators, and relate those motivators to the customer experience[10].

They found that clients’ desire to stand out from the crowd, and to bring order and structure to their lives, were the emotions that most strongly motivated them to choose and invest more with that firm.

They then mapped specific facets of the client experience – all the way from opening an account through on-going client care – against both what customers had said was important to them, and what actually affected their emotional connections.

The study found that, whilst clients said they really valued help with transferring funds when opening a new account, in actual fact this was found to have negligible impact on emotional connection. On the other hand, a personal welcome note and online investment education videos were found to have a massive impact, even though the clients hadn’t identified these things as important when asked.

The message here is that firms should focus on those client experience elements shown to drive emotional connection. For this particular firm, client-experience strategies which maximised emotional connection resulted in clients who are six times more likely to consolidate assets with the firm, when compared to clients who are highly satisfied but not emotionally connected[11].

In a practical sense, this means advisers will often need to dig deeper, and peel away the layers of the onion to find out what is really motivating their clients to seek advice.

(Hint: their true motivator is unlikely to be ‘to reduce tax’ or ‘increase investment performance’, or even ‘to have achieve the ASFA thresholds for a ‘comfortable retirement’.)

Adviser implications

There are several considerations flowing from this need to uncover clients’ emotional motivators, and the challenges in doing so:

- deciding the best questions to uncover true motivations, and

- the need to avoid/minimise anchoring advice in goals which are extrinsic (because they aren’t that important and thus won’t help strengthen emotional connections).

Chris Budd[12], financial adviser, and chair of the IFW (Initiative for Financial Wellbeing) in the UK, suggests a good starting point is to look at what client’s say are their objectives and then ask them whether those objectives would lead the client to a truly joyful life with meaning and purpose. If not, then the truly intrinsic motivators – those that drive true happiness – need to be explored.

In a similar vein are the 3 questions used as part of the ‘Life Planning’ methodology developed in the US by George Kinder and Susan Galvan[13].

Question 1: Design your life

I want you to imagine that your financially secure, that you have enough money to take care of your needs, now and in the future. How would you live your life? What would you do with the money? Would you change anything. Let yourself go. Don’t hold back on your dreams. Describe a life that is complete, that is richly yours.

Question 2: You have less time

Imagine you visit your doctor who tells you that you have 5 to 10 years left to live. The good part is you will never feel sick, the bad news is you will have no notice of your death. What would you do in the time you have remaining to live? Would you change your life, and if so, how?

Question 3: Today’s the day

Your doctor shocks you with the news that you only have one day to live. What do you feel as you confront your mortality? What dreams will be left unfulfilled? What do I wish I had finished or had been? What do I wish I had done?

Flip the narrative – reduce the friction

It needs to be remembered that helping your clients work towards goals associated with their emotional motivators – and deepening your connection with them as a result – can be as much about the things you take away as the things you give them. And one of the most important things you can take away is friction. In a client care sense, friction is the extra effort and/or cost that occurs because something isn’t as smooth or seamless as it could be.

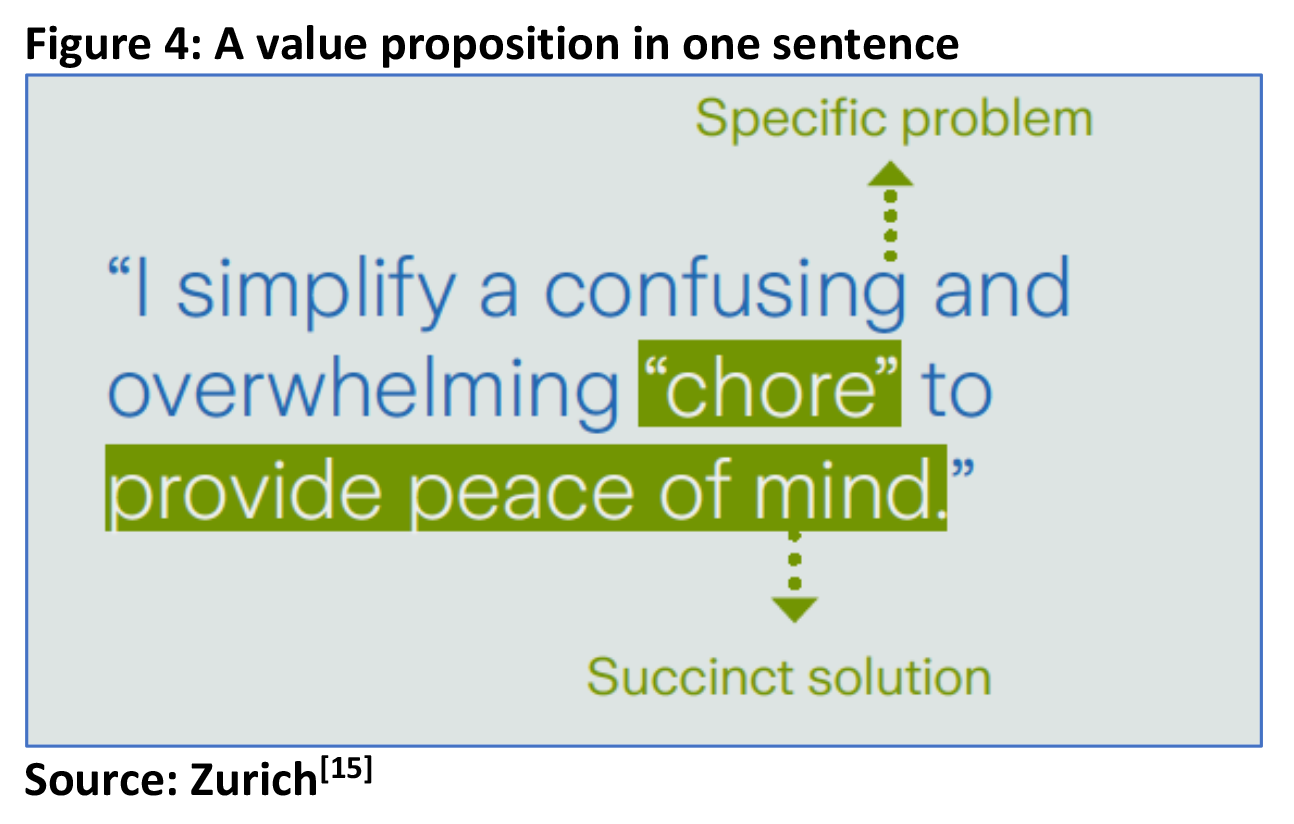

Reducing the friction can take many forms, for example streamlining processes, extending office hours, or reducing the number of times a client gets ‘handed over’ between different people in the practice. Reducing friction can also be the basis of your entire proposition, as it is for Craig Bigelow, a Melbourne-based financial adviser and self-confessed ‘insurance nerd[14].

Bigelow sums up his client value proposition in one sentence, a sentence infused into all his client communication:

Given how most people feel about life insurance, you could say it’s an advice proposition that is almost irresistible!

![]()

———-